Hamish McRae: Despite the danger of deflation, cheaper energy is a bonus to the world

Economic View: As so often in economics, a plus may, in the short term at least, seem a minus

To what extent will cheap, or at least cheaper, oil and gas offset any fall-off in global growth? It is impossible to distinguish cause and effect and so it may be that much of the decline in energy prices in recent months has simply been the result of a slowing down of growth in what has now become the world’s largest oil importer, China. Equally, as evidence has mounted that maybe China won’t slow so much, energy prices have recovered a bit.

But to focus on the day-to-day movements obscures a bigger story. That story is the increase in oil and gas production in the US is clearly giving a boost to the US economy and, through its impact on world-energy markets, a lesser boost to the rest of the world.

Historically, whenever there has been a significant global slowdown, energy prices have fallen. That decline, together with softer commodity prices, is one of the mechanisms through which the world economy recovers, for less money spent on energy is more money to spend on other things. But while energy prices did fall a bit after the last downswing, they did not fall as much as they had in previous cycles. The reason, insofar as we can pick out a single cause, was that the Chinese economy carried on growing pretty much as before. So too did India’s. So we in the developed world did not get the boost we might have expected to get and had to resort to other means, including very loose monetary policies, to crank up growth.

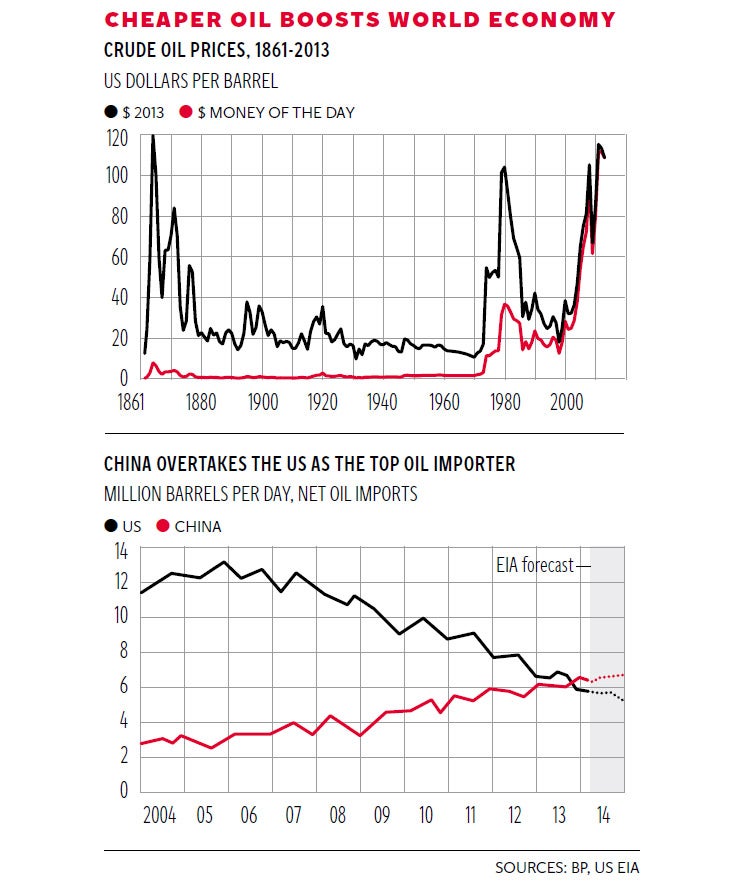

Now we seem to be getting a delayed-action fall. It is happening notwithstanding the fact that the US is growing steadily, though Europe is not. Oil is still expensive by historical standards, as you can see in the top graph, which comes from BP and shows it in real terms as well as money terms going back for more than a century. Even back at around $80-$90 a barrel in present day dollars it is still expensive. As the world has hunted down a finite resource and had to use more-complex ways to extract it, you would expect it to remain much more expensive than it was before the first oil shock in the early 1970s. But as anyone filling up their car on the forecourt knows, right now it is a lot cheaper than it was a few months ago. The oil price affects all energy prices and since for most consumers energy is a necessity, a cheaper price feeds directly through to higher demand for other things.

This boosts demand in just about every country, the only exceptions being the small-population oil producers. It boosts demand in China, now the world’s largest oil importer (see bottom graph). But the place that is feeling this most directly is the US.

There are two broad reasons for that. One is that Americans drive a lot. Even relatively low-income families have to use a car for travel to work. Using older and less-efficient vehicles does not help either. The other is that US industry is benefiting from the shale oil and gas boom. Thanks to that it looks as though the country will once again become the world’s largest oil producer.

This is a huge subject, with environmental and safety issues that need to be tackled. But looking simply at the economic impact, it is pretty clear that US industry as a whole is benefiting greatly from access to cheaper power than its competitors in the rest of the world, while its chemical industries are helped by cheaper feed-stocks. Part of that benefit is temporary in the sense that it is a function of underinvestment in gas technology. Natural gas is very cheap indeed because of the investment (pipelines, LNG plants, terminals, etc) needed to get it to market or to export it. Eventually the equipment will be put in, though there are huge practical and political issues, and the price differential should narrow a bit. But meanwhile US manufacturing has a large price advantage over the rest of the world.

Maybe prices won’t narrow that much. The International Energy Agency’s next annual report will not be out for another couple of weeks, but last year it said it expected that by 2035 US gas and electricity prices would still be half those of Europe or Japan. If that is right, the differential benefits will run for a generation.

As for the boost to the world as a whole, the top management of Dow Chemical, the largest US chemical company by sales, told investment analysts last week the benefits would feed through to the US, UK, Japan and China over the course of the next year. In other words, we have not yet seen anything like the full effect on the world economy.

There is, however, one twist. It is that while lower energy prices are very helpful in holding down inflation, boosting real demand and living standards, in a world of falling prices they have the immediate effect of making them fall faster, in other words increasing the danger of deflation. In Europe, then, it is just possible that a falling oil price will become the thing that nudges the Continent into deflation.

Quite how the authorities will respond remains to be seen – and well, it may not happen. But as so often in economics, a plus may, in the short-term at least, seem a minus. For the US, though, and indeed most of the world, cheaper energy is a pretty solid bonus.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments