FCA was warned three years ago about mini-bond firm Blackmore Bond, which collapsed with £45m of savers’ money

Then-FCA boss Andrew Bailey was personally warned about the firm — yet no action was taken to shut it down

For three years, the City watchdog sat on information about an alleged “boiler room” operation in which savers were persuaded to transfer millions into risky investments now feared to be worthless.

Blackmore Bond PLC, which issued high-risk “mini-bonds” between 2016 and 2019 to raise money to develop properties, collapsed into administration last week. Investors, most of whom were ordinary savers, were promised stable returns of as much as 9.9 per cent but have not received a payment since October. They now fear that all of their cash has vanished.

Blackmore’s products were speculative investments in new house-building projects, which did not offer guaranteed returns and which left investors facing losses of up to 100 per cent.

Accounts show Blackmore collected £45m from investors, from which it paid out at least £9.3m in management and marketing fees. The company also took out a series of mortgages against its properties, most of which remain undeveloped.

Insolvency practitioners Duff & Phelps have been called in to try to recover assets for investors.

Blackmore’s collapse again raises serious concerns about gaps in regulation that allow risky investments to be marketed to unwitting investors with little protection from authorities.

Repeated warnings

White-collar crime expert, Paul Carlier, who has 30 years’ experience in the financial services industry, handed the Financial Conduct Authority (FCA) allegations as far back as March 2017. The allegations concerned salespeople from an agency called Amyma that was marketing Blackmore Bond. Other investors made complaints in March 2019 but the FCA failed to act.

In emails to the FCA, seen by The Independent, Mr Carlier alleged that Amyma was targeting pensioners and unsophisticated investors, using high-pressure sales tactics and making what he believed to be false and misleading statements about Blackmore Bond.

In August 2018, a year and a half after Mr Carlier first raised concerns, Amyma was still selling bonds claiming to offer “guaranteed” returns.

He escalated his allegations directly to Andrew Bailey, then head of the FCA and now governor of the Bank of England. Still the regulator took no action against Blackmore Bond or Amyma.

Blackmore Bond stated in its latest accounts that it continued to take in around £1.5m per month of investors’ money during 2018.

In December, the FCA finally stopped the marketing of mini-bonds – unregulated investments that are effectively IOUs issued by a company – to ordinary investors after the collapse of London Capital & Finance last March.

LCF is now at the centre of a Serious Fraud Office investigation into £237m of missing investors’ cash.

Blackmore’s former auditor Grant Thornton cut ties with Blackmore last March. A scheduled interest payment to investors in July 2019 was late and the company failed to file accounts in December.

Blackmore chief executive Patrick McCreesh said he had worked “tirelessly” to recoup money for the company’s investors.

Contact us

If you have any further information about Blackmore, its directors, or linked companies please contact us in confidence: ben.chapman@independent.co.uk

FCA asleep at the wheel

Some of Blackmore’s investors say they would not have invested their money if the Financial Conduct Authority had acted on multiple allegations it had received.

Back in March 2017, before investors had handed over around £45m to Blackmore, Paul Carlier, a former foreign exchange trader who now investigates financial wrongdoing, wrote to the FCA’s whistleblowing team to allege that he believed there were major problems with how Blackmore’s bonds were being sold.

Mr Carlier’s team of six experts in investigating white-collar crime were renting a co-working space in the City of London when they witnessed staff in a neighbouring office working for a sales company called Amyma “clearly targeting” pensioners with calls about Blackmore’s bonds.

Through the glass partition of a WeWork space in Moorgate, Mr Carlier says he saw and heard Amyma’s salespeople falsely claiming that 9.9 per cent annual returns on Blackmore’s bonds were “guaranteed” and that investors’ capital was “protected”.

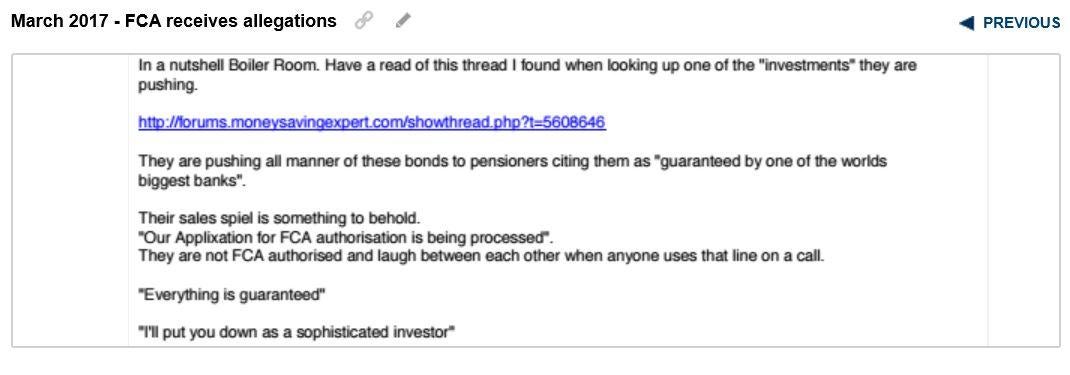

Believing the claims to be bogus, Mr Carlier wrote to the FCA’s whistleblowing team about Amyma, saying: “They are pushing all manner of these bonds to pensioners citing them as ‘guaranteed by one of the world’s biggest banks’.

“Their sales spiel is something to behold.”

Amyma’s salespeople would tell clients that their FCA authorisation was “being processed”, Mr Carlier said.

“They are not FCA authorised and laugh between each other when anyone uses that line on a call,” he wrote in an email to the FCA.

Mr Carlier, who has worked for several of the world’s leading banks, told the FCA that pensioners were “clearly being targeted” and said Amyma’s salespeople would high-five each other when they convinced someone to hand over their money for Blackmore’s bonds, among other investments they were selling, several of which have also turned sour.

A week later he wrote again to the FCA: “FYI these guys are still pushing this Blackmore Group bond product.

“Just overheard the pitch again: 9.9 per cent yield; interest paid quarterly; £75,000 maximum investment; all guaranteed.”

A spokesperson for the FCA said the watchdog was not responsible for Blackmore, as its activities were outside its remit. “Neither Blackmore Bond PLC nor the mini-bonds they sold are regulated by the FCA,” the spokesperson said.

However, the FCA is responsible for regulating the marketing of financial products to the public. It must ensure that claims made about investments meet certain standards including that they are “clear, fair and not misleading”.

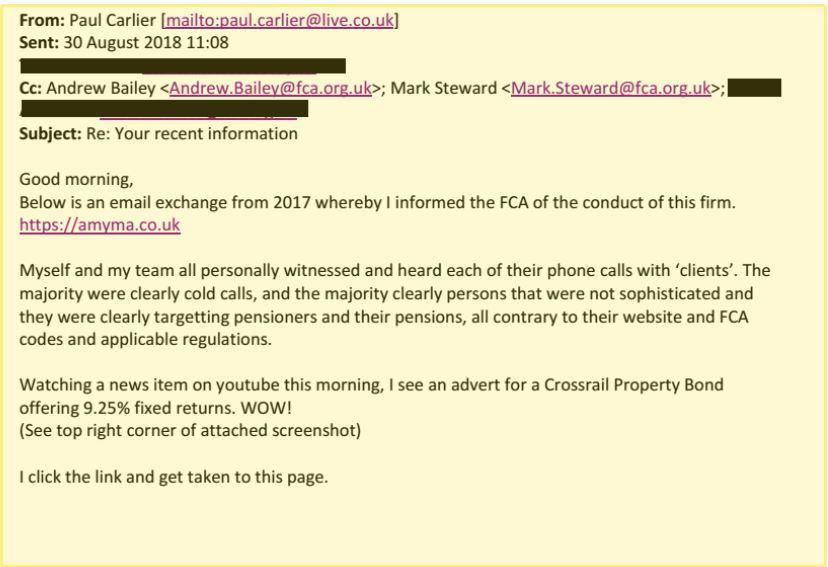

When Mr Carlier discovered – 18 months after he first raised concerns – that Amyma was still selling high-risk investments, he escalated the issue directly to FCA chief executive Andrew Bailey and head of enforcement Mark Steward.

Mr Carlier told Mr Bailey in August 2018: “Myself and my team all personally witnessed and heard each of [Amyma’s] phone calls with ‘clients’.

“The majority were clearly cold calls, and the majority clearly persons that were not sophisticated and they were clearly targeting pensioners and their pensions, all contrary to their website and FCA codes and applicable regulations.”

Three weeks later, in September 2018, Mr Steward responded, stating that the FCA was “making enquiries”. Just two months earlier, Amyma had been approved by the FCA as an "appointed representative" meaning it could carry out regulated activities.

What is a mini-bond?

There is no official definition. The name is controversial as it can mean people associate it with fixed-rate savings bonds of the kind offered by banks. Mini-bonds are very different. Returns are not fixed; they depend on the health of the company issuing them and the scrupulousness of the company’s directors.

Mini-bonds should also not be confused with corporate bonds, which are debt instruments issued by large companies on the financial markets. Firms issuing bonds through financial markets have a credit rating that is publicly available and independently established based on the company’s financial health. Once you have bought those bonds, they can be easily sold on to other investors.

By contrast, any company can sell a “mini-bond”. In legal terminology, a mini-bond is often in fact a “loan note”, a simple IOU from the company to the investor. The purchaser is lending money to the company with the hope that that company will pay it back with interest.

If the company goes bust, banks and other secured lenders will get their money back first from whatever can be recovered (often very little), leaving mini-bond holders at the back of the queue with every other unsecured creditors.

Investors in the dark

The Independent has heard from a number of investors who say they were contacted by Amyma and who describe similar sales tactics to those described by Mr Carlier.

Correspondence shared by investors supports the assertion that investors were told their capital was “protected”.

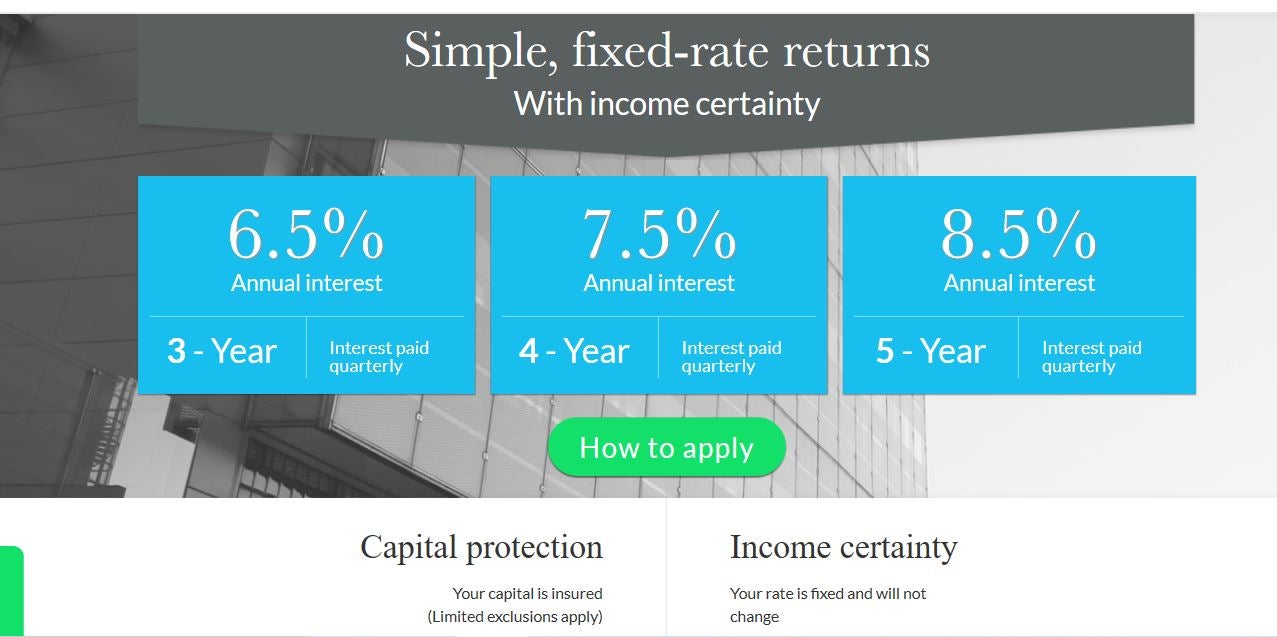

Brochures issued by Blackmore and archived versions of its website from 2017 and 2018 show that the company claimed to offer “simple, fixed-rate returns with income certainty”. The fact that capital was at risk was also stated less prominently within the documents.

Investors were told that their money was secured against the value of the properties but Companies House records show mortgages had been taken out on the properties. It is therefore unclear how much equity, if any, would be left for investors when the properties are sold and the mortgages paid off.

Blackmore’s 2017 accounts – the only ones it has publicly filed – also show that the company paid 20 per cent commission to sales agents who signed up investors.

A further 5 per cent of investors’ money was paid in fees to a parent company controlled by Mr Nunn and Mr McCreesh for services rendered.

The commissions meant Blackmore’s developments had to generate at least a 25 per cent return before any profits would be available to pay investors.

In total, at least £9.3m was paid out in marketing and management fees. It is unclear how much money was invested in the properties themselves.

Blackmore chief executive Mr McCreesh repeatedly refused to answer questions about how much mortgage debt the company had secured against the properties or how much investors might recover.

“I am the first to hold up our hands and apologise for the business decisions that we made that did not result in success,” he said.

“We made every effort to succeed, and even personally guaranteed each project showing how much we believed in and worked for the success of the company.”

A ‘massive cop-out’

According to the FCA’s register, Amyma did not have permission from the regulator to market any financial products to the public in 2017.

Despite the allegations the FCA had received, and at least three reports about Amyma in May 2017 to the police fraud prevention line, Action Fraud, the FCA granted the company permission to carry out regulated financial activity in August 2018.

The regulator confirmed to The Independent that it did not carry out checks on Amyma, its staff or directors because the company only applied to become what is known as an “appointed representative”.

Appointed representatives do not have to be directly approved by the FCA. Instead, they only have to find an approved firm that will vouch for their conduct.

The appointed representative can then carry out all of the same activities as the approved firm, despite never having been vetted by the FCA. Crucially, they are also listed on the FCA register, potentially giving the misleading impression to consumers that they have been accredited and are safe to deal with.

Mr Carlier described the FCA’s response as a “massive cop-out”.

“My concerns should have been on the record so that when [Amyma] went for authorisation it was flagged… someone is culpable. Are the FCA saying that they turned a blind eye?”

Amyma since appears to have ceased trading. Calls from investors have gone unanswered and the company’s sole remaining director could not be contacted for comment. A former Amyma employee told The Independent that the company followed all compliance procedures and did not cold call clients.

All investors that Amyma signed up self-certified themselves as “sophisticated”, the person said. This meant they agreed that they understood the risks of complex investments. It also means they were afforded little protection from regulators. He said Amyma only sold Blackmore’s products for “a few months” in 2017. Sales and marketing were then taken over by Surge Financial, which also sold London Capital & Finance’s bonds.

London Capital & Finance

The situation raises further questions about gaping holes in financial regulation that mean consumers may believe they are protected when they are not.

They also add to a growing list of problems that occurred under the watch of Bank of England governor Andrew Bailey, who was chief executive of the FCA from 2016 until March 2020.

Mr Bailey has faced criticism for the FCA’s failure to prevent thousands of savers losing £237m in the scandal surrounding London Capital & Finance, another issuer of so-called mini-bonds.

LCF bonds were marketed by Surge, an agency owned by former Kent police officer Paul Careless. After allegations of fraud against LCF, the company was banned from taking on new investors in early 2019.

What is the financial regulator’s responsibility?

The Financial Conduct Authority is charged with protecting ordinary savers and investors but UK and EU rules are a mess, leaving large gaps that aren’t regulated.

Some activity is within what the FCA calls its “regulatory perimeter” but much is not. For example, a “mini-bond” is not regulated, however marketing financial products to consumers is regulated.

Rules for investments are the FCA’s responsibility but rules for who can offer an ISA are HMRC’s responsibility.

The problem is that it is almost impossible for an ordinary consumer to understand all of the overlapping rules and regulations, so it is often hard to know if you are protected. Companies that are not regulated have for years taken advantage of this to avoid scrutiny or consequences for their actions.

Surge had been selling Blackmore’s bonds since 2017. It continued to sell Blackmore’s bonds after LCF’s collapse, contacting a number of LCF’s former clients.

One investor who put a six-figure sum into both LCF and Blackmore told The Independent that they believed parts of Blackmore’s marketing were a “pack of lies”, including the claim that his capital was safe.

They said they were initially attracted to LCF by the fact that it was approved and accredited by the FCA. They said they were then targeted by the same salespeople who pushed Blackmore Bond.

They were also encouraged by the fact that Blackmore’s chair, Kenneth ‘Buzz’ West, was accredited by the FCA and listed on the watchdog’s register as an approved person. Mr West left Blackmore in mid-2019 and there is no suggestion of wrongdoing on his part.

Blackmore’s brochure also claimed that the company had a “strategic partnership” with French bank BNP Paribas. The bank told The Independent that its property consultancy arm had undertaken work under a contract for Blackmore but the claim of a strategic partnership was untrue.

Responding to allegations that Blackmore’s marketing material may have been misleading, Mr McCreesh said: “Blackmore’s material was signed off by independent lawyers and regulated compliance firms, with full independent verification of each statement made and approved.

“The FCA also regularly commented and suggested changes to marketing material if they felt appropriate.”

The investor said they felt let down by the regulator: “I expected a high level of oversight [from the FCA] when in fact I now know there was minimal or none.

“I realised there was a risk there but you believe what you’re told, what you’re sold and what you read. You have a degree of trust in that.”

He added: “The letter that came with the bonds said ‘your full amount is protected’.”

Mr Carlier said the claim of a “guarantee” was also what had alerted him and his team to potential mis-selling by Amyma of Blackmore Bond. “They were saying that not only were returns guaranteed but the principal was ‘guaranteed by one of the world’s biggest banks’, which is simply not true.

“If you had a 9.9 per cent guaranteed return and the principal was also guaranteed, that would only be offered to the uber-wealthy. No ordinary investor would get a look-in.

“They were also going after people’s pensions, advising people to draw down their pensions, and they were marketing, which has to be regulated.”

The FCA said it took action that meant Amyma’s website was taken down and, in September 2019, Amyma’s status as an appointed representative was removed. By this time it was too late for many investors.

Blackmore continued to sign up £1.5m of investment per month during 2018, according to its accounts. Investors say that Blackmore and its sales agents were still making claims about guaranteed returns and “capital protected” in autumn of that year and into early 2019.

A spokesperson for Surge said: “Surge Financial is a third-party supplier of outsourced marketing services used in relation to raising investment for many businesses. It has never handled client money at any point.

“Blackmore had an FCA regulated partner – Northern Provident – and it signed off all marketing materials and financial promotions prior to publication, as required by The Financial Services and Markets Act section 21."

Investors’ concerns about Blackmore were heightened by the fact that its two directors, Patrick McCreesh and Phillip Nunn, were also directors of other investment schemes in which pensioners’ money is now allegedly unaccounted for.

They are directors of Gibraltar-based Aspinal Chase, which advised customers to switch their pensions into another unregulated fund called Blackmore Global, without informing them that they were also directors of that fund.

A separate investigation by the Insolvency Service found that another venture by the pair, Nunn McCreesh LLP, had received almost £900,000 in commissions between March 2012 and May 2014 for generating leads for Capita Oak, a pension fund which has seen investors lose £120m and is being investigated by the Serious Fraud Office.

Mr McCreesh said it was “completely incorrect” to state that Blackmore or Aspinal Chase had ever advised on pension transfers. “The shareholders in the Company are institutions, and they have their own individual clients who were advised by independent advisors unrelated to ourselves.”

He added: "We advised no clients and were simply a lead provider, and there has never been a suggestion of wrongdoing or any connection to the Capita Oak scheme.”

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments