The Independent's journalism is supported by our readers. When you purchase through links on our site, we may earn commission.

Care home rooms offered for sale to private investors on 'buy-to-let' basis

Exclusive: Hundreds of speculators promised returns of 10 per cent a year, squeezing funds available for actual care

Private investors are being enticed to purchase rooms in UK care homes on a ‘buy-to-let’ basis with the promise of large profits and rental income, an investigation for The Independent reveals.

The Bureau of Investigative Journalism has found hundreds of rooms being offered for sale for as much as £85,000 each. They offer “guaranteed” rental income of around 10 per cent annually and a total return on investment of up to 188 per cent over 10 years.

The largest player in the market is a company whose managers include a struck-off solicitor, a disqualified director and a chief executive who was once the sole director of a company that held a strip club licence – and who says his involvement in the sector will allow him to buy fast cars and diamonds for his wife.

Such buy-to-let room schemes are not regulated by the Financial Conduct Authority, while the Care Quality Commission, which oversees standards in care homes, says it does not have responsibility for providers’ financial sustainability.

Servicing such high fixed returns could squeeze funds available for providing the actual care. Residents could also have to move if the care homes failed to pay their debts to investors and were forced to close.

Already half of Britain’s care homes are at risk of closure due to council cutbacks and planned increases in the National Minimum Wage, while a string of care homes have gone out of business in recent years.

In response to the Bureau’s findings the former Care Minister Norman Lamb said: “My concern is that if you base the future of care on potentially volatile schemes that could crash then there are knock on consequences for the elderly people who receive that care. That’s what we need to avoid.”

The Bureau’s investigation focused on the Yorkshire-based MBi group which is currently registered to run three care homes in the North of England and is rapidly expanding.

The company has at least seven more care developments in the pipeline.

The company is also currently engaged in a significant marketing campaign, including sponsoring a “Dementia Cafe” and grassroots football scheme at Leeds United.

But the Bureau’s investigation has raised concerns about the accuracy of MBi’s marketing materials and some of its business managers’ track records.

The charity Dementia UK and Lancashire County Council have separately told the company to remove details from MBi marketing materials.

Buy-to-let beds

Q | How does the scheme work?

A | Investors hand over around £85,000 for a 125-year lease on a “suite” in a care home, often which has yet to be built. The money helps fund the construction of the home. MBi Group says that investors will have full legal title registered at the Land Registry.

Q | So what do investors get for their money?

A | MBi claims that after two years investors will see a return on their money of 12 per cent a year, which is £10,200 a year on a £85,000 suite over 10 years.

Q | This all seems like a lot – is it too good to be true?

A | MBi says it works as “an alternative to expensive bank funding” and that is why it can pay such high rates of return. But the scheme is not regulated by the Financial Conduct Authority and some have warned that such rates may be unsustainable. Care homes tend to pay the majority of staff little more than the minimum wage, which is due to rise significantly over the next four years. This will put big pressures on finances. Like with any investment, those putting money in could lose it all if the care home company goes bust.

Dementia UK, whose chief executive Hilda Hayo gave a presentation at one of MBi’s sales pitches in May 2015, claims the company made inaccurate statements about the charity’s relationship with it and had committed what it regarded as a “significant breach of trust”.

Meanwhile Lancashire County Council has demanded MBi remove the authority’s official logo from a website that it said wrongly claimed they were in a joint venture together.

MP Ben Bradshaw, the former Labour minister who sits on the Commons Health Select Committee, said the Bureau’s investigation raised “serious questions” for ministers and regulators.

“We are dealing with elderly people, often at their most vulnerable, and the record of some of those involved in this business [MBI] does not instill confidence,” he said.

MBi markets itself as a “knight” riding to the rescue of Britain’s growing elderly population by building and managing quality nursing and residential homes.

Through an email marketing campaign and investor seminars the company has persuaded investors to buy leases on rooms in its homes for up to £88,000.

Investors’ leases are registered with the Land Registry and the company guarantees them up to 12% annual rental income over 10 years – as well as pledging to buy back the rooms for a 25 per cent mark-up at the end of that period.

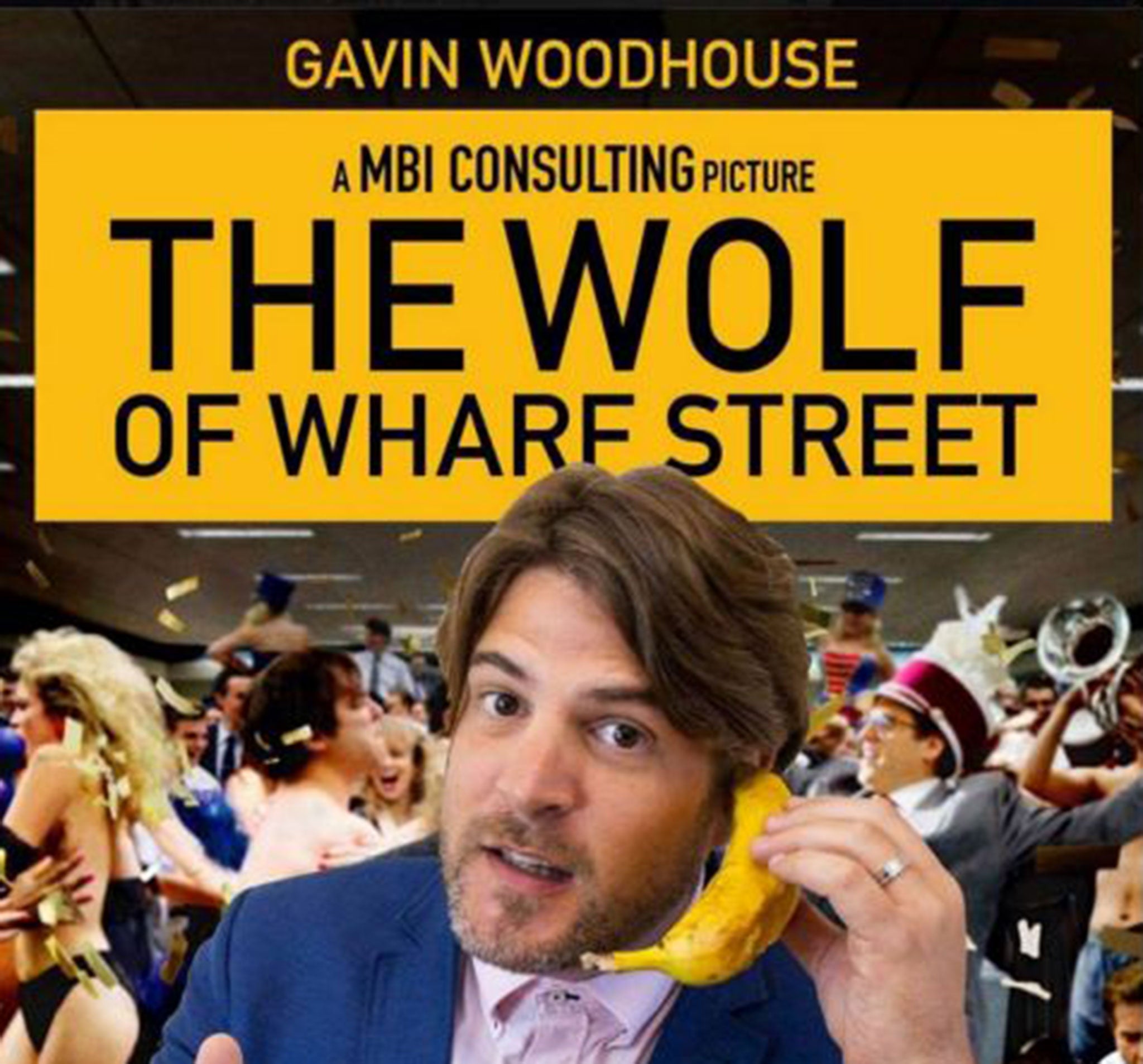

Gavin Woodhouse, the charismatic chief executive of MBi, last year posted a jokey Facebook image of himself posing as the notorious Wolf of Wall Street film character and describes himself as an “anarchist” who "hates" banks.

He says because MBi’s business model cuts out the need for bank loans, costs are lower.

However the Bureau has discovered that MBi has been taken out short-term loans from individuals or small credit companies secured against some of its development schemes. MBi’s loans include one for £224,000 at a 30% per annum interest rate over three years.

MBi’s lawyers told the Bureau: “Our clients do not have any bank loans. Short term loans are sometimes taken out and secured against the freehold title. This is standard business practice.”

The company’s business model has won the support of Graham Rowan, who describes himself as a “wealth coach” and who runs the “Elite Investor Club” for ambitious small private investors.

The club hosted a “Dementia Care Mini Summit” for potential investors in May, at which Woodhouse said: “When we go in and talk to people like Lancashire [County] Council … we’re seen like a knight on a horse because nobody else can afford to develop, because they have the big bank loans to service.”

At the meeting, which was filmed by the organisers, Woodhouse said his company had 750 rooms under development, ownership or renovation and would have 1,000 by the end of 2015.

He was aiming to acquire 10,000 beds in 10 years and then sell up, he added.

“I still have a demanding wife, still got to buy the diamonds and fast cars at some point in my life – the exit strategy will allow me to do that,” he said. “It will change my life when we sell it.”

MBi has recruited a team of respected social care experts who operate through a separate company, MBi Social Care Limited – part of the MBi group – to manage the homes.

However, it is the background of some other people involved with MBi and its risky business structure that has raised concerns.

MBi’s chief commercial officer is former Oldham-based property lawyer Alan Cockburn. He was struck off after a Solicitors’ Disciplinary Tribunal hearing in 2013 for what it said was “the most serious misconduct”.

The tribunal found that he had acted for the buyer, seller and lender in the same transaction and caused the Yorkshire Bank to lose hundreds of thousands of pounds. Cockburn had failed to register the bank’s mortgage loan against a commercial property – meaning the loan was unsecured – then allowed the money to be “dissipated”.

It was the second time he had faced disciplinary action, having been fined for misconduct by the tribunal three years earlier.

Until recently Cockburn was referred to on MBi’s websites as “contracts director”. Lawyers for Cockburn told the Bureau he did not manage client contracts however.

“Our client is a commercial director, not a contracts director,” his lawyer said. “He is not employed in a legal capacity. The fact that he was struck off the Solicitors Roll is a matter of public record.”

The Bureau has also examined the business background of MBi chief executive Gavin Woodhouse. Prior to founding MBi in 2011 he was a director of several other companies.

Companies House lists Woodhouse as director from late October 2012 until May 2013 of Harjen Limited, which held a sexual entertainment licence for the Leeds strip club, Wildcats, throughout that time.

Woodhouse’s lawyer said his client had not been involved with the management of the strip club and that the dates of his directorship listed at Companies House were incorrect.

The lawyer said Woodhouse had “immediately resigned” when he found out about the business.

He added: “Mr Woodhouse was interested in purchasing another part of the business. Following preliminary enquiries he decided not to proceed.”

Woodhouse was also listed as a director of Eventfield Ltd, which was linked in an employment tribunal to the controversial collapse of Waremart, a Halifax discount store, in 2010.

Woodhouse’s lawyer said his client had been “wrongly appointed” as director and had had no involvement in the company.

He was also the director of a finance firm which failed during the recession in 2009.

Woodhouse’s lawyer said: “Many banks/finance companies were wound up during the financial crisis.”

The lawyer added: “Mr Woodhouse has held short-lived directorships of two businesses that left debts when they were wound up. He was appointed without his knowledge and/or not removed when he should have been.”

“[Woodhouse] has co-operated fully with the Insolvency Service who do not intend to take any further action.”

The backgrounds of two other MBi managers, Chris Longfellow, head of client support and project coordinator, and Ben Dews, agent development manager, have also raised concerns.

Dews was disqualified in 2015 from acting as a director after the Insolvency Service found HMRC had lost more than £500,000 in unpaid VAT as a result of the way one company he had been a director of had been managed three years earlier.

Dews’s lawyer told the Bureau his client “did not have day to day conduct” of the insolvent business and “may be appealing the decision to disqualify him”.

And a 2014 report by insolvency practitioners into a company in which Longfellow had been a co-director said they were investigating “possible misfeasance”. The directors had not responded to the practitioners’ requests for assistance, the report noted.

Liquidators Begbies Traynor told the Bureau its investigation into the company was ongoing.

The Bureau asked Longfellow if he had co-operated with the liquidators since 2014. His lawyer said he “is not aware of any ongoing investigation by insolvency practitioners for ‘possible misfeasance’”.

MBi has donated the ground rent from one of its homes to Dementia UK and fundraised for the charity.

The charity’s chief executive, Hilda Hayo, gave a presentation at the Elite Investor Club meeting in May, where the buy-to-let deals were pitched to potential investors.

She told them Dementia UK had a “good relationship” with the company and that she was “positive” MBi would be “stamping out poor practice [in the care sector] with the plans they’ve got for the future”.

However since then the charity has claimed there has been “a significant breach of trust” by the company. The charity said MBi had printed “factually incorrect” information.

It told the Bureau it had terminated its relationship with MBi.

A Dementia UK spokesman said Hayo had not realised that May’s meeting, at which she received a fundraising cheque from MBi staff, was going to be a sales pitch.

Following the May event the charity discovered its logo had been used on a national newspaper advertisement for one of MBi’s investment schemes.

Hayo immediately asked MBi to remove all references to Dementia UK from its marketing materials.

However MBi websites and promotional materials seen by the Bureau months later stated that Hayo was a member of its advisory board and that Dementia UK and its specialist Admiral Nurses were training the company’s staff.

The charity’s spokesman said Hayo had declined MBi’s invitation to sit on its advisory board and that Dementia UK “is not doing any training for MBi at all, either from central HQ or by Admiral Nurses”.

He added: “As a significant breach of trust has occurred – Hilda’s good nature was abused and MBi has printed factually incorrect information about both Hilda and Dementia UK – Dementia UK has terminated its relationship with MBi.”

MBi’s lawyer said the company denied the charity’s allegations, including that of a breach of trust. The lawyer said Hayo had been informed that investors would be present at the May meeting and that she had attended their events “willingly”. MBi has now removed all references to Dementia UK from its websites.

Philip Challinor, a director of financial advisors Chatfield Private Client, said of the care home room-based buy-to-let model: “I wouldn’t touch it with a barge pole. You don’t get those sort of returns without taking a lot of risk.”

Care sector financial expert William Laing described the returns proposed by MBi as “excessively optimistic”.

MBi’s lawyer said MBi was “offering a boon for a struggling sector” and that the company “has put in place and adheres to the highest standards of governance.”

He added: “Our client uses its best endeavours to ensure that its marketing materials are correct.”

Regarding the investment schemes, the lawyer said the investments do not need to be regulated by the Financial Conduct Authority. He said the FCA had confirmed this.