Buried fees that can cost you a small fortune

Excessive investment fund charges could make a major difference to the amount you receive, warn Chiara Cavaglieri and Julian Knight

Excessive workplace pension charges are finally being tackled after government proposals for a cap on fees announced this week. However, fund investors putting their cash into individual savings accounts are still losing out to the tune of thousands of pounds due to such fees experts warn.

The Government is consulting on workplace pension scheme charges which could see the introduction of a cap set as low as 0.75 per cent, but critics have already pointed out that this only addresses one element – the headline annual management charge – and does nothing to tackle the lack of transparency on other fees. The real issue is that charges on both pension funds and investment funds such as unit trusts and open-ended investment companies can be easily hidden elsewhere.

It's no exaggeration to say that even experts struggle to assess the full extent of all the fees involved, and until the true cost of investment funds is made clear to investors, they cannot make informed decisions.

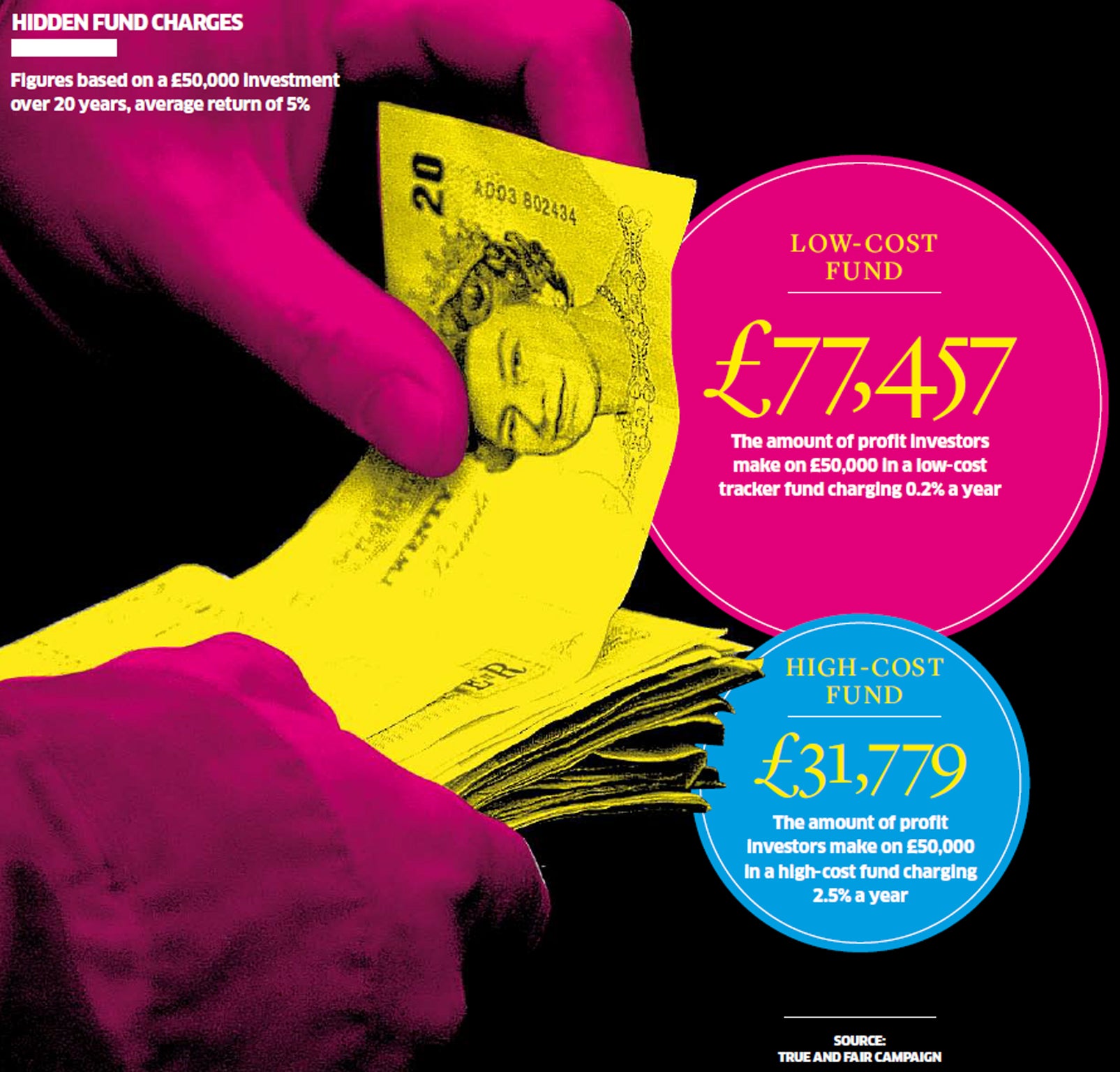

The potential impact of these charges is startling. Gina Miller, founder of the True and Fair Campaign which is calling for transparent fund charges, explains that if an investor put away £50,000 for 20 years, based on a return of 5 per cent, they would pay as much as £50,885 in fees (with total charges of 2.51 per cent) for some actively managed funds.

"If that individual bought a similar tracker fund they would pay as little as £5,206 in fees based on a true total cost of investing of 0.21 per cent. So the active fund is 12 times more expensive," she says. "At the end of the 20 years, the investor in the expensive, actively managed fund would have made in their pocket £31,779 – the investor in the tracker fund would have made £77,457".

Fund managers have various methods for taking their chunk of your money, whether it's an initial fee covering set-up costs (typically around 5 per cent of your overall investment) and an annual fee for ongoing running costs (the average fund charges 1.5 per cent). And this is only the beginning, because the "ongoing charges" figure or total expense ratio (TER), which includes the management charge as well as additional expenses associated with operating a fund (administration costs, auditor fees and legal costs), is taken directly out of the fund.

But even this isn't the whole picture as the TER can sometimes represent less than half of the full costs incurred. There are many more charges which could be eating away at any gains because fund managers incur various transaction costs, commissions and transfer taxes when they are buying and selling assets in the fund – all of which are hidden in the performance of the fund.

A number of unit trusts also add on complex performance fees of between 10 and 20 per cent of the profits, which kick in when the fund exceeds a particular benchmark. Some investors might be happy to pay managers who hit their targets, but it's worth remembering that there is no compensation for underperformance and it can be tricky to put any perceived success into context because there are no standard benchmarks to compare to.

The worst scenario in terms of high charges is advisers who sell their own funds and use fund of funds arrangements (where one fund manager picks a whole range of funds to invest in on your behalf). For example, Towry imposes its own initial charge of 1.5 per cent and an annual management charge of 2 per cent, but you also have to factor in the annual charges of each fund on top.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

There are signs of improvement, starting with a ban on commissions to advisers following the retail distribution review, which came into force at the start of the year, and a move towards "clean" share classes, which don't pay commissions to platforms. Some firms have also begun to disclose costs on their website, prompted by the Investment Management Association.

The Financial Conduct Authority has also called for greater transparency in the asset-management sector, and chief executive Martin Wheatley has said we need to see that managers are "putting their clients' value for money, good returns, and transparency at the heart of how they do business".

Many experts also maintain that charges cannot be the primary factor. What really matters is the performance once any charges have been deducted and Jason Hollands of independent financial adviser Bestinvest says that the very best fund managers may well be able to justify above-average fees.

"In our view, excessive fees are those where the manager is unable to demonstrate value added net of fees," he says. "These would include persistent underperformers, supposedly actively managed funds charging full fees but in reality operating as closet trackers and also certain index trackers that are levying high fees compared to competitors."

Investors are also urged to vote with their feet and move their money into a vehicle offering strong performance and competitive fees.

Fund supermarkets or discount brokers such as Bestinvest, Cavendish Online, Chelsea Financial Services and Hargreaves Lansdown will usually waive the initial fee and give back a portion of the management charge. You can also check the True and Fair campaign fund cost calculator which covers 7,500 investment products, working out the total cost as a single figure with an estimate of the potential returns after these costs have been deducted (trueandfaircalculator.com).

Tracker funds and exchange-traded funds are a popular alternative as these have much lower charges than actively managed funds (some have a TER of as little as 0.15 per cent) and you don't have to worry about transaction costs either because they buy assets within an index.

Patrick Connolly of IFA Chase de Vere says: "While there are some good-quality actively managed funds which justify the level of charges they make, too many managers charge too much and deliver too little. This is why we have seen an upturn in the use of passive investments and why this is a trend which is set to continue."

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks