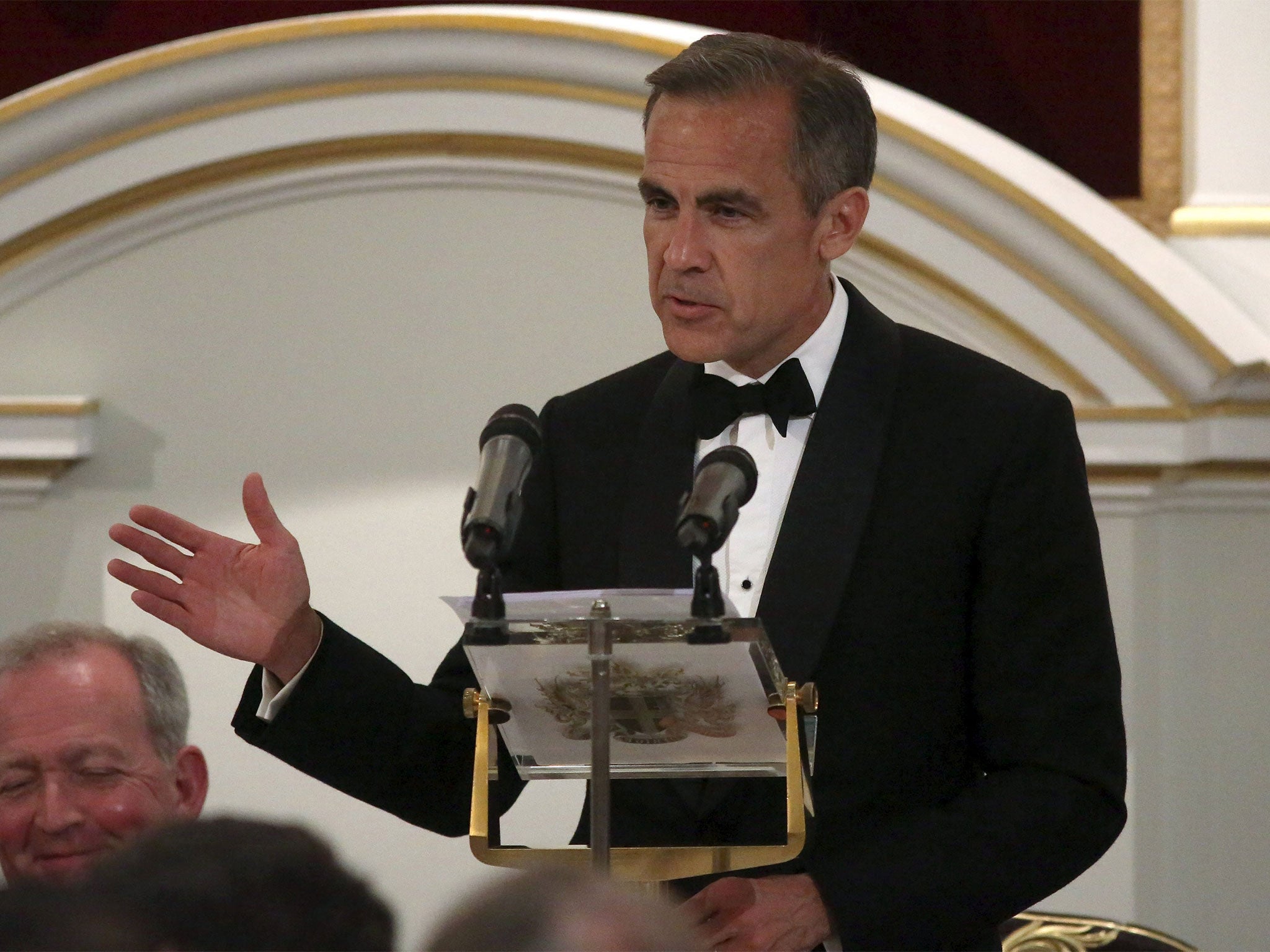

Mansion House speech - Mark Carney tells City of London: 'The age of irresponsibility is over'

Speaking at the annual Mansion House dinner, he unveiled a host of new sanctions and procedures designed to cleanse financial markets

For free real time breaking news alerts sent straight to your inbox sign up to our breaking news emails

Sign up to our free breaking news emails

Mark Carney warned the City of London that the "age of irresponsibility is over" as he unveiled a host of new sanctions and procedures designed to cleanse financial markets that have been tarnished by a tidal wave of rate rigging scandals.

Speaking at the annual Mansion House dinner, the Bank of England’s Governor promised that traders fired for misconduct would have their full history made available to prospective employers. He also called for criminal sanctions to be "updated", with longer maximum prison terms for rate-riggers.

Mr Carney added that a "senior managers’ regime" would be extended beyond banks to cover asset managers and hedge funds, meaning that all those in charge of traders active in markets vulnerable to abuse will find themselves personally “on the hook” for promoting compliance within their organisations.

"For the best in the industry this won’t be new. This is just how you run your business," Mr Carney said. "But for others, who free-ride on your reputations: the age of irresponsibility is over."

The UK’s largest banks, including Barclays, HSBC and Royal Bank of Scotland, have been fined billions of pounds by regulatory authorities over the past two years for the illicit actions of some of their senior traders, who rigged Libor and foreign exchange benchmarks for personal profit.

“Unethical behaviour went unchecked, proliferated and eventually became the norm,” Mr Carney told the audience of City grandees and senior executives. “Too many participants neither felt responsible for the system nor recognised the full impact of their actions.”

The crackdown plans emerge from the Bank’s so-called Fair and Effective Markets Review which was commissioned by the Chancellor, George Osborne, and Mr Carney in June 2014 to restore public trust in the City. Mr Carney admitted that the Bank itself “fell short” over the past decade, pointing to its faltering provision of liquidity to lenders during the crisis, its failure to spot “gaps in the regulatory architecture” and its own “arcane governance” structure.

An independent inquiry earlier this year by Lord Grabiner cleared the Bank of any complicity in rigging. But Mr Carney nevertheless said the Bank would henceforth apply the same new senior managers’ regime to its own staff, including himself.

He said that the draining of trust in financial markets had had “direct” consequences for the real economy. “Mistrust between market participants has raised borrowing costs and reduced credit availability.

Falling confidence in market resilience has meant companies have held back productive investments. And uncertainty has meant people have hesitated to move job or home. These effects are not trivial and they have reduced the dynamism of our economy in the post-crisis years.”

That was echoed by Andrew Tyrie MP, the chairman of the Commons Treasury Select Committee, who welcomed the Governor’s plans. “Business will locate and flourish in trustworthy markets. So the discovery that the FX market had been rigged made [the review] essential, not just to clamp down on misconduct but to safeguard UK markets’ competitiveness” he said.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies