Hamish McRae: Increasingly the future of the world economy is being determined by what happens in the Brics

Economic View: While China is pressing forward on bank reform 'the omens are not good'

The past couple of weeks has seen a progressive reassessment of the strengths and weaknesses of the Brics. They are, of course, an utterly different group of countries, linked simply by the fact that they are the four largest emerging economies. But three of them have, for quite different reasons, been downgraded in the eyes of the business and financial communities.

As far as Russia is concerned there is not much more to be said. What has happened has confirmed that there are political risks to business with Russia that are hard to calculate. You might have imagined that something similar to what has happened in Ukraine could have been foreseen but it evidently was not. The fall of both the rouble and Russian share prices in the past few weeks shows that this risk was not "in the market".

In the case of Brazil the switch has been driven entirely by economics rather than politics, with growth back in 2010 of 7.5 per cent flipping to near-recession at the moment. Actual recession is thought unlikely but there is no doubt that the country is experiencing very slow growth. It is, in the phrase of The Wall Street Journal, "a wilting giant".

India is the one of the four where prospects are perceived to have improved, while in China there are two stories. One is about the transition from an economy driven by investment and exports to one driven by consumption. The other is the shift from an economy where there was very little debt to one where debt, known and unknown, hangs over future growth.

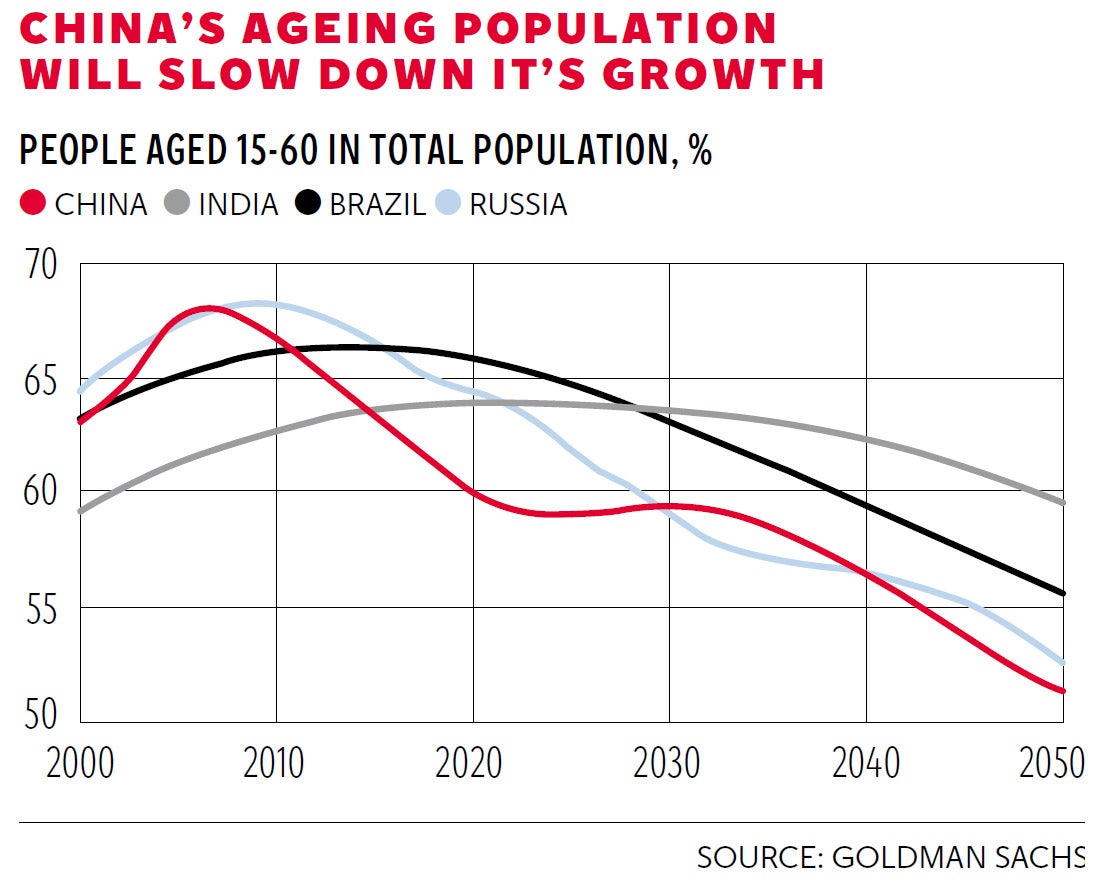

The first is a necessary and inevitable shift of emphasis. As you can see from the graph, which shows the size of the working-age population relative to the total population, China's demographic structure is becoming more adverse, at least from an economic point of view. The one-child policy is starting to kick in. Russia faces similar headwinds, while in the case of Brazil and especially India, demographic trends are positive for some time yet. Demography is by no means the only driver of economic growth, but it is an important one. On a long view it seems reasonable to expect Chinese growth to decline, while that of India and Brazil to remain high.

China's first story is illustrated by some sharp numbers for trade last month, when there was a rare trade deficit. Imports were up 10 per cent on February last year, while exports were down 18 per cent. True, this is just one month but it gives a feeling for the transition that China is seeking to make. Why shift so much stuff abroad and pile up dollars that go down in value, when you can use those resources to improve the living standards of your own people? It's a difficult transition to make and it does, in the view of Steen Jakobsen, the chief economist at Saxo Bank, involve short-term pain. But that pain, he argues, will lead to long-term gain.

Besides, the country has to do this because export-driven growth will run up against increasing resistance. As Andrew Smithers notes in a paper out yesterday, China's past policy of boosting its economy through an undervalued exchange rate has been successful but has created problems which are becoming more acute. He argues that to hold down the exchange rate China had to increase its foreign exchange reserves, which in turn had to be sterilised to prevent the resulting increase in domestic liquidity from causing inflation. This has been successful, but at the cost of creating a large, unregulated, parallel banking system.

That leads to story two, the rise of debt. The growth of the parallel banking system is not the only source of instability; the boom in investment, orchestrated to try to offset the impact of the global downturn, also involved huge borrowing. Relative to GDP, public debt in China is quite low, around 50 per cent (we are about 80 per cent). But add all debt together, public and private, and insofar as we know what it is, it must be at least 200 per cent of GDP. Worse, a lot of that debt has been accumulated by poor investment decisions. So there is a dilemma: China needs fast growth to work through its debt mountain but one of the main ways it has maintained fast growth is piling up more debt.

How serious is this? Diana Choyleva at Lombard Street Research suggests that while China is pressing forward on bank reform "the omens are not good". She argues that the authorities have to allow defaults rather than have banks roll over loans that cannot be repaid. That was the policy employed by Japan to shore up banks after the property bubble of the 1980s, which meant Japanese banks were so stuffed with bad debts that they were unable to make new loans to creditworthy customers. The result was 20 years of stagnation.

I don't think China is in that position, for two reasons. First it is a much less mature economy, with much greater growth potential. Second the scale of the indebtedness, as far as one can see from the outside, is much more manageable. But over the next decade Chinese growth will slow, as it needs to, with all the implications this will have for demand for raw materials and energy.

A final quick word about India. The rupee is very undervalued – by more than 30 per cent against the dollar, according to some calculations by World Economics. So the country should be ripe for an export boom. Elections start next month, with the strong possibility that the BJP, led by Narendra Modi, will take office. This will be controversial, but there is a perception that India will have a more business-friendly climate and lift growth, currently 4.5 per cent, to something nearer 6 per cent.

We will see. The big point here is that the future of the world economy is being increasingly determined by what happens in the Brics rather than what happens among the G7. On my quick tally the Brics will this year again add more demand to the world economy than the G7, as well, of course, as continuing to grow more swiftly.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments