UK economy in grip of most feeble recovery on modern record, says IFS

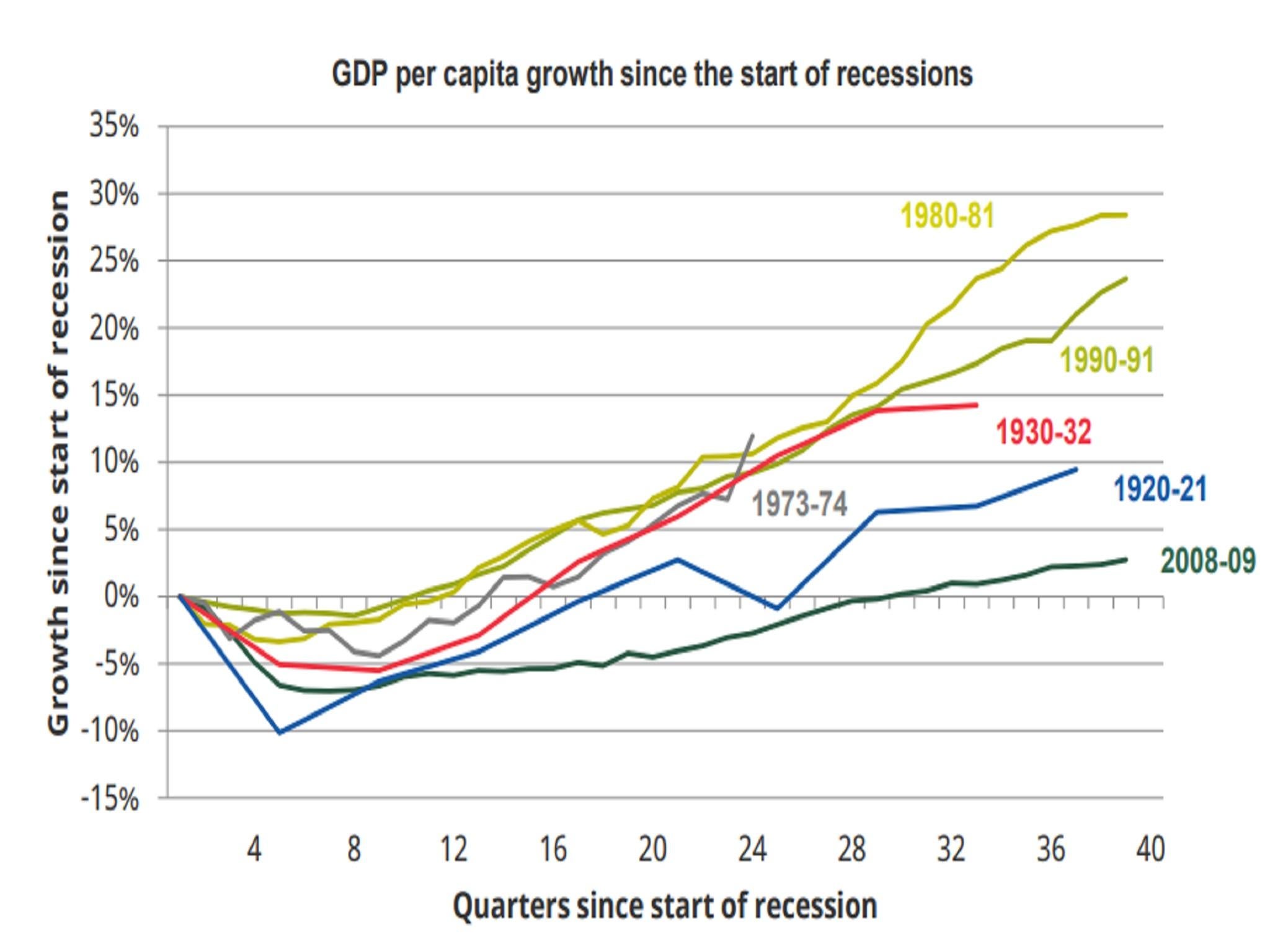

Analysing historic data on UK GDP per capita the think tank shows it has been weaker even than what followed the agonising slump of the early 1920s

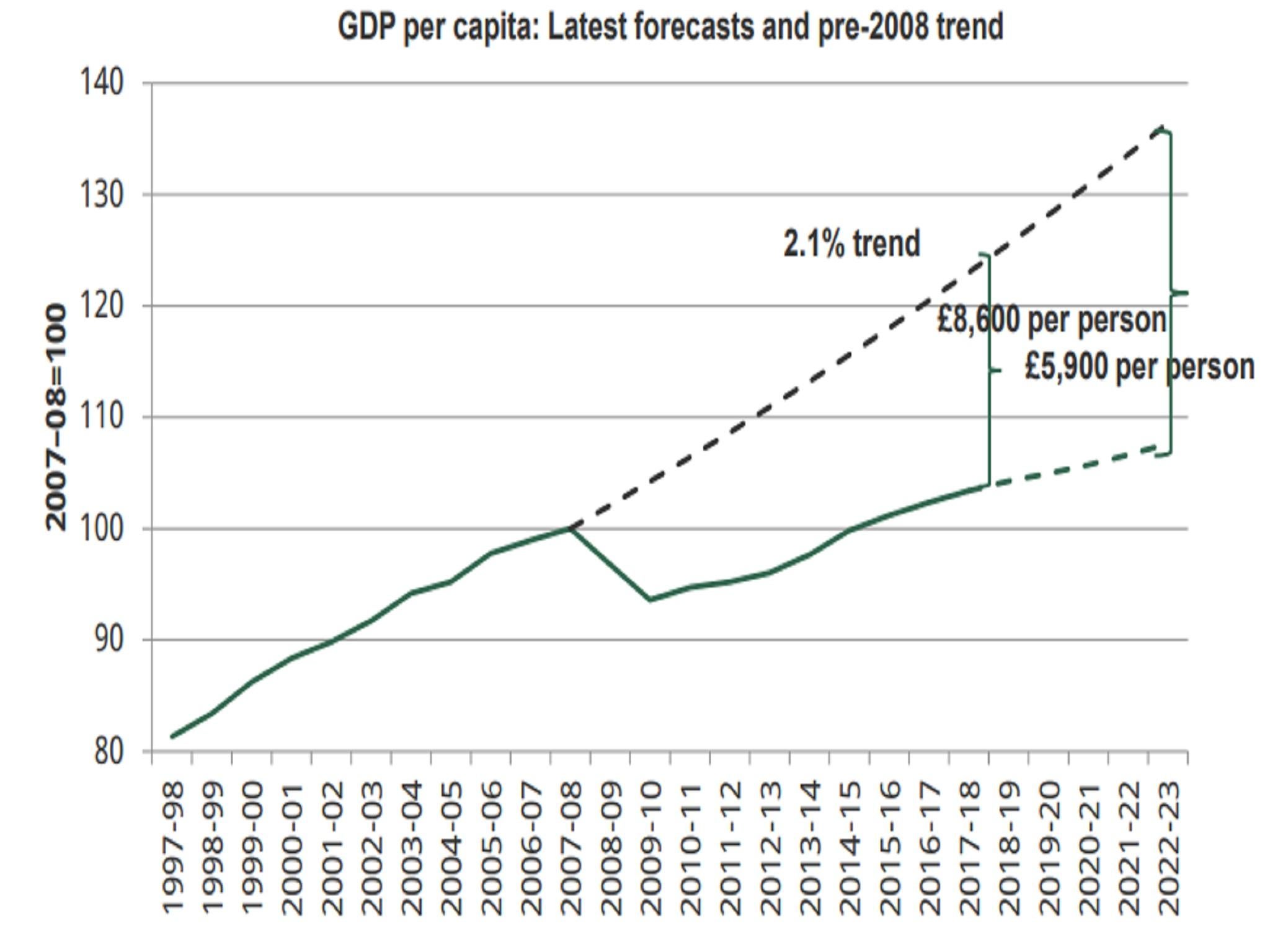

The UK has been living through the most feeble and protracted economic recovery in modern British history, leaving people on course to be almost £9,000 worse off on average by 2022-23 relative to the pre-crisis trend, according to calculations by the Institute for Fiscal Studies.

In its analysis of the Government’s Spring Statement on Tuesday, which contained no new tax or spending measures, the think tank took a longer term perspective on the performance of the UK economy in the decade since the UK economy first sank into recession in 2008.

It has long been noted that the UK’s recovery from that slump has been the slowest since the Great Depression in the 1930s.

But, analysing historic data on UK GDP per capita, the IFS showed on Wednesday that it has been weaker even than what followed the agonising slump of the early 1920s.

In that era output per person fell by 10 per cent, as global industrial overcapacity in the wake of the First World War ravaged once mighty UK firms, resulting in mass unemployment.

The UK recession after the global financial crisis was shallower, with GDP per capita falling by around 7 per cent as banks failed and global trade fell off a cliff.

Yet a decade after the 1920-21 recession UK output per person was more than 10 per cent higher than before the crisis.

Today it is only 3 around per cent higher than it was in 2008-09.

Weakest recovery on modern record

“The history matters,” said Paul Johnson, the IFS’s director.

“It matters in part because we should never stop reminding ourselves just what an astonishing decade we have just lived through and continue to live through.”

The UK has avoided the mass unemployment that scarred the 1920s and indeed employment has grown strongly since 2010, but the chronic weakness of UK GDP and productivity growth since 2008 is the reason why average real wages are still below where they were a decade ago – and are not set to return to their peak until well into the next decade.

The IFS also produced calculations showing that if the pre-crisis trend of GDP per capita growth had continued national income per person would today be £5,900 higher this year.

By 2022-23, on current official projections, the financial hit per person will grow to £8,600.

The cost per person

“Dismal productivity growth, dismal earnings growth and dismal economic growth are not just part of the history of the last decade, they appear to be the new normal,” said Mr Johnson.

The IFS’s analysis is sharply at odds with the claims by the Chancellor, Philip Hammond, who said at the House of Commons Despatch Box on Tuesday that there is “light at the end of the tunnel” for the UK economy.

Conservative MPs have been lobbying for public spending increases, after eight years of cuts, but the IFS calculated that in order to meet their party’s own target of balancing the overall budget by 2025 would require an additional £18bn of spending cuts or tax rises.

A number of explanations for the record weakness of the UK economy since 2008 have been offered.

Many have blamed premature austerity by the previous Chancellor, George Osborne, for suppressing aggregate demand before the recovery was secured.

Others suspect a secular slowdown in productivity growth, as the rate of technological advance across the developed world has fallen over the past 15 years.

Others have argued that official statistics are not capturing advances in output related to the digital economy.

Another explanation is the lingering impact of the global financial dislocation, with the UK particularly exposed through the City of London.

Asked by The Independent what the IFS’s view was on which of these explanations was likely to be correct, Mr Johnson said it was probably “a combination of all of those things”.

He added that particular domestic supply side failings, such as inadequate skills training and weak investment rates by UK corporations, had likely compounded the damage caused by weak aggregate demand.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks