Savers in flight from Greek banks amid mounting fears of euro exit

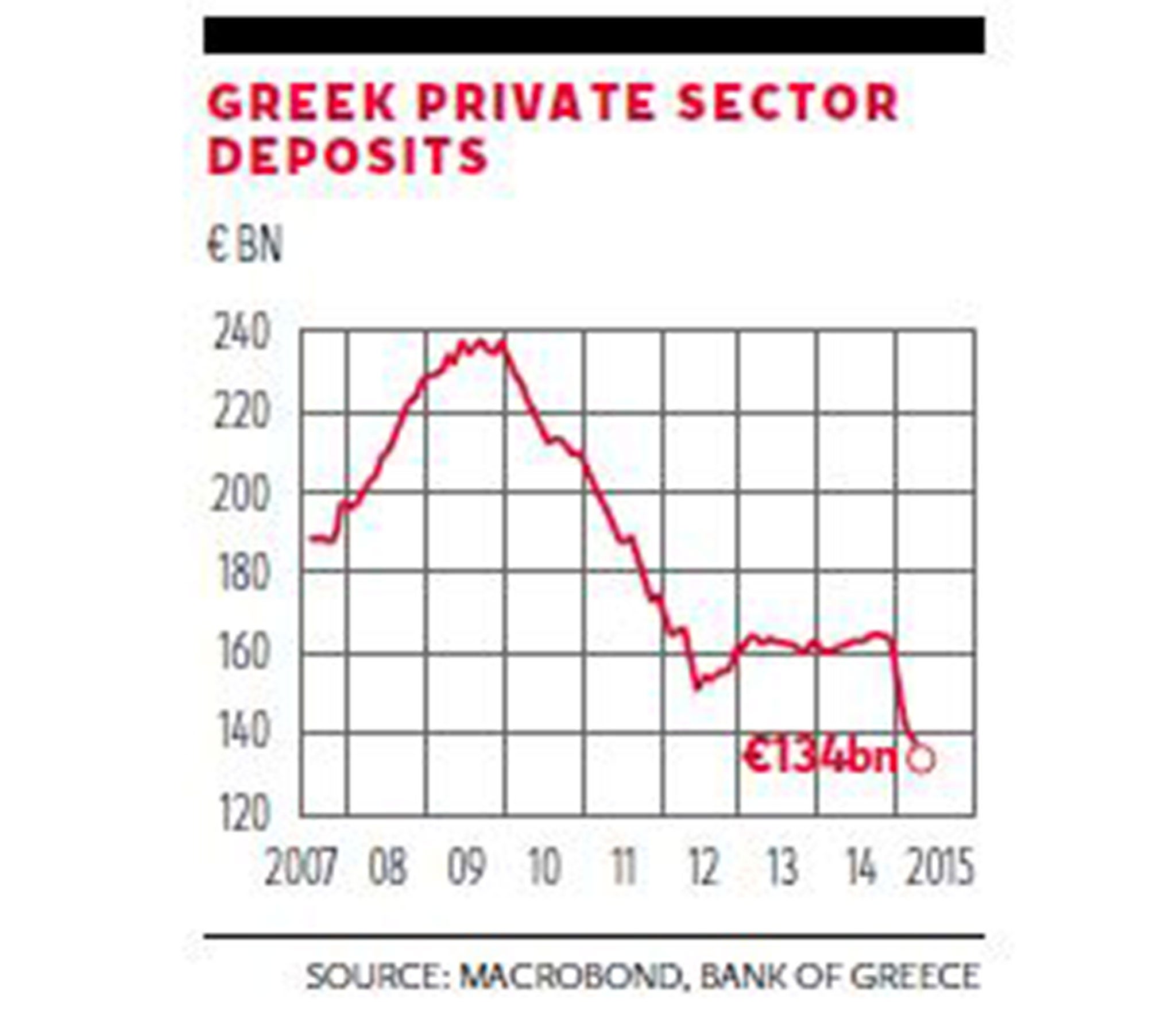

Fears of a looming “Grexit” prompted savers to pull almost €5bn (£3.6bn) out of Greece’s beleaguered banks in April, leaving deposits at their lowest level for over a decade.

The Bank of Greece’s alarming figures come as the nation’s left-wing Syriza government struggles to strike a deal with its international creditors over reforms in order to unlock €7.2bn in bailout loans needed to keep the country afloat. Greece is due to make the first of four debt repayments to the International Monetary Fund totalling €1.6bn next Friday, but Greek ministers say the country cannot afford to pay.

Deposits by households and businesses fell to €133.7bn in April, from €138.6bn the previous month – more than €100bn below their September 2009 peak, according to the Bank of Greece. Since the start of the election campaign that brought Syriza to power, €31bn has been pulled out of the banks, which are being propped up by more than €80bn of expensive emergency support funding from the European Central Bank.

The exodus of savers comes amid concerns that Greece’s protracted battle with its lenders will force it out of the euro – leaving euro-denominated savings converted into vastly cheaper drachmas, or bank deposits slashed to recapitalise banks in a “bail-in” rescue of the type seen two years ago in Cyprus.

“The main factor of uncertainty remains deposit flight, which is likely to accelerate in case of renewed political uncertainty, leading to a liquidity crunch and the introduction of capital controls,” warned Federico Santi, an analyst at the political risk consultancy Eurasia Group.

Athens insists that a deal is imminent, potentially as soon as this weekend. But European officials insist there is still no sign of a breakthrough, with Greece’s leadership unwilling to compromise on cuts to pensions demanded by the IMF as well as labour market reforms. The IMF also opposes its plans to raise the minimum wage. The French Finance Minister Michel Sapin said bailout talks “are progressing faster but not yet fast enough to conclude”.

The US Treasury Secretary Jack Lew waded into the row yesterday at the G7 group of leading industrial nations in Dresden, warning that the brinkmanship on both sides risked “courting an accident”.

He accused both sides of wasting time since January, adding: “Once you reach a general agreement, you still have a lot of work to do ... So it would be in the best interests of all parties to reach an understanding at a general level and leave some time to work through some detail before whatever the next deadline after is.

“I think waiting until the day or two before whatever the deadline is, is just a way of courting an accident.”

Greece can choose to “bundle” the four IMF payments together and pay on 19 June, although the bailout deal expires at the end of the month. Its Finance Minister Yanis Varoufakis – sidelined from the negotiations in recent months – insisted a deal would be struck imminently. He told Greek radio: “This negotiation has taken long enough. We are not prepared to drag the Greek people – and ourselves, I must add – all the way to September.”

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments