Spread-betting firms lose £1.3bn in minutes after watchdog crackdown

The Financial Conduct Authority plans to impose stricter rules on financial spread betting products

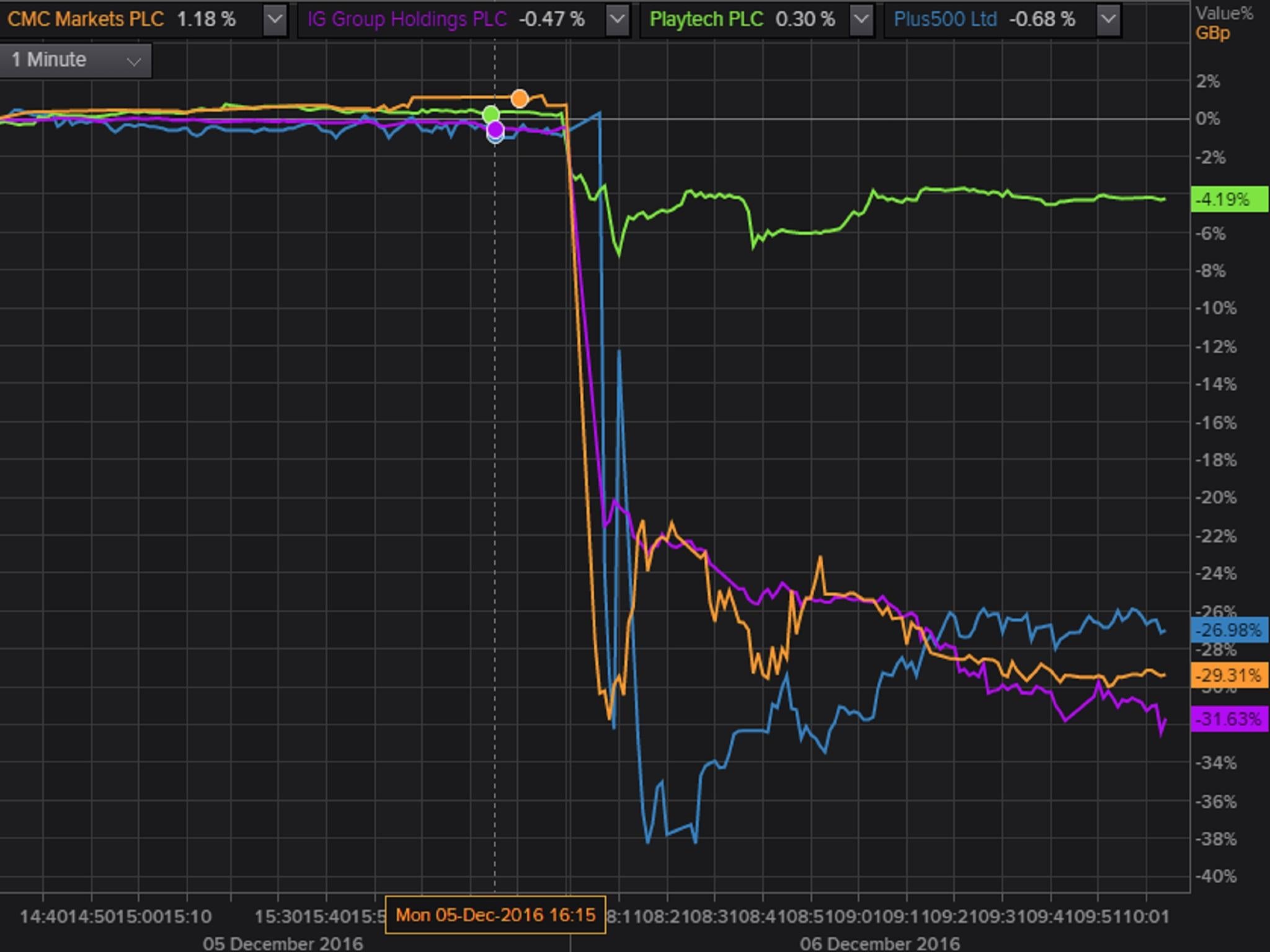

More than £1bn has been wiped off from the value of spread-betting firms after the financial regulator launched a crackdown on the spread-betting market to protect inexperienced retail customers from “unexpected losses”.

The Financial Conduct Authority (FCA) on Tuesday proposed tougher rules to help protect investors in the “contract for difference” (CFD) market, which includes financial spread betting, after finding that 82 per cent of customers using them lost money.

London-listed spread betters plunged by as much as 30 per cent following the announcememt.

CMC Markets, one of the biggest fallers among the larger providers, shares tanked by 29 per cent shedding about £156m of its market value.

IG Group, which holds 40 per cent of the UK financial betting market by number of active primary accounts, dropped by 29.6 per cent or the equivalent of £800m.

Playtech dropped by 6.4 per cent, losing the equivalent of £170m

Meanwhile the AIM-listed Plus500 lost about a third of its value or around £158m.

Plus500 has warned it will be significantly affected by the FCA's new rules for the spread betting industry.

In a statement to the stock exchange, the company said: “The company believes that the topics covered in the [FCA’s] note will have a material operational and financial impact on the UK regulated subsidiary which represents approximately 20 per cent of the group's revenues.”

IG Group said that it recognised there were “shortcomings in the approach to the marketing of CFDs” by certain firms, often operating from outside the UK.

“Certain of the FCA proposals could enhance client outcomes,” it added. “However, the FCA's proposals do not appear to directly apply to firms operating from outside the UK offering CFDs and binaries to clients in the UK on a cross-border services passport from another EU member state.

“IG will carefully consider the implications of the FCA consultation paper.”

Christopher Woolard, the FCA’s executive director of strategy and competition, said: “We have serious concerns that an increasing number of retail clients are trading in CFD products without an adequate understanding of the risks involved, and as a result can incur rapid, large and unexpected losses.

“We are introducing stricter rules for CFD products to ensure the sector addresses the shortcomings identified, and that firms make sure that retail clients are aware of the high risks involved in trading these complex products.”

Jake Green, regulation partner at the law firm Ashurst, said the clampdown by the FCA will come as “a shock” to the UK industry.

He told The Daily Telegraph: “This is less an example of ‘conduct regulation’ than ‘product intervention’, and this will come as a shock to the UK industry, which received detailed briefings from the FCA earlier in this year where this was not indicated.”

“The industry may consider that the FCA’s position misunderstands the users/clients who utilise these services. Many do understand the risk (and are aware that many lose) – they do not compare the product to less riskier ones (tracker funds as an example) and moves to reduce the risk appears to miss the point of the product.”

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments