The Big Question: What was Roosevelt's New Deal, and is something like it needed today?

Why are we asking this now?

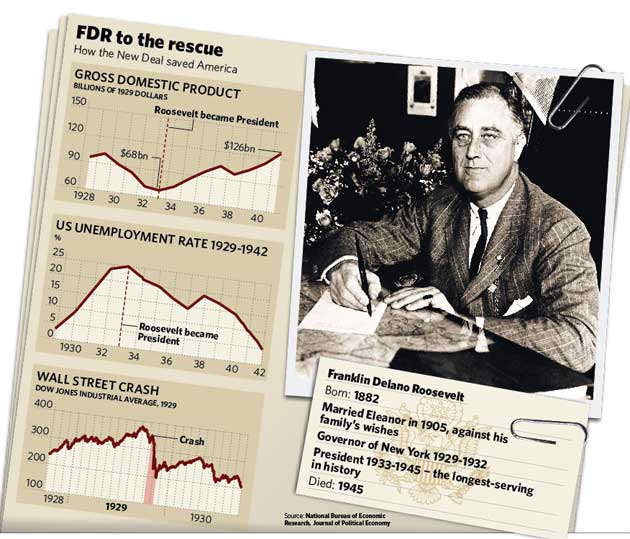

The current financial and economic turmoil is increasingly likened to the crisis that began with the Wall Street crash of 1929, paving the way to the Great Depression of the 1930s. That slump, the deepest and most prolonged economic downturn of modern times, continued through much of the decade. The response of Franklin Roosevelt, who became President of the United States in March 1933, was the New Deal. But the US economy did not truly recover until the country's entry into the Second World War.

What was the New Deal?

The New Deal is shorthand for a host of government programmes introduced by Roosevelt between 1933 and 1938. The phrase itself originates in FDR's acceptance speech at the 1932 Democratic convention in Chicago, in which he promised "a new deal for the American people". The various measures included support for, and reform of, the collapsing banking industry, a new stock market regulatory agency, moves to boost wages and prices, the creation of massive public works projects and – perhaps most important of all – the launch of Social Security, the American equivalent of National Insurance in the UK.

Taken together, they not only constituted a "New Deal" to help ordinary Americans. They also initiated a new era of government activism, in terms of both intervention and regulation of the economy. Many New Deal programmes still exist, part of a safety net that even today's most laissez-faire rightwingers in the US would not dare touch.

Why was it introduced?

The economic plight of the US and other countries in the early 1930s is almost impossible to imagine today. Recession of some kind was inevitable after the collapse of the speculative bubble in 1929 crash (caused by an excessive run-up in share prices, not house prices as between 2000 and 2006). But the downturn was made far worse by a tit-for-tat international trade war, started by the infamous Smoot-Hawley Act of 1930 boosting US import tariffs, and by the failure of the Federal Reserve, America's central bank, to pump money into the system and prevent a panic run on banks. When FDR took power, the US unemployment rate was almost 25 per cent, its farm sector was in ruins and industrial output was 30 per cent lower than before the crash. Drastic measures were needed to restore confidence, on a scale only the government could provide.

Are there political parallels?

In the US there are plenty. Then as now, a long spell of Republican dominance was approaching an end. Even if John McCain snatches victory in November, it will not alter the fact that the conservative movement that took control with Ronald Reagan's victory in 1980 has run out of steam. In 1932, Roosevelt's landslide defeat of Herbert Hoover signalled the end of a long period of Republican ascendancy. Today, the stars are similarly aligned for the Democrats (though whether the country is ready for Barack Obama is another matter entirely). George W. Bush has been mockingly dubbed "George Herbert Hoover Bush". America is shifting to the left, and government is back in fashion. The debacle on Wall Street has cemented a widespread view that free-market capitalism needs reining in. As in 1932, the pendulum in 2008 is shifting back towards greater regulation and intervention.

And what about economic parallels?

Conceivably, the present turmoil could result in a second Great Depression. But although history and economic crises past provide lessons we ignore at our peril, they never repeat themselves exactly. These are painful times, but (not yet at least) a patch on 1932. The US economy, which grew at 3.3 per cent in the second quarter, is technically not even in recession yet. Unemployment stands at 6 per cent, not 25 per cent, and industrial output is down 1 per cent on 2007, not 33 per cent.

In the 1930s, the crisis was compounded by falling prices, as governments sought to balance budgets by deflationary measures, even as economies were contracting. Today, deflation is not on the horizon; indeed, falling commodity and farm prices are a welcome relief, not a threat. The problem is not a lack of money in the overall economy, but of banks' reluctance to lend money to all but the most trustworthy borrowers.

So we've learnt some lessons from history?

Most certainly. In the 1930s, the Smoot-Hawley Act imposed a trade war on top of an economic downturn. Despite the stalling of the Doha round of trade liberalisation, and widespread criticism of globalisation, there is scant risk of a similar bout of beggar-my-neighbour protectionism today.

Meanwhile Ben Bernanke, the current Federal Reserve chairman and former Princeton economics professor, is a lifelong student of the Great Depression. He has publicly criticised the Fed's performance then, and will not make the same mistakes now. By allowing Lehman Bros to go under, the US government signalled that the banking system must purge itself of the bad mortgage toxin. But with its moves to pump in liquidity, the central bank has signalled it will not permit the system itself to go under.

So the US can get by without a New Deal?

Not necessarily. Everything depends on the extent to which the crisis impacts on ordinary people. Every sign is that America, like Britain, is sliding into recession. In the best-case scenario, growth will restart some time in 2009 – in the US, once house prices hit bottom and stabilise, and banks feel confident again to lend the money they are hoarding to protect themselves against the storm. In that case, as credit markets return to normal, the downturn will have been relatively brief. But if recession drags on, the clamour for New Deal-style programmes will grow. Indeed some are already demanding the government use the opportunity to boost spending on America's crumbling public infrastructure – roads, bridges, railways and so on – to create new jobs and spending power that will be pumped back into the economy.

What are McCain and Obama saying?

Inevitably, their takes on the crisis differ. For John McCain, the mess has been created by greedy, out-of-control banks and mortgage lenders. For Obama and the Democrats, the crisis is an indictment of an entire Republican economic philosophy which looked out only for the rich, and blindly insisted that markets always knew best. But they agree on one thing – the need for tougher regulations, to prevent a repeat. In that sense at least, and whatever the severity of the downturn, a new New Deal is certain.

So is this another Great Depression?

Yes...

* The banks may have money, but how to make them lend it?

* Financial globalisation guarantees the crisis will spread, whatever countries do.

* This bubble was 20 years in the making, twice as long as the one which burst in 1929

No...

* The crisis in the real economy is nowhere near as severe. The US is still growing.

* Regulators have learnt their lessons, and won't make the mistakes of the 1930s again

* The world economy is less US-centred, reducing the risk of contagion

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments