Hamish McRae: Britain up, eurozone down - for once, the Bank is right

Economic View: The markets conclude that this news is so bad the ECB will have to find ways of injecting new demand into the eurozone

For free real time breaking news alerts sent straight to your inbox sign up to our breaking news emails

Sign up to our free breaking news emails

Um, a somewhat better outlook for the UK and a somewhat worse one for Europe. That is really the headline summary of the economic news yesterday, and for once I think that the simple story is the right one.

It is a relief to have the Bank of England revising its growth forecast up for a change, instead of down. If this sets the tone for the next year or two it would be a relief, because we have had two years when the pessimists have tended to be proved right and the optimists wrong.

As for Europe, now clearly back in recession with the eurozone experiencing six quarters of decline on the trot, the main concern must be that even the present official forecasts will prove over-optimistic, as they have in the past, and that growth will not resume next year.

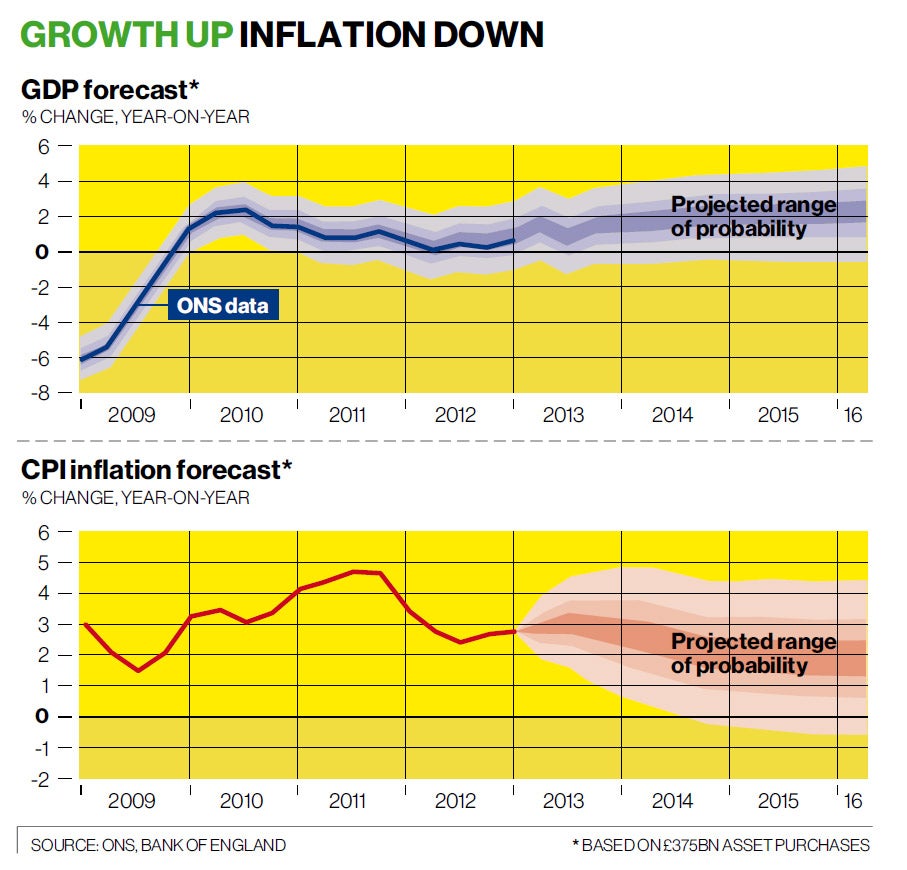

As far as the UK is concerned, the Bank's Inflation Report fan charts are a useful place to start. As you can see, the Bank expects a gradual recovery to the long-term growth trend of 2-2.5 per cent a year, and a similar gradual decline in inflation to around 2 per cent. It also seems to expect some upward revisions to past growth numbers, which would be consistent with the elimination of the "double dip".

There is a similar marginal improvement in the inflation outlook compared with previous reports. But in both cases the bands on either side of the central number are quite wide. If the past four years has taught us anything it is that we should be aware that a 90 per cent probability band means that there is 10 per cent chance of the outcome being outside the band.

The inflation projections are based on current market expectations of interest rates and no further quantitative easing, but if things turned out differently there would be changes in policy. The growth figures, well, there have been changes in policy because the deficit-cutting programme has been stretched out, but quite where they go next is unclear. There is a possibility that faster-than-expected growth might get the fiscal position back on track, as seems to be happening in the US, but if there is one overriding message from the report, it is that there is still a long way to go.

There is also a long way to go in cutting unemployment, as the latest labour market statistics show. They are a mixed bunch, with good elements balanced by bad ones. So unemployment on a three-monthly basis is up a bit, but the claimant count is down; and the fall in total employment is balanced by a rise in full-time jobs. But we do rather need stronger figures from now on, and only greater growth can bring that.

If the message for the UK is sort of all right, the message for Europe is sort of all wrong.

That the eurozone is in recession is not a surprise. That France is in recession is not a surprise. That Italy and Spain are declining at an annual rate of 2 per cent, dreadful but not a surprise. The surprise is Germany, which only managed to eke out a little growth in the first quarter thanks to a downward revision of the previous quarter. Indeed there may be further downward revisions of this quarter, propelling Germany into true double-dip territory. So even Germany is in trouble.

Exports? Not good, because demand from China is down and there is more competition from Japan thanks to the weaker yen.

Domestic demand? Flat and getting flatter – very bad car sales in March.

Was there any good news at all? Sure, but it is scraping the bottom of the barrel. Portugal declined at an annual rate of "only" 1.2 per cent, a lot better than before, and the Greek economy actually grew a tiny bit.

The conclusion of the markets is that this news is so bad that the European Central Bank will have to find ways of injecting new demand into the eurozone economy. European equities climbed slightly on the expectation of action. The ECB has leeway to do so, for inflation is well below target, but quite how is harder to envisage.

What worries me is that expectations of the ECB are running ahead of its realistic opportunities. Central banks can print money and cut interest rates, as the ECB has just done, but the link between this and creating sustainable real demand is a loose one.

The hardest thing is to translate this mixed bag into some sort of prediction for the rest of this year. It is difficult to see much of a recovery in the UK if there is no prospect of growth in Europe for a year, maybe longer. On the other hand, the stream of anecdotal evidence here is not bad: businesses a little more optimistic, retailing mostly all right and online retailing storming away, car sales good, activity in the housing market picking up, a modest wealth effect from higher share prices – and so on. Recoveries never feel great in the early stages, and this certainly doesn't, but for once the official view from the Bank feels the right one.

Have equities gone up too far, too fast?

A word about equities, for the performance in recent days has been extraordinary, all the more so because hardly anyone saw it coming – even those of us who were pretty positive have been surprised. The FTSE 100 index nudged above 6,700 in trading yesterday, having been below 6,250 less than a month ago. The previous all-time close of 6,930, reached on 31 December 1999, suddenly seems not that far away, with valuations now much more reasonable than they were then.

So without wanting to spoil the party, let's just put on record that two economists that I admire are sounding notes of caution. Chris Watling of Longview Economics thinks there is a high risk of some sort of pull-back, while Simon Ward at Henderson asks: "Should equity investors take profits?"

Neither have sounded a serious alarm; both think that things may have gone a bit too far, too fast.

My own feeling is that at some stage in this market the FTSE 100 will indeed get past its previous all-time high. But maybe not just yet.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies