Secular stagnation? We should hope it's not true - but also plan for the worst

Economic View

It’s hard to make predictions, especially about the future. Alvin Hansen found that out the hard way. In the late 1930s the distinguished economist advanced a gloomy thesis that America was in the grip of what he termed “secular stagnation”, brought upon by a slowing of population growth and a dwindling of technological innovation.

This was always a risky prediction given that secular means 100 years. Economists famously have trouble forecasting one year ahead, never mind a century. And in the event Hansen didn’t have to wait even a decade for his prediction to turn to ashes. After the Second World War the US embarked on one of the greatest economic booms in history, powered by technological innovation and a baby boom.

But did Hansen merely get his timing wrong? The disappointing performance of the world economy since the global financial crisis in 2008 has prompted some of today’s top economists to dust off the secular stagnation thesis. Foremost among them is Larry Summers, the former US Treasury Secretary, who kicked things off with a ruminative speech at the IMF in November 2013.

The debate has been raging ever since. Among those who have dismissed the idea of secular stagnation are George Osborne and the Governor of the Bank of England, Mark Carney. And last month the former president of the Federal Reserve, Ben Bernanke, entered the ring, picking holes in the Summers thesis.

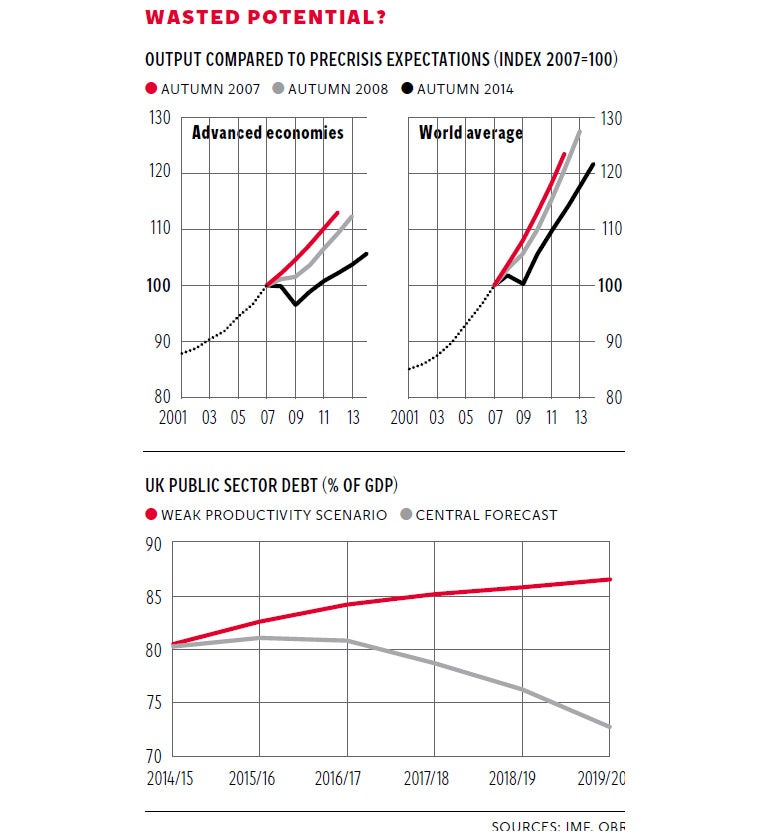

Yet this week the IMF seemed to come down on the side of the stagnationists, noting how radically weaker growth has been than expected before the financial crisis (as the first chart demonstrates) and judging that it will “remain below pre-crisis rates in the medium term”. The IMF, like Hansen, cites weaker population growth and weak investment as the root causes of the stagnation.

Suppose for a moment that the pessimists are right. What are the implications of a secular stagnation world? The IMF picked out two. First, it means much slower growth in living standards than we’ve historically come to expect. That’s a pretty sobering prospect for us in the UK, where average living standards have flat-lined since the financial crisis. If secular stagnation is a reality that means things are not going to snap back to normal any time soon.

Second, lower future growth will make it more difficult for both households and nations to cope with their accumulated debt burdens. The Office for Budget Responsibility spelt this out last December when it produced a forecast for the UK sovereign debt to GDP ratio under a “weak productivity” growth scenario. Under its central forecast growth averages around 2.3 per cent over the next five years and the debt ratio falls from 80 per cent of GDP to 70 per cent. But, as the second chart shows, if productivity is weak growth averages 1 per cent a year and the national debt burden carries on rising right through the forecast period to 87 per cent. We need decent growth to put the public finances back in order.

So what can be done? It’s important to clarify some elements of the debate. Secular stagnation means different things to different economists. For some it’s mainly a pessimistic forecast about the likely future pace of technological change. For others, particularly Summers, it’s more a story about a chronic shortfall in demand, which means economies will fail to grow at their full potential and that unemployment will remain damagingly elevated.

These different diagnoses argue for different solutions. There is not a huge amount that governments can do if technology is the limitation, aside from investing in research and education and hoping that this produces a breakthrough. But if demand – or spending – is the problem governments can do rather a lot. This includes investing in infrastructure and redistributing income to those more likely to spend. The solution is, thus, akin to a kind of permanent-Keynesianism, which probably explains why many of those on the right of the political spectrum are sceptical of the stagnation thesis. It argues for the kind of interventionist government policies that they have spent their political life reviling.

But are we really stagnating? That is, of course, the key question. And it impossible to answer definitively at this stage. Summers, Bernanke and the rest of the profession can bat around theories and counter theories as much as they like but we will not know until we’ve seen the out-turn data in several years.

So what stance should fiscal and monetary policymakers adopt today given this uncertainty? As with policy during the financial crisis, the cost-benefit logic points to a proactive approach of stimulus. If the demand shortfall stagnation thesis is correct this will prove to have been the right course. If the thesis is wrong – or it is being driven by an innovation shortfall – then we will get a burst of inflation and policy will have to be tightened. The costs of inactivity in terms of lost output and higher joblessness would outweigh the costs of activity in the form of excessive price rises – especially given inflationary pressures are presently absent across the developed world.

We should, of course, hope Summers is as wrong today as Hansen was 80 years ago. But it would be prudent for policymakers to behave on the assumption that he’s on to something.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks