Hamish McRae: The odds are on a Greek debt deal. But it won't work

Economic View: Whenever there is a political shock, you should beware of instant market reactions

All reason says that there will be a deal between Greece and its creditors – in effect, the rest of the eurozone. Reason says so because it is in their self-interest, at least in the short-term, for there to be a deal. But if you go through the numbers it is hard to see quite how the deal can be done. Add in the politics: the Greek negotiators are inexperienced and saddled with high expectations among the electorate, while their creditors have been round this block many times already and have red lines that they cannot cross. Maybe, just maybe, a deal is not possible after all.

Whenever there is a political shock, you should beware of instant market reactions. First thoughts are often wrong. Nevertheless, the reaction is troublesome. There has been a surge in government bond yields, with three-year bonds yielding nearly 17 per cent yesterday afternoon, while 10-year bonds are now above 10 per cent. Equally troubling, Greek bank shares have halved since the election was called in December.

There is a further problem. Things have to be done quite quickly. There has to be some sort of agreement by the end of February, when the latest extension of the bailout terms runs out. The new government has reversed some elements of the previous deal, including the privatisation of government-owned assets, including the national electricity utility, and there won’t be much time for it to assemble an alternative credible plan, even assuming that can be done.

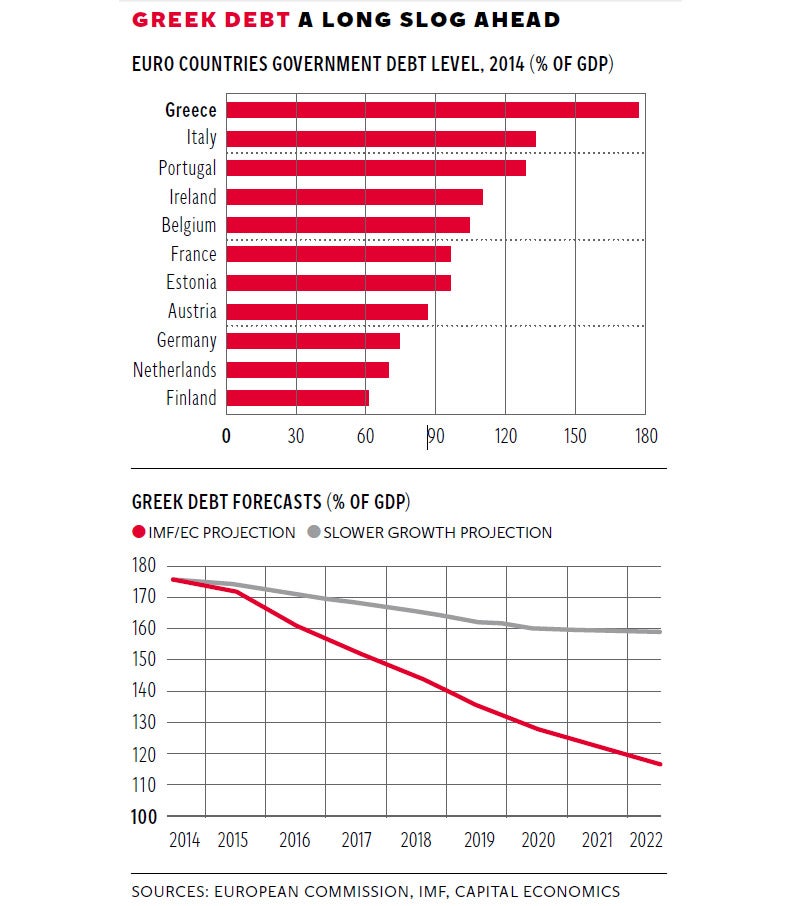

But the biggest problem of all is the maths. The top graph shows Greek national debt as a percentage of GDP compared with that of the rest of the eurozone. At 175 per cent of GDP, it is not only the highest – it is by far the highest. The red line on the bottom graph shows how, under present plans, it is projected to decline. Note that by 2020 it will still be almost as high as that of Italy and Portugal now. The trouble is that this projection is almost certainly too optimistic. It assumes that nominal GDP will grow by 5 per cent – say, 2 per cent in inflation and 3 per cent in real growth. It also assumes that the country will run a primary surplus (a surplus before allowing for debt interest) of more than 4 per cent of GDP. Capital Economics has calculated an alternative path, assuming nominal growth of 4 per cent and a smaller primary surplus of 2 per cent, and you can see the results in the grey line. Debt does fall a little to start with, but remains stuck at around 160 per cent of GDP.

Yet the new Prime Minister, Alexis Tsipras, and the Finance Minister Yanis Varoufakis, who learnt his economics at Essex University and who has been a strong critic of austerity, have both pledged to avoid a clash with creditors. “There will neither be a catastrophic clash, nor will continued kowtowing be accepted,” Mr Tsipras said yesterday.

The problem is that neither he, nor Professor Varoufakis, has any practical experience of such negotiation. Elected governments with a strong mandate can do anything they like, provided they control their own currency and allow that currency to float, and do not need to borrow abroad. But if they defy the financial markets, that independence carries costs. The most immediate way in which those costs are evident is a fall in the currency and a rise in borrowing costs. You can see now that consequence in Russia, following its annexation of Crimea and its support for dissenting Ukrainians.

In the case of Greece, there can be no fall in the currency, for what Greece does is unimportant in the totality of the eurozone. So all of the burden falls on interest rates and hence the country’s ability to borrow. Rates have gone up because Greece cannot service its debt, so no one is prepared to lend to it. In fact, nearly all Greek government debt is held publicly, with private holders maybe dipping in and out but not holding debt long-term. Why should they, when their holdings were halved in value under the terms of the previous bailouts? (Technically there was no Greek default because private holders “agreed” to the writing down of their bonds, while official holdings were protected.)

So what will happen? It only makes sense to talk in terms of probabilities. Since we are only three days into the new government, to do even that is hairy. But try this: if common sense says there should be a deal, then that is the most likely outcome. So there is a strong probability, let’s say 80 per cent that, after a difficult couple of months, a deal will be patched up, allowing longer repayments, lower interest rates, some formula that reduces the headline level of debt without reducing its substance. In exchange for that, the Greek government comes up with a new set of economic proposals that allows the rest of the eurozone to claim that it is making appropriate structural reforms. Both sides will claim common sense has won, and Greece does not formally default and it keeps the euro.

The deal won’t work, of course. In another 18 months there will be another row, another set of negotiations and, who knows, then the outcome may be the catastrophic clash that Mr Tsipras seeks to avoid. But that is in the future.

And the 20 per cent? It is that the clash does come now and Greece formally defaults on its debts and is out of the euro by Easter. Could Greece default and stay within the euro? I suppose anything is possible, but it is hard to see how its banking system could survive without European Central Bank support, so the answer is almost certainly no.

Would that be such a disaster? It would be hugely disruptive but were the country to devalue it would become super-competitive and could grow strongly from then on. To be clear – this is not the probable outcome. But, if the past seven years have taught us anything, it is never to exclude any possibility, however extreme.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments