Bernanke told on tapering but the hawks didn’t listen

It made sense to wait and see because of the impending change in the chairmanship

Sign up for the View from Westminster email for expert analysis straight to your inbox

Get our free View from Westminster email

I arrived at Boston Logan at around 4pm ready to fly to Spain to give a speech just before a fire started at the fuelling depot, which closed the airport down. That was a bad surprise. Eventually, off we trundled with a few drips of fuel that could be scrounged from a beamer (whatever that is) to Bangor in Maine, which was the first American airport I ever landed at in 1971, and only 175 miles from home.

Then it turned out that the crew had done too many hours and it was already 1am. I managed to get a nice hotel at the airport and we eventually left at 7pm. I had a change of clothing and the hotel had a toothbrush and a comb so I was all set. The moral of the tale is to prepare for the unexpected. Twenty-four hours late, I arrived in sunny Malaga.

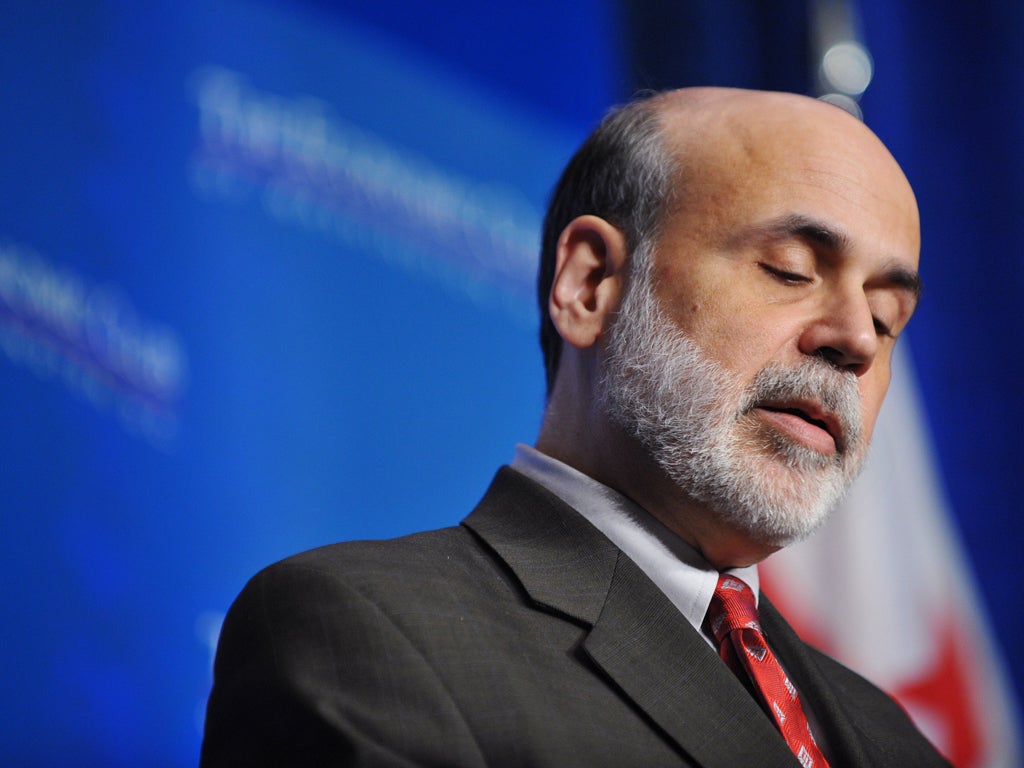

The one advantage of the unexpected stop was that it was “Fed Day”, and I sat expectantly in my hotel room for the much-awaited decision to be announced at 2pm. There wasn’t much else to do. To taper or not to taper, that was the question. Were the 12 voting members of the Federal Open Market Committee, which sets monetary policy – eight governors and four Federal Reserve Bank presidents – going to take the first steps in an exit strategy? Would they cut asset purchases from the $85bn a month split between $45bn of Treasuries and $40bn of mortgage backed securities (MBS)? If so, by how much? Would tapering be evenly split between MBS and Treasuries?

I have to admit that I did have skin in the game because I had said in an interview some time ago that the chance of tapering occurring at this meeting ‘was for the birds’. Never one to be backward in coming forward; if they did taper I was going to have to eat humble pie, but not for the first time.

Central banks got themselves into the business of quantitative easing in the depths of recession in 2008 and 2009. Once they got in, everyone wanted to know how and when they would get out. Would interest rate rises precede a sell-off of assets? When would this happen? That put central bankers in a quandary, as they could certainly not provide a certain date. How long is a piece of string?

Chicago Fed president Charlie Evans argued that this should be done by following the data. Fed governor Janet Yellen also made a speech supporting such a strategy of forward guidance; the Fed would extricate itself contingent on the data – their responses would be path dependent. In June at a press conference, chairman Ben Bernanke suggested that if the data turned out the way the Fed thought, tapering would start in September. The markets appeared to interpret this as a commitment; various Fed officials said this wasn’t the case, and Mr Bernanke then made clear that asset purchases could actually increase if the data worsened. But the markets didn’t take any notice.

Tapering was set in stone; except it wasn’t and they didn’t. Plus they revised down their estimates of growth in 2013 and 2014 and can still see no inflation anywhere. The hawks were wrong as ever. I had a clue that they weren’t going to taper, when a high-level Fed source told me last week that “if Bernanke was a dictator, they would not be tapering”.

But the data gave it away as it had worsened recently, suggesting the FOMC would sit on its collective hands. First, bond yields rose so the average rate on a 30-year fixed-rate loan was 4.57 per cent in the week ended September 12, close to a two-year high. Second, purchases of new homes plunged 13 per cent in July, the most in more than three years.

Third, mortgage applications have fallen in 15 of the last 18 weeks, reaching their lowest level since October 2008 last week. Fourth, the University of Michigan consumer sentiment index in September fell to 76.8 from August’s 82.1. The index measuring expectations six months ahead fell to 67.2, its lowest level since January, from 73.7. Fifth, US retail sales rose less than forecast, up 0.2 per cent in August, the smallest gain in four months. Sixth, Consumer Price Index inflation increased 0.1 per cent in September, the least in three months.

Seventh, non-farm payrolls expanded by a weakish 169,000 workers last month, after downward revisions to June and July. Finally, over the next month or so, the Congress will return and try to agree on a budget: Mr Bernanke has made clear on several occasions failure to agree quickly represents a major downside risk to growth.

All of this suggested a wait-and-see strategy, and so it turned out. The FOMC would have known its decision was going to be a surprise to the markets, and so the jump in equity markets and decline in bond yields along with a weakening of the dollar would have been broadly expected and welcome. It did warn that its response was data-contingent, and it was.

It also made sense for the Fed to wait and see because of the impending change in the chairmanship at the end of January when Mr Bernanke’s term is up. But he wouldn’t say at the press conference whether he would stay on, and he still might. The big news earlier in the week was that Larry Summers withdrew as it became increasingly obvious he would have trouble being confirmed in the Senate.

The front-runner now is Ms Yellen, who I know and have publicly backed. She is an accomplished labour economist, and appointing her would imply a seamless transfer – what you see is what you get. It’s hard for the Fed to be credible on forward guidance when President Obama hasn’t made up his mind on who will be doing the guiding. We could do without a big surprise though. Go Janet, go.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies