Shoppers are flocking to spend their money, the pound is soaring – and the Government is counting its blessings

Economic View: If you want to know what's really happening with the economy look at what people do, not what they say

For free real time breaking news alerts sent straight to your inbox sign up to our breaking news emails

Sign up to our free breaking news emails

Confidence is a slippery beast. You think you know what is happening by asking people, be they replying as individuals or as company executives, how confident they feel. But you get responses that are at best crude and uneven, and at worst misleading. If you are more precise and ask businesses whether they think sales, prices or employment will go up or down – as in the purchasing manager surveys – then you do get helpful signals for what is happening. You can then take these and project what is likely to happen to economic growth.

For many years now these PMI surveys have given a good feeling for growth in the UK. They caught the initial recovery, the slackening of growth and now the new boom. They were pretty consistently more optimistic than the GDP figures as initially published, but the GDP figures have subsequently been revised up and will be further revised in the future. Current growth is reported at about 3 per cent. I suspect that when, years from now, we have full figures we will see that it is around 4 per cent. That figure would be consistent with the PMI numbers, which are also exceptionally strong.

Now think about personal confidence. Ask people about their personal finances and the figures have been strengthening. These are now decently positive, except somewhat surprisingly for the 45-55 age group, giving some credence to the notion of a squeeze on the middle-aged, if not necessarily the middle-earners. But ask people about housing and sentiment is still negative, though a lot less so than a year ago.

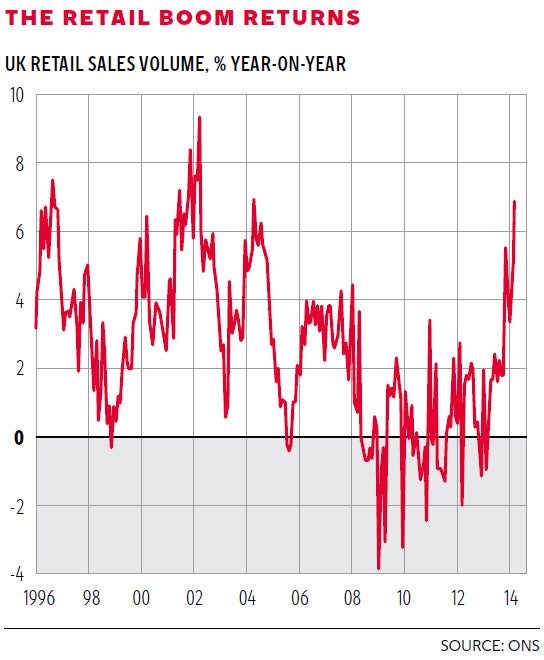

Moral: look at what people do, not what they say. We caught a glimpse of what people are doing with their money yesterday, with the retail sales figures for April. These were up 6.9 per cent in volume on April last year, which, as you can see from the graph, is the highest since spring 2004. True, the retail sales numbers jump around quite a lot, there was Easter and a bout of good weather, so these strong numbers probably overstate what has been happening. Let's say the underlying rise is only 5 per cent. That is still eye-wateringly strong. Online sales were up 25.1 per cent; department store sales were up 9.2 per cent; and the only significant area where sales were down was fuel stations.

So how is it that retail sales are rising so fast when pay is still just behind inflation? There are two main drivers, maybe three.

One is that there are a lot more people, about 750,000, at work. Obviously if there are more people at work, we have more money even if pay has been stagnant.

The second is that reported wage increases may not be picking up what is happening. For example, the self-employed are now 15 per cent of the workforce but their pay is not included at all in the earning figures. Nor are the profits of small businesses. During the downturn this segment of the workforce was probably more squeezed than those in regular employment, so it is possible that at that stage of the cycle earnings fell by more than the figures stated. Now the reverse is happening.

And the possible third? It is that the grey economy, the cash-in-hand economy, has grown relative to the official and fully taxed economy. That would be consistent with the evidence on VAT receipts, which have been OK but in the year to March were up only 4.5 per cent. Knock off inflation and you get measured consumption up by less than 3 per cent in real terms, or only 2 per cent if you deflate by the retail price index.

The inescapable point here is that the boom in consumption is picking up pace. You can crawl over the numbers but the detail is less important than the big story. There is not just a property boom. There is also a consumption boom. It has been running in the car market for two or three years, helped by easy and cheap credit and the desire to switch to more fuel-efficient models. Now it has broadened into retail sales.

In a normal world the response would be a rise in interest rates. The housing market needs one, for while the various prudential changes (for example those announced by Lloyds Bank) will curb it a bit, there is so much cash sloshing around that the only effective way to cap price rises will be a tighter monetary policy. We can see from the Bank of England minutes that the MPC is starting to move in that direction, though as yet no members have voted for a rise. The debate has been whether the first increase will be in the autumn, early next year or later next year. This has all become a bit tedious. I suspect that in the end the decision about interest rates will take itself. It will become screamingly obvious that the Bank has to move, probably because it will become clear that the inflation cycle has turned upwards again, and that will be that. Meanwhile the foreign exchange markets are busy tightening policy by jacking up the pound. It went briefly above $1.69 yesterday and once it goes through $1.70 expect it to move fast towards $1.75.

This will all, I fear, become rather political. British voters like a strong pound. They punish governments that devalue and reward those that revalue. If in addition real wages start to rise strongly (and that means actual real wages, not official earnings figures) and if the rise in interest rates is delayed, that will be three plus points for the Government.

Add in rising house prices (good for the Government) and you can begin to see quite a favourable outlook, on purely economic grounds, for the Coalition.

It would be silly to take one set of numbers, for example these retail sales, and say this is good news in electoral terms for the present incumbents. But it can't be bad news.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies