The story of the spring Budget 2017 explained in seven charts

There was very little change in the general picture since the Autumn Statement in November, when there was a significant deterioration due to the fallout from Britain’s vote to leave the European Union

Sign up to our free Brexit and beyond email for the latest headlines on what Brexit is meaning for the UK

Sign up to our Brexit email for the latest insight

Philip Hammond will hold one autumn Budget a year from 2018, meaning that this was the last spring Budget.

That means the tradition has gone out with a whimper rather than a bang as far as the economic and public finance forecasts are concerned.

For in Wednesday’s Budget there was very little change in the general picture since the Autumn Statement in November, when there was a significant deterioration pencilled in by the Office for Budget Responsibility due to the fallout from Britain’s vote to leave the European Union.

Here we tell the story of the Budget in seven charts, provided for The Independent by Statista.

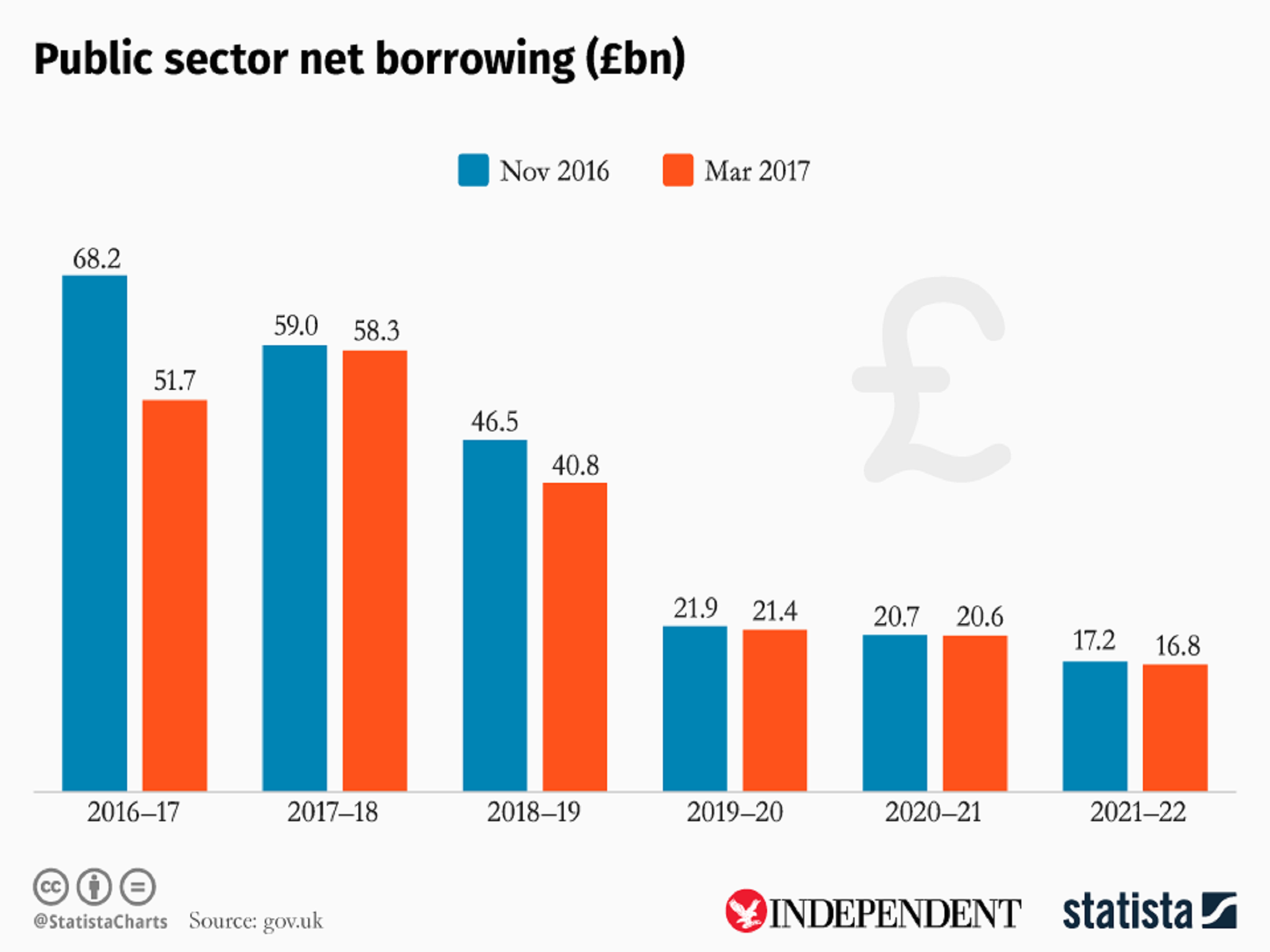

Borrowing down in the near term…

There was much anticipation of a better picture on public borrowing relative to November.

And the Office for Budget Responsibility delivered that in its outlook for the current financial year by slashing its borrowing estimate from £68.2bn to just £51.7bn.

However, the OBR has concluded that this is mainly a one-off benefit due to various technical factors affecting the tax take this financial year, such as changes to the timing of the recognition of corporation tax receipts and individuals shifting their income into different tax years.

The OBR therefore expects borrowing to rise again to £58.3bn in 2017-18.

The profile of annual borrowing is lower in 2018-19 than expected in November. But for the final three years of the forecast it is almost identical.

All the various spending and taxing measures in Mr Hammond’s Budget – from the additional money for free schools to the increase in National Insurance contributions from the self-employed – are small in the overall context of the public finances and broadly balance out over the next five years.

...a small borrowing revision in the scheme of things…

Overall the OBR thinks the Government will borrow £24bn less over the next five years than it anticipated in November.

That’s certainly positive for the public finances, but it doesn’t come close to reversing the massive £122bn upward adjustment in its borrowing forecast in the wake of the Brexit vote. The OBR attributed around £59bn of this deterioration directly to the Brexit result.

There have been several other larger downward revisions in borrowing forecasts between fiscal events in the past. In December 2013 the outlook improved by £67.8bn. This latest improvement is nothing out of the ordinary.

…the Chancellor has room to meet his fiscal target…

Philip Hammond’s new fiscal mandate is for cyclically-adjusted public sector net borrowing to be less than 2 per cent of GDP in 2020-21.

The OBR’s forecast for borrowing in that year is only 0.9 per cent of GDP.

This implies that the Mr Hammond could borrow around £23.5bn more in that fiscal year and still be (just) within his self-imposed borrowing mandate.

The Treasury has been briefing that the Chancellor is keeping this leeway, rather than using it up now in spending or tax cut promises, in case the economy deteriorates further over the next few years due to Brexit uncertainty and he is forced into borrowing more to stabilise the economy.

…the debt to GDP profile is modestly better…

Modestly lower annual borrowing in the latest forecasts also helps keep the national debt to GDP ratio under control.

The ratio is on a slightly lower path according to the OBR relative to November, peaking at 88.8 per cent of GDP and declining to 79.8 per cent in 2021-22.

With the national debt also seen falling between 2019-20 and 2020-21 (from 86.9 per cent to 83 per cent) the Chancellor also meets the “supplementary” part of his new fiscal mandate.

…GDP growth is higher this year, but the improvement does not last…

The 2017 growth forecast has been upgraded to 2 per cent, up from 1.4 per cent in November, something that has cheered Brexit supporters.

This is mainly due to stronger growth in the second half of 2016 in the wake of the Brexit vote than the OBR expected.

But this is not seen as a lasting improvement.

The OBR has downgraded its growth forecasts slightly in 2018, 2019 and 2020.

And these growth rates are all below what the OBR was forecasting before the Brexit referendum.

Moreover, the detail of the OBR’s forecasts shows that the level of real GDP by 2021 is actually projected to be slightly smaller in 2021 than it projected in November (£2,044bn versus £2,051bn).

Real GDP per capita growth over the next five years has also been downgraded by the OBR.

…the productivity growth forecast is still weaker due to Brexit…

The foundation of all the OBR’s forecasts is its estimate of the potential productivity growth of the UK economy (measured as output per hour).

This essentially refers to the speed that the economy can grow without setting off excessive inflation.

This potential estimate was downgraded in November, with the OBR blaming the negative impact of weaker investment due to Brexit.

And this bleaker outlook has not changed since November, confirming that the OBR has not had a change of mind over the harmful economic impact of the UK leaving the European Union.

…real wages are set to be squeezed hard this year despite the GDP growth upgrade

The OBR projected a big squeeze on average real earnings in November due to a jump in inflation stemming from the slump in the pound since the referendum.

That does not change much in this forecast.

Average earnings growth is expected to be moderately higher in 2017.

But the forecast has been downgraded for the four subsequent years.

Combined with essentially the same inflation forecast as in November (with inflation peaking at 2.4 per cent of GDP) the OBR’s projections imply real wage growth almost disappearing this year and rising by just 0.4 per cent in 2018.

All this means that, despite the headline upwards revision in overall GDP growth in 2017, living standards are set to come back under serious pressure for the next two years as we prepare to leave the EU.

The Resolution Foundation think tank estimates that average earnings by 2021 will be £1,220 a year lower than forecast by the OBR before the Brexit referendum.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies