Italy referendum explained: What is it about and what would a No vote mean for the UK?

If the eurozone economy goes into another slump brought on by a fresh financial panic it will damage growth in the UK by depressing exports and hitting domestic UK business investment

Italy will hold a referendum on Sunday on whether or not to change the country’s constitution.

The country’s centre-left Prime Minister, Matteo Renzi, has promised to resign if the electorate rejects his proposals. But the vote hangs in the balance.

Financial market traders are showing signs of nerves, with some analysts even suggesting that a "no" vote could ultimately lead to the destruction of the entire eurozone.

What is at stake? Why should the rest of us care? And what is the worst that could happen?

Below we answer the big questions.

What is this referendum about?

Matteo Renzi, who came to power two years ago aged just 39, wants to streamline Italy’s political system so he can push through a major economic reform package. He wants to reduce the number of senators and limit the senate’s power relative to the lower house of parliament.

He also wants to reduce the political power of Italy’s regions.

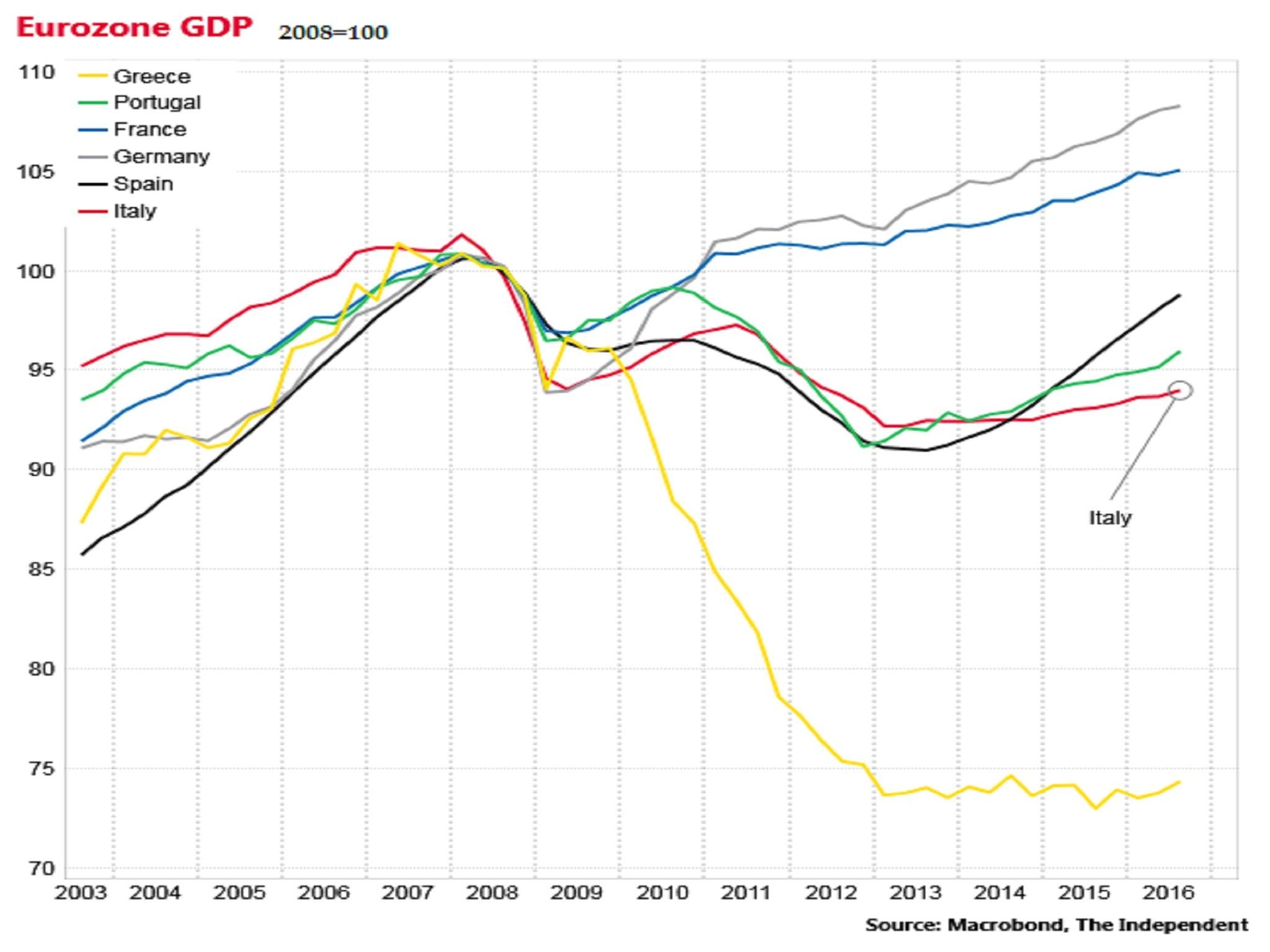

Few dispute that economic reforms are necessary: the Italian economy has essentially gone nowhere for 16 years and unemployment is high at 11.5 per cent. With the exception of Greece, Italy has had the worst performance of any eurozone country since the 2008 financial crisis.

Going nowhere

But any political reforms in Italy that have the effect of concentrating political power have, by law, to be put to a popular referendum.

This is a legacy of the country’s painful history of a fascist takeover by Mussolini in the wake of the First World War.

How is the referendum likely to go?

Before the official blackout on polls on 18 Novermber, there was a projected 53.5 per cent to 46.5 per cent lead for the “No” camp”.

There is some hope that the 20 per cent people who haven’t made up their mind will ultimately swing behind “Yes”.

But this has been a of year of massive protest votes – in the form of Brexit and Donald Trump’s US Presidential victory.

And the “No” vote is being championed by the populist Five Star movement, led by the comedian Beppe Grillo, an admirer of Mr Trump.

In short, the outlook for Mr Renzi is not particularly good.

So what happens if Mr Renzi resigns?

The government falls. But the real question is what happens after that.

It’s possible that the Italian president, Sergio Mattarella, could appoint another prime minister and a “technocratic” government could keep the show on the road for a while.

But if new elections are called for early 2017 it’s conceivable that the Five Star movement could come to power.

The party is currently on around 28 per cent in the polls, not far behind Mr Renzi’s Democratic party, which has a 32 per cent share.

An emphatic referendum victory might give Five Star the momentum it needs to get into pole position.

Sick man of Europe

Why is that dangerous?

The simple answer is that Five Star has said it would hold a referendum to decide whether Italy should leave the eurozone.

Italy is so large and economically important that many think the single currency itself would break up entirely if its people did vote to depart.

But there’s a way to go before we get to that point isn't there?

True. Under the Italian constitution, holding a referendum on the euro would itself require a referendum first. And polls suggest that around 67 per cent of Italians are in favour of remaining in the euro.

But the problem is that financial markets always try to get ahead of events.

They went into a selling frenzy in 2012 when it looked as if Italy and Spain would be unable to roll over their national debts and could, as a result, be forced to quit the single currency bloc in order to carry on paying salaries to public servants.

That panic could re-start if the referendum is lost on Sunday and traders assume the country is on a slippery slope to leaving the eurozone.

Why would the markets be so scared of that?

Because there would be colossal global economic and financial upheaval if the eurozone broke apart.

Investors who had lent in euros to a country would suddenly find themselves paid back in a new currency – a new Italian lira, or Spanish peseta, or French franc for example – and that currency may well be worth considerably less.

Domestic savers would face a similar devaluation risk to their wealth.

This threat creates a massive incentive for people, investors and companies to pull their money out of the more vulnerable eurozone countries and put it into stronger ones, like Germany.

This is what we saw in Greece in 2015, when capital controls had to be imposed to stop money haemorrhageing out of the country and destroying the economy.

The same kind of mass financial run could happen – but on a far larger scale, and across the eurozone – if the Italian domino looks about to fall.

So what should we expect from the markets if the referendum is lost?

The biggest short-term pressure point is the Italian banks, which are understood to be carrying around €350bn of bad loans and many of which are seen as undercapitalised.

Analysts warn of a renewed and heavy sell-off of their stock if the referendum is lost.

The other major indicator to watch out for is Italian government bond prices.

There could be major selling of these on Monday, driving up the Italian government’s effective borrowing costs, although this may be offset by an emergency buying spree from the European Central Bank in order to maintain financial stability.

Italian bond yields, which move in the opposite direction to prices, have already been rising since the summer and are now back above 2 per cent.

Pressure point

Why does this matter to Britain?

We may have voted to leave the EU on 23 June, but our economic and financial fortunes are still intimately tied to those of the Continent.

If the eurozone economy goes into another slump brought on by a fresh financial panic it will damage growth in the UK by depressing exports and domestic UK business investment.

This is precisely what we saw in previous outbreaks of the eurozone crisis.

Unemployment would rise and living standards would fall.

The pound may well gain against the euro – which would be good for holidaymakers heading to the Continent – but the overall economic impact of a return of the eurozone crisis for Britons would almost certainly be negative.

A new financial crisis may also make it harder for Britain to get the rest of the EU to focus on the Brexit divorce proceedings, which are due to begin next March.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments