Coronavirus: What will it mean for our jobs and livelihoods?

Could it mean mass layoffs as in previous recessions? Should we expect wage stagnation?

Global economic bodies like the OECD and the International Monetary Fund are slashing their macroeconomic growth forecasts in response to the Covid-19 pandemic.

There’s a possibility of a global recession according to some analysts.

But how would that economic damage be experienced in ordinary people’s lives?

Could it mean mass job layoffs like in previous recessions? Should we expect wage stagnation?

Or is it possible that, if mortgage repayments are suspended by banks for the duration of the crisis, some people could actually find themselves better off? What about falling oil prices?

How will the economic fallout from the coronavirus impact be experienced?

Job losses

In previous recessions tens of millions were made redundant as consumer and business spending came to a sudden stop and companies went bust as a result.

During the 2008 financial crisis recession the jobless rate in the US doubled from 5 per cent to 10 per cent. In the UK it went from 5 per cent to 8.5 per cent.

Could that happen again? Certainly in theory.

If you put large populations in lockdown they will be unable to spend and that will place local companies – especially those with debt repayments to make – under severe financial strain and they may well go bust and make their employees redundant.

Firms could also be at risk if their workforces fall sick at the same time.

In the US there are already reports of jobs going in the transport and tourism sectors.

In the UK the domestic airline Flybe has gone into administration, threatening 2,300 jobs. Its bosses highlighted a slump of bookings due to coronavirus fears.

The UK government unveiled a raft of business support schemes, from tax relief to direct grants in the Budget earlier this week. Germany did something similar on Friday.

Other countries are very likely to roll out their own schemes.

The question is whether these schemes – never tested before – will be sufficient to prevent a spike in insolvencies and the inevitable ensuing redundancies.

Wages

The post-financial crisis decade has been a bleak one for average wage growth.

In the UK inflation-adjusted wages only recovered their pre-2008 peak at the end of last year.

Things have not been much better for the median worker in the US on the wage front.

Even if governments are able to prevent a wave of redundancies economists will already be revising down the expectations for real wage growth.

Companies that are on the verge of insolvency due to a collapse in custom – or firms plagued by uncertainty about the general business outlook – do not tend to give above-inflation pay settlements to their employees.

Deflation

In a boom inflation – spiralling prices – have historically been the problem.

In recessionary conditions the problem is the opposite: the danger of falling prices as lack of demand leads to discounting by firms.

The 30 per cent collapse in the oil price this week may contribute to falling prices.

Ordinary people may experience this as fuel and groceries being cheaper than normal.

But if their incomes are under pressure from stagnant wages or from losing their jobs, price deflation will not translate into an overall increase in living standards.

Mortgage repayments

This week Italy announced that households’ mortgage payments to banks would be suspended after imposing its total lockdown on the country, recognising that if people cannot work they cannot repay their borrowings.

Expect similar policies – with governments putting pressure on banks to offer forbearance for missed payments – to be rolled out in other countries that go down a similar route of lockdown or enforced social distancing.

As with falling prices, though, this will not translate into a rising living standards because, although people might welcome a suspension of their repayments, they will also likely face damage to their incomes.

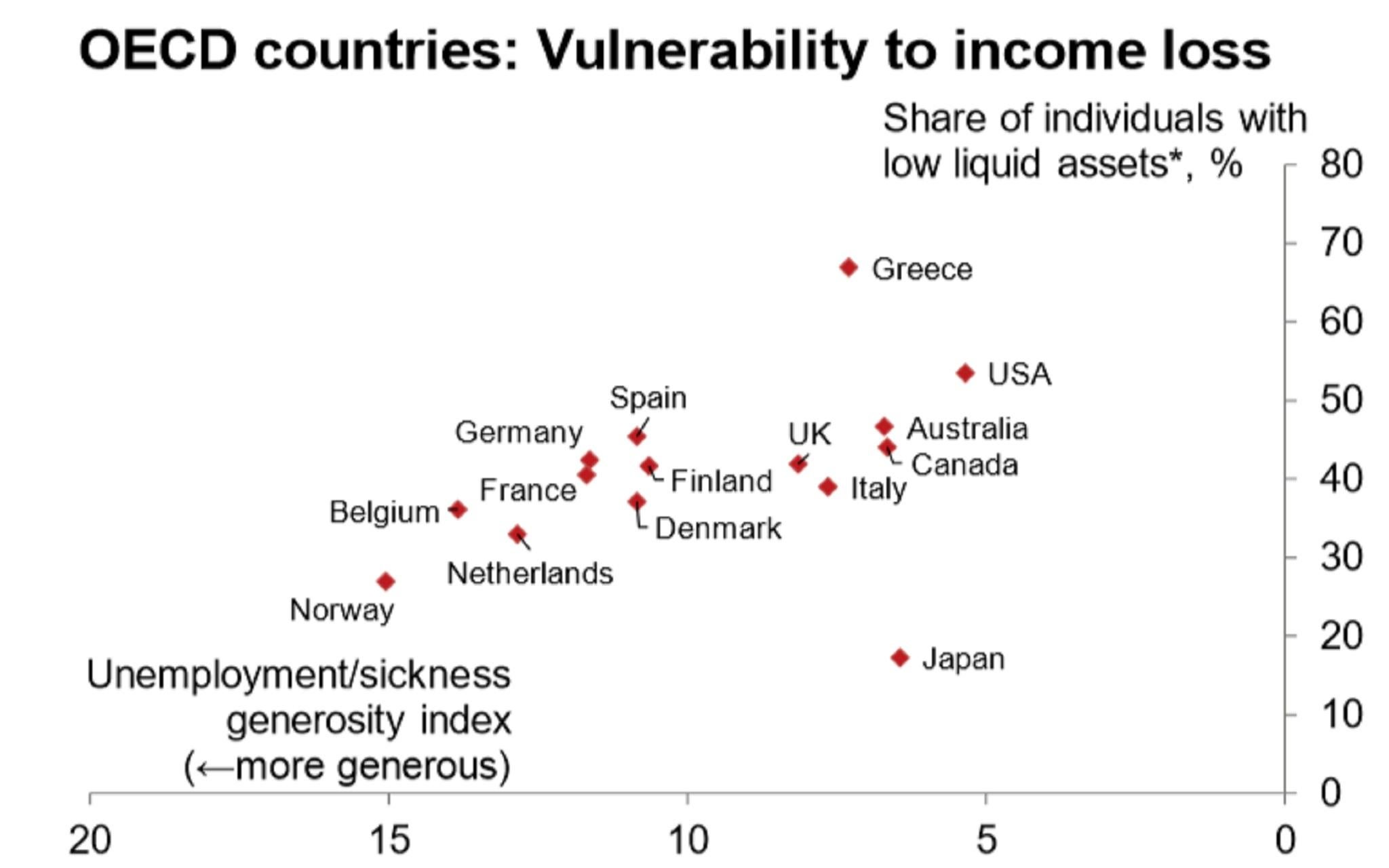

It’s important to bear in mind how many households are already financially vulnerable.

Around 40 per cent of individuals across the developed world countries of the OECD have insufficient money or saleable assets to support themselves at the poverty line for more than three months.

“Many workers will have very limited liquidity buffers to tide them over if they cannot earn,” says Adam Slater of Oxford Economics.

Their livelihoods may well depend on the willingness – and, crucially, ability – of their governments to provide them with welfare and support.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments