90% of Google adverts for ISAs and bonds may be scams, search giant told

Sites back online within hours of being taken down, as campaigners demand action from government and regulators

Up to 90 per cent of adverts on Google for investment ISAs and bonds could be scams, the search giant has been warned – as it emerged that questionable sites have been taken down only to reappear again within hours.

As savers prepare to put billions of pounds into ISAs before the end of the tax year in April, scammers are taking advantage of Google’s lax controls to promote investments claiming to offer annual returns of up to 29 per cent.

Many promotions appear to break rules stating that only regulated financial firms can promote investments – an offence liable to up to two years in prison.

Mark Taber, a campaigner who has been warning of an epidemic of scam financial advertising online, has highlighted 126 separate promotions to the Financial Conduct Authority (FCA) and Google in just six weeks.

While most of these are eventually taken down, several appear to have immediately set up the same site again with only a minor change in the URL.

The FCA, which is responsible for protecting consumers, has a “scam list” but only a handful of the sites that have been flagged as suspicious appear on it, often several weeks after concerns have been raised.

Investment scams are estimated to have cost consumers £1bn last year alone, with many people being targeted after clicking on a Google advert and filling in an online form.

Google does not vet adverts before they go live, leaving consumers exposed to the risk that they may be targeted by unscrupulous firms that fleece them of their savings.

The FCA also predicted this week that savers will lose a staggering £20bn from bad pension advice – much of it procured through online searches – unless rules are tightened urgently.

“Pension scams continue to be both a cause of significant consumer harm to victims and a threat to wider consumer confidence and market integrity,” the watchdog said.

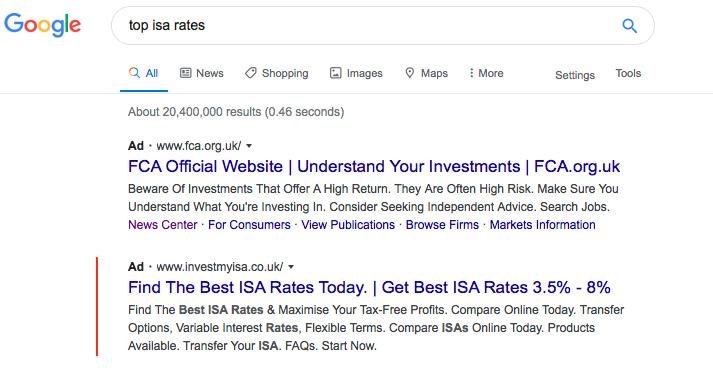

Most people seeking the best way to invest their savings will turn to Google. The top four results for any search for investments will almost invariably be adverts, subtly labelled as such with an “Ad” tag but otherwise indistinguishable from free results.

The ads are not at the top of the pile because they are the most relevant to the query, but because an advertiser has paid to appear after searches for a particular keyword.

Mr Taber, who has spearheaded a number of high-profile campaigns against banks on behalf of consumers, had a simple word of advice: “Don’t look for investments on Google.”

He has studied the adverts that Google displays when users search for common investment queries. He estimates that 90 per cent of those adverts take users to websites that are linked to investment scams.

A number of sites that have been removed by Google then appear to have been copied and pasted across to new domains so they can start advertising again almost immediately. Some have no contact details other than an online form, in breach of Google’s rules requiring advertisers to provide a physical address.

Other advertisers falsely claim to offer investments protected by the Financial Services Compensation Scheme which can return money to consumers in some circumstances.

Mr Taber is calling on Google to vet any adverts for financial products before they go online, a move he says would put a stop to most ISA and bond scams “overnight”. Under the proposal, if a firm is not authorised by the FCA it would be blocked by Google from advertising a financial product online.

“The FCA also needs to start prosecuting people who break the rules. It has the power to put people who issue financial promotions without authorisation in prison for two years but it never uses it.”

The FCA has started just two prosecutions for breaking financial promotion rules in the last two years and has not closed either of them.

Mr Taber said in the case of scam adverts the offence should often be as easy to prosecute as issuing a speeding ticket. If a company is advertising without being authorised to do so, it would receive a court summons in the post within days.

“It’s unrealistic for the FCA to expect Google to act if Google looks at the FCA and sees it’s not doing anything,” Taber said.

The FCA’s chief executive Andrew Bailey has said that the watchdog can’t prosecute Google because it is, according to Treasury guidance, exempt from financial promotion laws.

While a publisher such as a newspaper could be held jointly liable for publishing misleading ads, Google says it is not responsible for the content of adverts. Google brought in $113bn from advertising last year.

A Google spokesperson said: “UK consumers often look online for help with financial decisions but there are businesses who purposely set out to mislead consumers.

“Protecting consumers and the credible businesses operating in this area is a priority for us, which merits careful rules and enforcement.

“We are also working with the FCA and other independent experts on a scalable and long-term solution for us to ensure that consumers are protected.”

A government spokesperson said: “We want to protect people from misleading investment schemes and have given the FCA strong powers to ensure these products are regulated effectively.

“While advertising restrictions in the UK are among the toughest in the world, we are not complacent. We continue to review how online advertising is regulated in the UK to assess its economic and social impact.”

How do online investment scam adverts work?

Anyone can open an account with Google and start bidding to get their ad placed at the top of pretty much any search result. There are almost no checks beyond whether or not you can pay.

Many of these ads for investment products are legitimate, but Google is set up in a way that can favour less legitimate operators and even outright scams.

The search giant ensures it gets the most ad revenue it can through an auction for each keyword. Investment search terms such as 'best ISA bond' are among the most lucrative because each customer can generate a lot of money for an advertiser.

However, with no pre-vetting of ads, scammers are often able to outbid legitimate businesses.

A real investment firm has all the costs associated with actually running a business and investing the money; a scammer has no costs other than how much they have to pay to find customers and convince them to part with their cash.

The prize is also much larger as the scammer may take all of the money that someone “invests” with them, as opposed to a small commission that a legitimate firm would charge.

Mr Taber has created a database of adverts for ISA investments since the start of the year. He estimates that up to 90 per cent of those appearing at the top of searches are not legitimate investment companies.

Google says that it is not liable for scam adverts because it is a platform, not a publisher. The FCA says it cannot prosecute Google because it is based in Ireland and is – according to the Treasury – exempt from rules governing financial promotions.

So consumers have few places to turn.

Further problems

The primary aim of most investment sites advertising sky-high interest rates on Google is not to sell a product straight away but to induce people to input their details.

Then a salesperson will call to discuss what may be a legitimate - but high-risk - investment, or even potentially a scam.

Amazingly, these firms, known as “introducing agents”, do not have to be regulated by the FCA and nor do the products they sell, meaning consumers have very little protection.

The watchdog says it is only responsible for regulating particular types of firms. This includes any firm that promotes financial products but companies can get around this by saying that they are merely introducing an opportunity, rather than giving advice or arranging an investment.

However, many people who have been on the other end of a sales pitch from an introducing agent would be forgiven for thinking that they are hearing a promotion for a financial product.

‘Appointed representatives’

Another glaring hole in the regulations means that companies can trumpet their FCA credentials and be listed on the FCA register without ever being assessed by the regulator at all.

Any unregulated company can set itself up to promote investments as long as an FCA-regulated firm will vouch for it. The company will then appear on the FCA register as an “appointed representative” with no checks done by the FCA at all.

This has led to a cottage industry where a small number of regulated firms charge unregulated firms to piggyback on their FCA authorisation. This causes understandable confusion for consumers.

Very rarely are there any consequences for the regulated firm if the unregulated firm then breaks the rules.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments