Hamish McRae: Forecasts simply offer more questions

Economic View

If economic forecasts turn out to be so wrong, why do we bother with them? Just last week we had the Office for Budget Responsibility acknowledging that it had been too optimistic about growth this year – and too pessimistic about employment. Back in March, it thought the economy would grow this year, and now it thinks it will shrink by 0.1 per cent. But it thought that employment would be flat, whereas the economy has added half a million jobs. If in March you can't predict what will happen in the next nine months, what hope is there for forecasts two, three or more years out?

I am making this point not to beat the OBR, or indeed any other forecasters, over the head. It is still quite possible that its initial expectation that there would be modest growth this year will turn out to be right, for the GDP figures are invariably revised, sometimes several years after the event. As the OBR pointed out in its last report, the latest figures show that the recession of 2008/9 was both deeper and shorter than originally estimated. Indeed, looking at this year, if you take VAT receipts, national insurance contributions and PAYE income tax receipts, you would think that the economy has been growing modestly rather than shrinking.

But the plain fact is that forecasts are usually wrong. Even the famous fan charts pioneered by the Bank of England and now adopted by the OBR can be wrong because they show only 90 per cent probabilities. So once every 10 years you would expect, by definition, the outcome to be outside the boundaries of the chart.

So why do we have them? The reason is that we all make implicit predictions in our daily lives and that some form of written forecast enables us to do so in an orderly way. For example, anyone taking out a mortgage to buy a house is making a series of mental forecasts. These include their future earnings and job security – can they afford to make the payments? – and also the likely profile of house prices. And these in turn depend on the expected path for inflation and for economic growth.

For companies, the forecasts have to be more explicit. A car company needs to know how many cars are likely to be bought in its different markets if it is to plan its production schedules, and that in turn depends on consumers' incomes and confidence. An airline has to make some stab at fuel costs, which in turn depends on the oil price. And so on.

So it is best to use economic forecasts as a discipline. They help to create a base on which you formulate your main plans, but also enable you to ask "what if?", so that if something at the edges of the possible happens, it does not come as a surprise. The central failure of the previous government was that it did not accept the possibility that the long boom would end. While it is true that hardly anyone foresaw the depth of the recession, quite a few of us did predict that there would be a downturn starting around 2008.

Armed with this caution about economic forecasting, what can we sensibly say about the coming year?

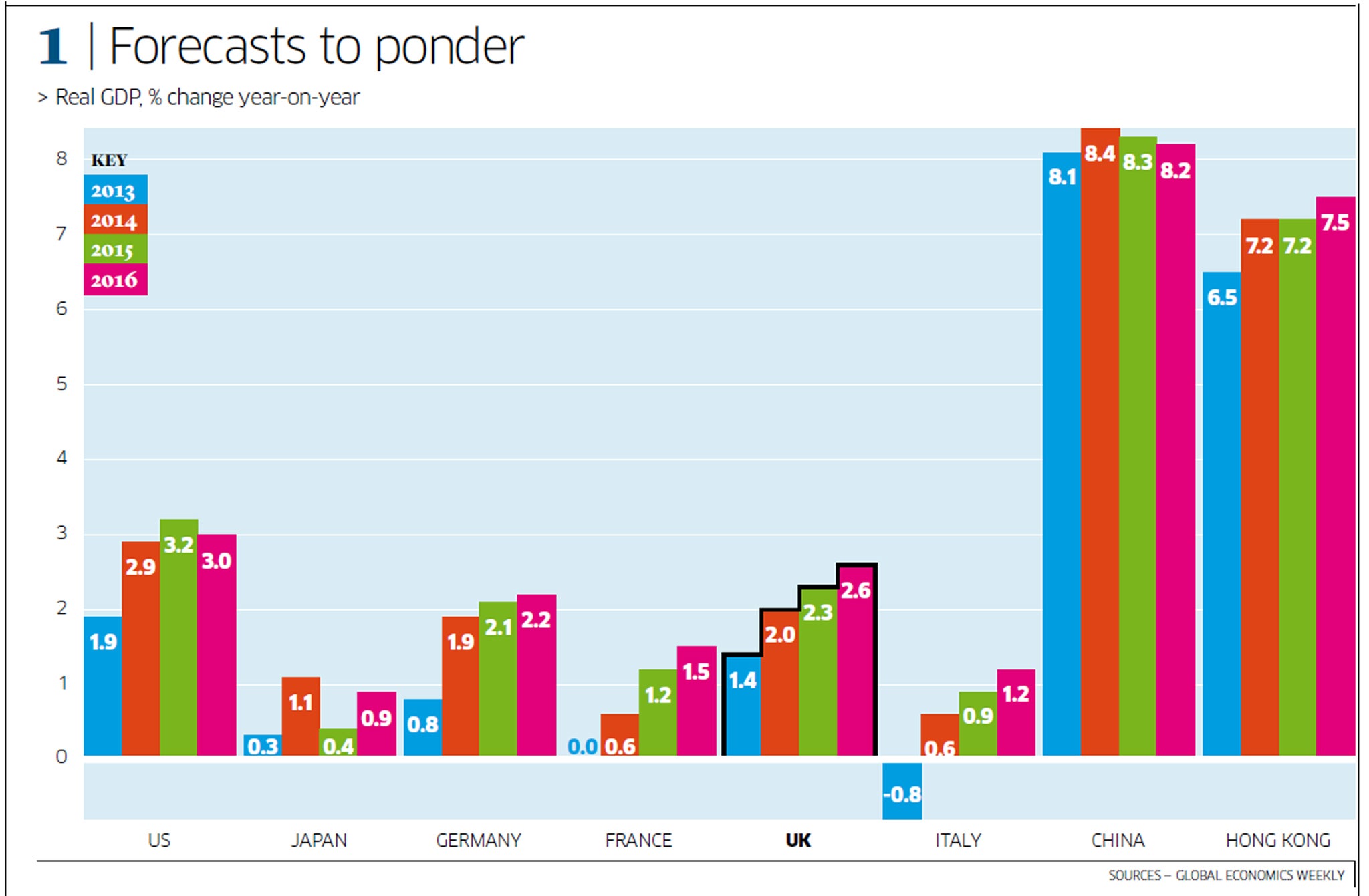

Well, I have shown in the graph some growth forecasts from Goldman Sachs for the major economies not just for 2013 but right through to 2016. Brave indeed – but remember we should see these as a discipline for thinking about the future rather than what will actually happen.

Start with the UK, which I have highlighted. Its view is that we will gradually pick up pace, so that from 2014 we will be growing at our past trend rate of a bit over 2 per cent. That itself leads into an interesting and massively important debate: what is the long-term sustainable growth rate of the British economy? Is it the 2.25-2.5 per cent rate that it has been for the past century or more, or have structural changes taken place that push it down to say 1.5 per cent?

The difference may not sound a lot, but it makes a huge difference over a decade. In a nutshell, if we can get back to growth averaging more than 2 per cent, then the debts run up during the past four years look bearable and living standards will be able to improve. But if the long-term rate of growth has been undermined, as some argue, then our children may have to accept lower living standards than their parents.

Meanwhile, we have to get growth going again, and so the basic question is whether this forecast's cautious optimism (which is broadly similar to that of the OBR) will be justified. Part of the answer will depend on what happens in other developed economies. Here, as you can see, the prospect is for decent growth in the US, somewhat slower in Germany, and slower still in France and Italy, with nothing much happening in Japan.

This picture of a slowly recovering developed world is in sharp contrast to the continuing boom in China and India. Here, the prospect is for steady growth of 8 per cent or more in China and a speed-up to more than 7 per cent growth in India. We have become so accustomed to these rates they have ceased to surprise us, but the contrast between those towers of growth on the right and the little stubs in the middle should be a reality check to us of just how rapidly the emerging world is overtaking the advanced one. Yes, of course absolute levels of wealth remain much lower than in the West, but every year which passes narrows the gap.

So I think the value of these forecasts is to make us focus on two huge issues. One is whether the recovery of the West is indeed secure. Are we really in the early stages of a sustained recovery, and will that recovery gradually strengthen over the next few years? I happen to expect that it will, but the "what if?" question needs to be asked. And the other is: when will this boom in China and Asia start to ease back, and how will China in particular make the transition to slower growth?

Analysts dust off their crystal balls, but consensus is lacking

It is that time of year when market – as opposed to economic – forecasters are also starting to set out their stalls. What will happen to share prices, bond yields, currencies, the oil price and so on. They have the advantage over economic forecasters that no one expects them to be right, but as with economic forecasts, it is a useful discipline. So, some observations.

One is that there seems to be a growing consensus that global bond yields are so artificially low that some rise over the next five years is as near an odds-on certainty as you ever get. The issues are whether this rise has already begun or, if not, will it begin this year or be delayed a bit?

It is quite hard to see any set of circumstances where yields could go much lower, because in the major markets they are already negative in real terms – the rate of interest is below that of inflation. But whenever there is broad agreement one should be especially cautious.

The second observation is that on equity pricing there are two contrasting views. One is that the present recovery is built on sand. If you look at the conventional valuation measure, price/earnings ratios, and adjust them for the fact that profits are cyclically high, they are quite stretched. So the scope for a reversal is huge. The other view is that while p/e ratios suggest share prices are not particularly cheap, the market will look through the present dip in global growth.

Besides, they do give some protection against inflation should that be the outcome of the flood of money that the world's central banks have printed. So, there is no consensus as far as equities are concerned, which is as it should be.

A third observation is that property is returning as a core asset in many portfolios. The point is simply that, with minimal yields on bonds and a hesitation at committing too heavily in equities, the obvious other category is something solid.

The particular twist here is a shift to residential property. Housing investment in traditional core markets, such as the US and UK, is now giving decent returns.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks