Greece crisis explained: 7 key points on what happens now the Greeks have voted 'No'

Greeks voted by a large margin to reject the EU's austerity demands

After five years of bailouts, budget battles and a battered economy, Greece is on the brink of becoming the first country to leave the euro zone.

If it seems as if you've been hearing some variation of that for a while now, that's because you have. This time might be different, though, since all the bad things people had only worried would happen are happening. Greece's government last week missed a critical debt payment to the International Monetary Fund, and its banks have been forced to close.

And on Sunday, Greeks voted, by a surprisingly large margin, to reject the European austerity demands that would have meant more financial relief for Greece. The country's banks now are at risk of imminent collapse, and the country could be forced to leave the historic monetary union.

So how did we get here, and what does this mean for Greece, Europe and the rest of the global economy? The short answer is (1) with a currency that's a doomsday device for turning recessions into depressions, and (2) it shouldn't be the end of the world. And the longer one, well, here it is.

(1) What's the situation in Greece right now?

The referendum had asked:

“Should the proposal that was submitted by the European Commission, the European Central Bank, and the International Monetary Fund at the Eurogroup of 25 June 2015, which consists of two parts that together constitute their comprehensive proposal, be accepted? The first document is titled ‘Reforms for the completion of the Current Programme and beyond’ and the second ‘Preliminary Debt Sustainability Analysis.’ ”

The essence of the debate was whether Greece should do austerity on Europe's terms — or its own. In other words, does it have to cut social spending significantly more, as the Europeans want, or can it reduce deficits by raising taxes, as the Greeks wanted?

Syriza, the leftist party that soared to victory on an anti-austerity message this year, successfully bet that Greeks would reject Europe's demands. Many thought they wouldn't, in part because while Greeks don't like the European program, they have long opposed leaving the euro zone.

But on Sunday, in definitive terms, Greece has answered that it wants to chart its own course.

Now Syriza may have a stronger hand at the negotiating table. But the party also has the burden of navigating the country through what's likely to be a painful financial and human crisis. The gamble will shape the economy of this nation of 11 million for more than a generation.

(2) What's next?

If Greece had voted yes, there would probably have to have been new elections — Europe doesn't trust Syriza to actually implement austerity — and, after that, negotiations would probably have continued along the same lines as before.

Now, while Syriza might think it has the better position with Europe, its mettle is going to be tested. The first signs of market reaction will come late Sunday when Asian markets open, and future markets were predicting a swoon Sunday night.

But Monday is the real test. Investors may well refuse to lend Greece money at almost any cost, as banks and the government lack essential funds to operate. Here's what former U.S. Treasury secretary Larry Summers wrote this weekend:

Greek banks will run out of cash early in the week, probably on Monday. There will be an immediate need to either provide them with some sort of IOU scrip to meet demand for funds or to resolve them in some way, as Greece lacks the capacity to create Euro. What the Europeans do and the decisions the Greeks make will shape the future of Greece and the Euro area.

It's possible that the scrips will buy some time -- the Economist has an explainer here -- or some eleventh-hour deal will come. German Chancellor Angela Merkel will be in Paris on Monday for talks, and a summit of euro zone nations will be held Tuesday to discuss the crisis. Even if it won the vote, Syriza may face pressure to accept a better deal, given that Greeks don't want to leave the euro.

But if the European Central Bank ultimately won't give Greece's banks the money they need, then there are only two ways for them to get it. Otherwise they'll crash and burn. That's to either take it from depositors or to print it. The first option, what's known as a bank bail-in, is what Cyprus did when the ECB stopped propping its banks up two years ago.

But the second option is available only one if Greece has a currency it can print. It doesn't right now. It has the euro. So Greece would have to ditch it and bring back the drachma if it wanted to recapitalize its banks via the printing press. Both of these are painful, of course, but default and devaluation could be less so for the economy (more on that later).

In a research briefing July 3, Oxford Economics, a research group, posted the odds of Greece leaving the euro zone at 85 percent with a no vote. On Sunday afternoon, after the referendum vote, top banks including JPMorgan Chase and Barclays said a Greek exit from the euro zone is now their expectation.

Joseph Gagnon, senior fellow at the Peterson Institute for International Economics, explained the mechanics of so-called "Grexit:"

The first step would be to enact legislation to convert all financial assets and liabilities and all commercial contracts and wage agreements issued under Greek law from euros to drachmas at par (one for one). Banks would need to close for at least a couple days, possibly more, to reprogram their systems. Legislation would also specify the introduction of drachma notes and coins at the earliest possible time, perhaps within six months.

The drachma would be allowed to float against the euro as soon as the banks reopen. It would surely depreciate, probably by a lot at first and with considerable volatility before settling down. It is impossible to predict how much the drachma would depreciate; in Iceland’s experience, the financial and debt crisis of 2008 caused an initial depreciation of nearly 40 percent that has since stabilized at around 25 percent in real (price-adjusted) terms. The euro notes and coins currently circulating in Greece would increase in value. During the months before drachma notes and coins are introduced, euro notes and coins would be used for small purchases, with merchants accepting them at the market-determined premium.

Government debt held by Greek financial institutions would be converted to drachmas at par. These institutions would be required to accept new government debt for principal and interest payments coming due. The government would declare a moratorium on principal and interest payments on the rest of its debt, including the debt of the Bank of Greece to the European Central Bank. Negotiations would begin on a restructuring of this nonconverted debt.

(3) What led to this point?

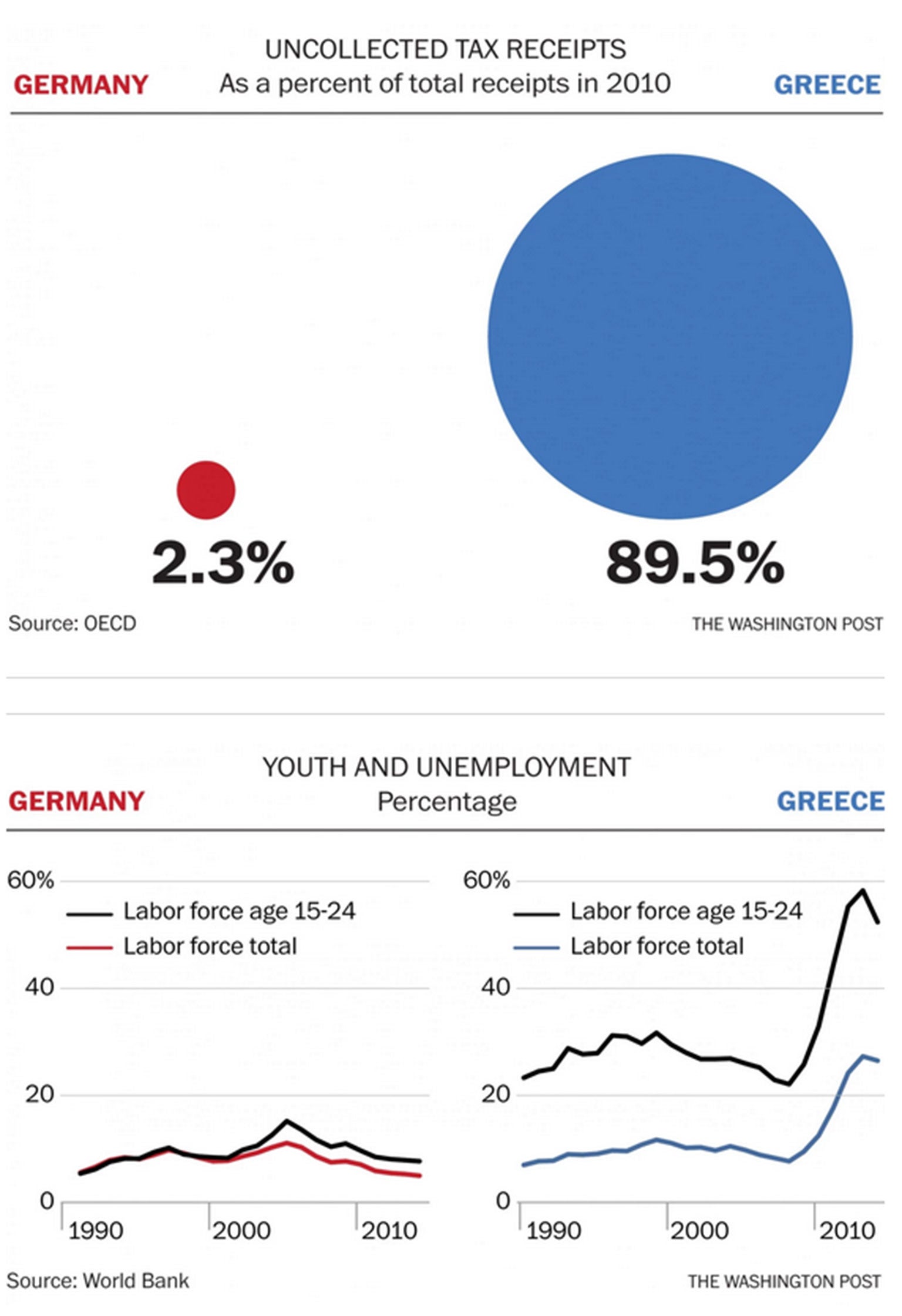

It's a long story that has its roots in the creation of the euro, five years of unsuccessful efforts to stem the burgeoning crisis and the diverging experiences of Greece and Germany, Europe's economic behemoth and decision maker. These two charts make those differences stark:

The first, uncollected tax receipts, shows that Germany has had almost no problem when it comes to taxpayers paying their bills due to the government, while Greece has had an unparalleled challenge. Germany has fewer outstanding tax debts than any other country in Europe, while Greece has more than any other. That difference not only helps Germany enjoy a far more fiscally sound position than Greece, but it offers a stark contrast between a disciplined government and one that historically has been hardly disciplined.

The second, unemployment, shows why Greece wants to take control of its own future. It is suffering the worst unemployment on the continent — worse than unemployment in the United States during the Great Depression — and even worse unemployment among its young workers. When they see that one in two young Greeks is unemployed — a problem that will cast a shadow on the Greek economy for generations — Greece's leaders want a different course.

More immediately, the referendum was called last weekend by Prime Minister Alexis Tsipras after negotiations with Europe broke down in Brussels. The European Commission, the European Central Bank and the International Monetary Fund — "the troika" — were giving Greece the money it needed to function and to, well, pay the troika back. The IMF, in particular, insisted that Greece cut its pensions by 1 percent of gross domestic product, and Greece responded that it was willing to cut them only half as much and make up the difference with higher taxes on businesses. When they couldn't come to an agreement, Tsipras called for the vote.

That led to not only a political escalation of the crisis — but an economic one. There has been a slow-motion bank run the past few months — a bank jog, really — that has picked up pace as it has appeared as if there wouldn't be a deal. That's because people were worried that Greece would be forced out of the common currency without one, and their old euros would get turned into new Greek drachmas, which wouldn't be worth anywhere near as much.

So when there wasn't a deal, Greece was forced to close its banks, limit ATM withdrawals to 60 euros a day and prevent people from moving their money abroad in a capitulation to this panic. Then, on Tuesday, Greece announced that it would default on a 1.5 billion euro payment to the IMF. That wasn't surprising. Greece doesn't have 1.5 billion euros. It doesn't have anything. It's broke.

For a moment it seemed talks might resume last week. Greece's government was making a last-minute request for a new bailout, and Europe was offering at least minor concessions. But then German Angela Merkel and other creditors made clear that they want to await the terms of the referendum, and the rhetoric coming from Syriza only heated up, making the referendum all but a certainty.

(4) How terrible is this situation for Greece?

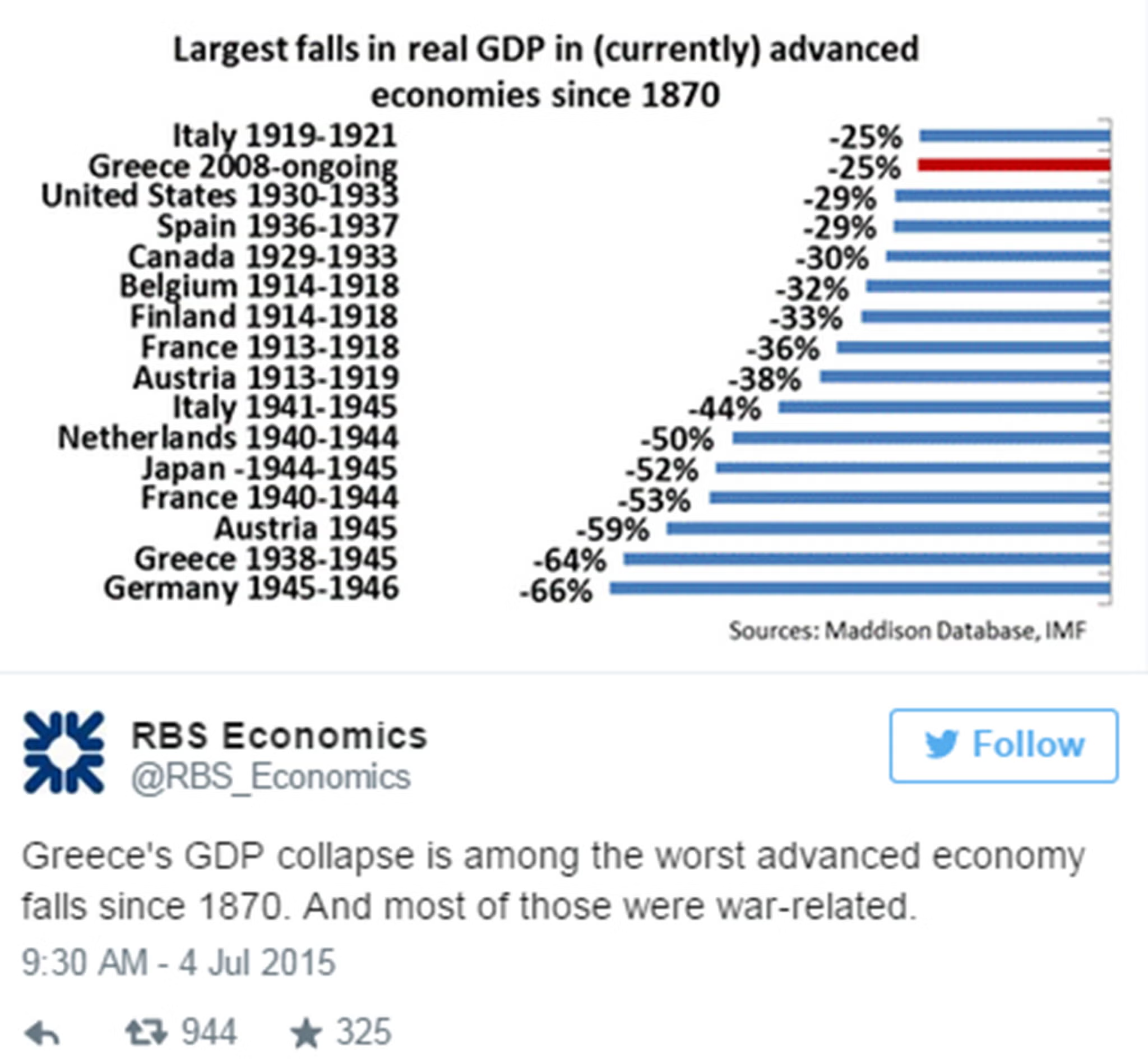

The situation is pretty terrible. As this tweet from RBS Economics shows, Greece has suffered one of the worst economic declines in modern history, especially considering that it is not at war.

(5) Would leaving the euro be an absolute disaster?

It is hard to know what the future brings beyond more Depression. But there's a case to be made that leaving the euro could be a good thing for Greece. If not that, there's an even stronger case to be made that joining the euro was a bad thing.

As the culmination of Europe's 60-year project toward greater and greater integration, the euro was a political masterstroke. It was also an economic albatross. And it's one that wasn't hard to see coming. Plenty of economists, including Nobel Prize winner Milton Friedman, warned that it wouldn't work for countries with different economic needs to share a single monetary policy but not a fiscal policy. At any given time, money would be either be too tight or too loose for some members, and there wouldn't be anything — like unemployment insurance — to balance it out. The euro, in other words, is a paper monument to peace and prosperity that has made the latter impossible for some countries.

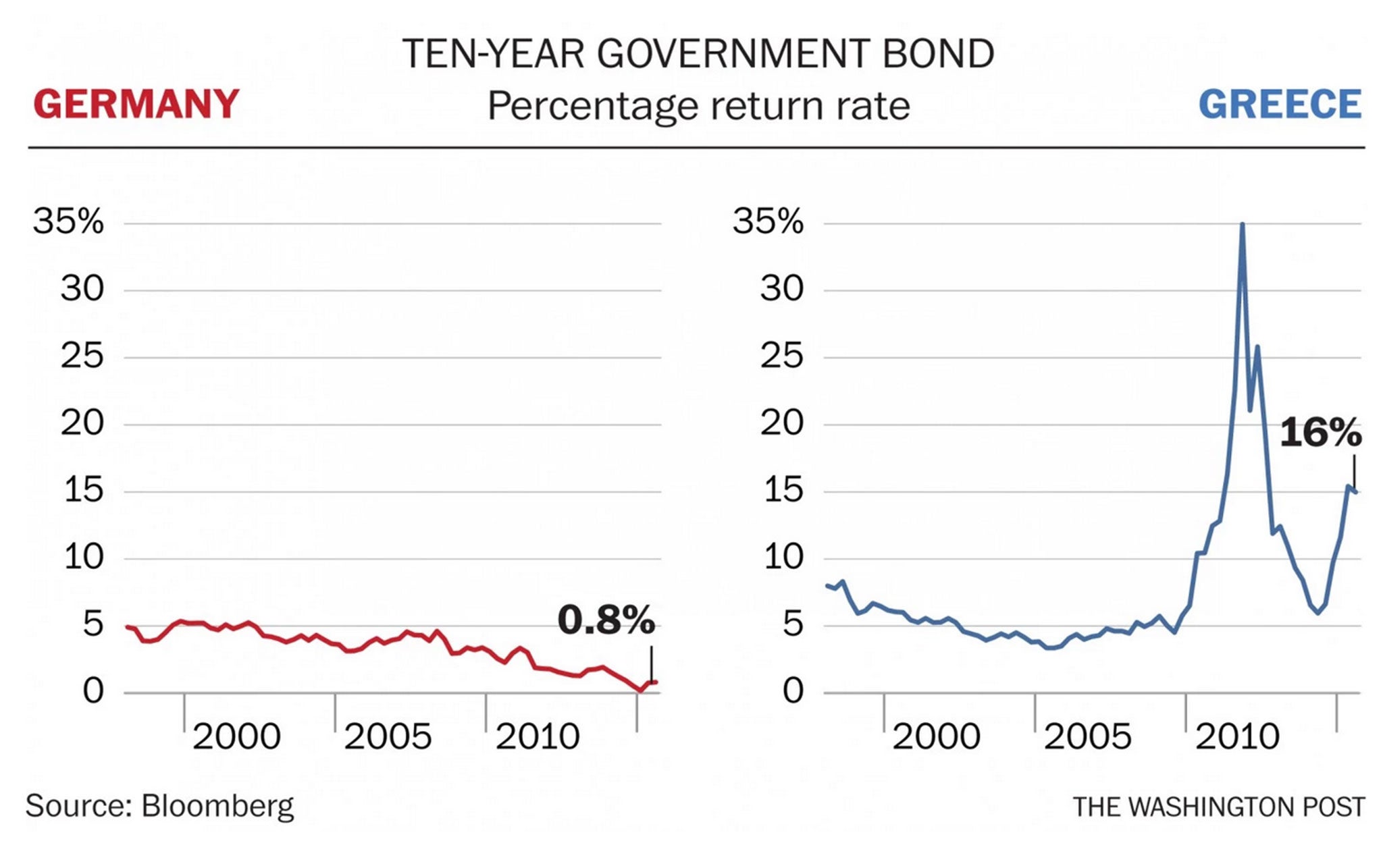

None more so than Greece. Its big bubble in the early 2000s was the result of interest rates that were too low for it, and its big bust since is, in large part, the result of a currency that has been too strong. You can see that in the chart below comparing bond yields between Germany and Greece. With a stronger economy and much less debt, Germany should have always paid less to borrow. But investors treated more risky Greece and Germany the same for years, because they were both part of the euro.

When the debt crisis started, though, investors abandoned Greece and rushed for safe havens such as Germany (and U.S. Treasury bonds).

Now, instead of being able to devalue its way back to competitiveness, Greece has been forced to deflate its economy. That is, it has had to cut wages — which makes unemployment worse — rather than cut its currency. It's the same problem that the gold standard created during the 1930s. The difference, though, is that Europeans are even more attached to the euro than they were to the gold standard, which is saying something, since, at the time, they equated it with Western civilization itself. That's because the euro is the gold standard with moral authority.

Nobody wants to get rid of the real problem, and so the other ones continue.

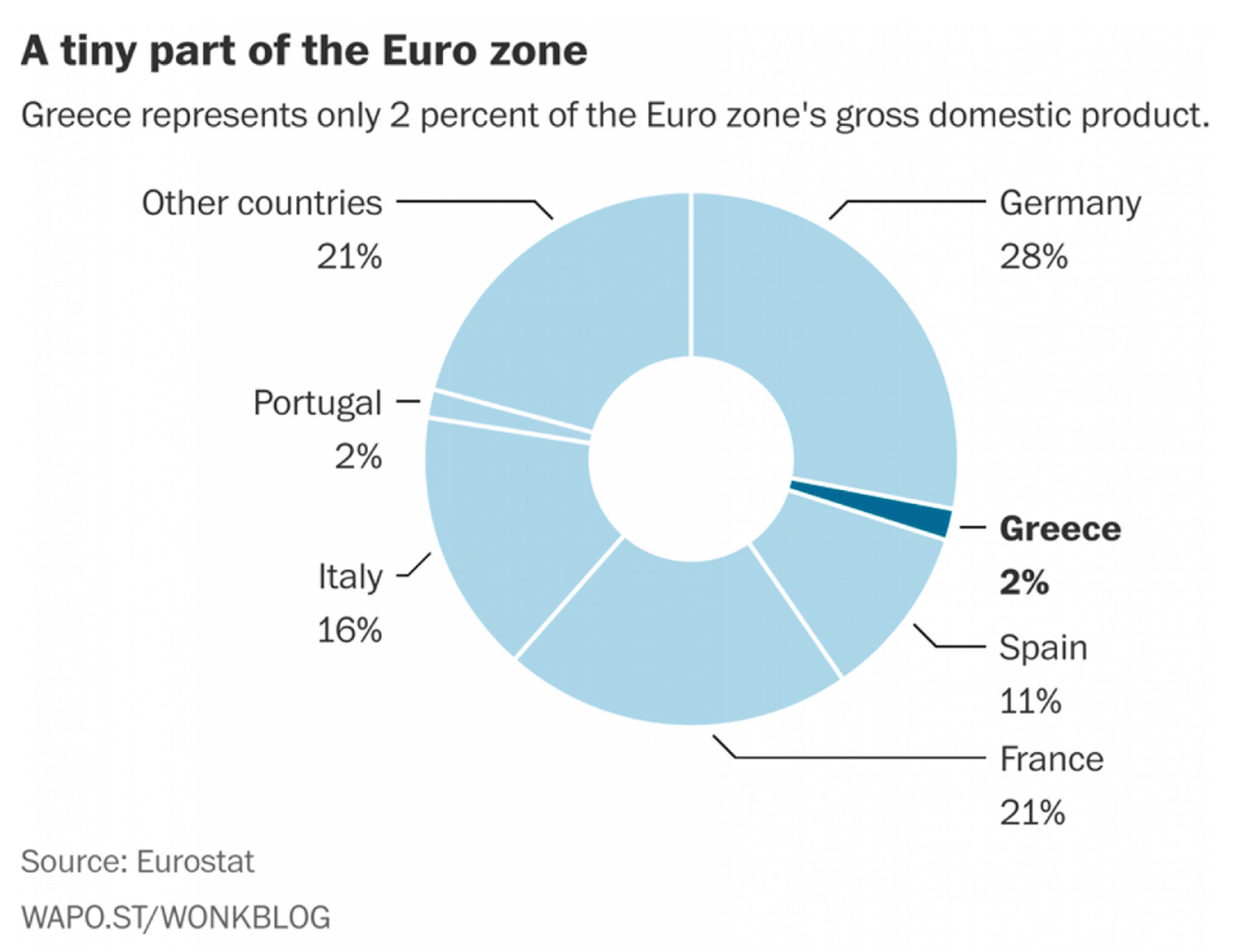

(6) But why does everyone care so much about Greece? Its economy is tiny, isn't it?

It is. Greece's economy is only about 2 percent of the euro zone's total. But the best way to think about why something so small still matters so much is to think about how we got here in the first place. Now whenever a country borrows too much, the IMF usually recommends that it write down its debts, balance its budget and devalue its currency. The idea is that it's pointless to try to pay back more than you can — it can actually be self-defeating — but you also need to become fiscally self-reliant so you don't have to go back for one bailout after another.

The tricky thing, though, is that at the same time you're raising taxes and cutting spending, which hurts the economy, you need to get it growing again. Otherwise, shrinking national income might make it harder for you to pay back your debts even though you have fewer of them. And that's why the IMF prescribes a big dose of monetary stimulus — that is, a cheaper currency — to offset the economic pain from fiscal austerity. That, by the way, is how Iceland managed to recover so quickly though it cut its budget more than any country not named Greece.

But this isn't what happened in Greece. Well, aside from the austerity. It did get a lot of that. What it didn't get, though, was a cheaper currency or enough debt relief. This last part is the original sin of Europe's bailouts. See, back in 2010, policymakers were petrified that the euro zone was like a line of dominoes just waiting to get knocked over by the weakest link. If Greece defaulted on its debt, the French and German banks that had lent it money might go bust, and the banks that had lent them money might, too, and, well, you get the idea. Not only that, but default also might force Greece out of the euro, at which point markets would begin to bet against whatever they thought was the next weakest link. That would push up borrowing costs for, say, Portugal and make it more likely that it would, in fact, default, which would then push up borrowing costs for Spain, and, well, you can fill in the rest. In other words, Greece wasn't allowed to default, even though it needed to, because doing so threatened to set off a series of self-fulfilling prophecies that could have ripped the common currency apart.

So Greece got bailed out to the extent that it was given money to then give to the people to whom it owed money. That was good news for the aforementioned French and German banks that got their money back, but it wasn't for Greece. It still had as much debt as before, only now it owed official creditors such as the IMF instead of private ones like the banks. Now, it's true that two years later, its official-sector debts were given lower interest rates and longer maturities at the same time that its private-sector debts were actually written down. But it wasn't nearly enough, especially given that it was getting harder for them to pay anything back with their economy collapsing under the combined weight of budget cuts and a too-strong currency. Indeed, since 2008, Greece's debt burden has shot up mostly because of its economy getting smaller rather than its debts getting bigger.

It took only five years, but Europe finally might be ready for a Greek default. Emphasis, though, on the word "might." Even though the ECB has created a firewall that should keep any kind of panic from spreading, it hasn't been tested yet. It should be enough, but who wants to find out? Europe doesn't if it can help it. But Europe also doesn't want to not find out so much that it's willing to give Greece whatever it wants to keep it from happening. This game of chicken, in other words, might end differently than the last.

(7) So what does this mean for the global economy?

* Greece. The new drachma would plummet, inflation would soar into the double digits, imports such as food and oil might need to be rationed, companies that borrowed in euros might go bankrupt, and the government would have to balance its budget overnight. In other words, things would get a good deal worse than they already are, which is saying something when you're talking about a country with 25 percent unemployment. But after a year or two, this pain would pass and Greece would be left with a cheaper currency that would make its exports more competitive and its tourism more attractive.

* Europe. First off, they'd lose real money here, as in the hundreds of billions. Greece's government hasn't just gotten 240 billion euros, but its banks also have received 89 billion euros in loans from the ECB that might be defaulted on in the case of euro exit. Second, there'd be some contagion. Borrowing costs could creep up for Italy, Spain and Portugal, but the fact that the ECB is already buying their bonds and has promised to buy as many as it takes to keep their interest rates low means they shouldn't rise that much. Third, all this uncertainty should make the euro fall further, boosting their exports in the process. And finally, though this might sound cruel, the worst thing that could happen to Europe is if Greece does well after it leaves. That would embolden anti-austerity parties in the rest of the continent by showing that they have nothing to lose but their fiscal chains by challenging the continent's budget-cutting orthodoxy.

* The United States and everybody else. Our banks should be fine. Some hedge funds might fail. And the stronger dollar (the flip side of the weaker euro) should make our exports a little less competitive overseas. And that's it. There really shouldn't be too much damage from the failure of a country whose GDP is the size of Connecticut's. The fact that there ever would have been — and there would have — tells you how fragile the euro zone is.

Zachary A. Goldfarb contributed to this report, which is adapted from a June 30 report.

Copyright: The Washington Post

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments