How your junk mail can show if you're rich or poor

Are you 'pre-screened' for lots of mileage-reward cards? Banks think you’re rich and educated

If you want to know what credit card companies think of you, look at your mail.

Are you “pre-screened” for lots of mileage-reward cards? Banks think you’re rich and educated.

Do you mostly see offers for low-APR teaser rates? Banks think you’re poor and uneducated — and, perhaps, vulnerable to financial traps.

To get ahead in a highly competitive industry, credit card companies have become increasingly sophisticated — and specific — about soliciting new customers. They have also learned to be savvy about wringing profits from their cardholders, even if that means taking advantage of people’s behavioral weaknesses.

The game happens before our very eyes. Recently, MIT economists Hong Ru and Antoinette Schoar analyzed over a million credit card mailings collected by Mintel, a company that pays people to read their junk mail. The economists scanned the terms of these offers and noted the income and education levels of recipients.

Their preliminary findings, based on data from 1999 to 2011, span a seismic shift in the credit card industry. The Card Act of 2009 curtailed many industry practices that legislators deemed most abusive — in particular, the law caps late fees, curbs sudden interest-rate increases and makes it harder to penalize people if they go over their credit limit. So the practices that might have been widespread a decade ago would be much less today.

Still, companies target their cards to maximize profits off different kinds of customers, and Ru and Schoar's data offer a unique window into the heyday of that practice not long ago, when banks had perhaps the greatest freedom to take advantage of people's bad habits.

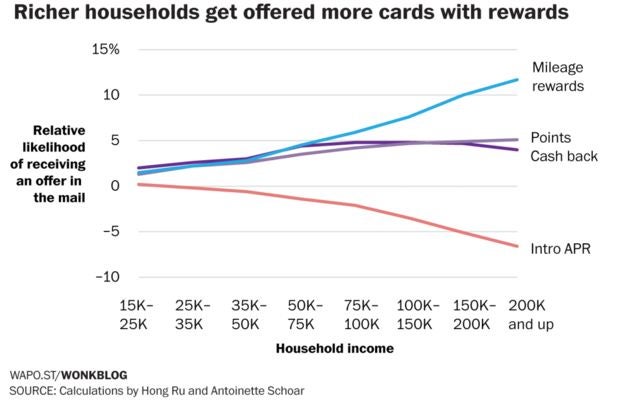

These were the broad patterns the economists discovered: Richer people were more likely to get cash-back, point-reward or mileage offers. Poor people were more likely to get offers that advertise a low introductory APR.

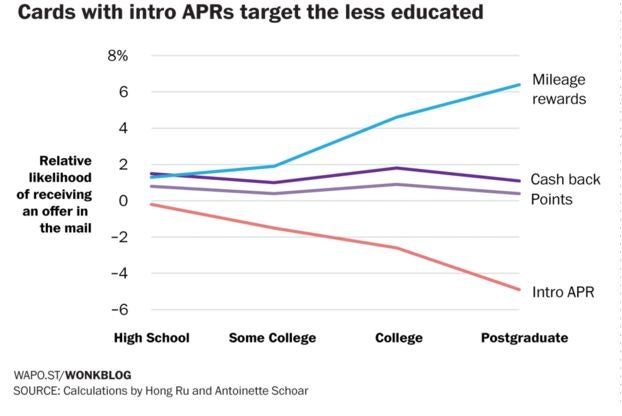

Mileage cards tended to be marketed at college graduates, while cards with teaser APR rates were sent to the less educated. Cash-back and point-reward cards were offered equally to people at every education level.

The innocent explanation for these trends is that banks offer people cards they are most likely to want (and qualify for). Different folks, after all, have different needs. But as Ru and Schoar dug deeper, they found that this wasn’t the whole story.

Cards with travel rewards epitomize the kind of product aimed at the rich and educated. It’s a fairly exclusive niche — only about 8 percent of credit card offers fall into this category. People in this demographic are the most likely to jet around, and therefore most likely to appreciate a card that will earn them frequent-flier miles.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

But frequent-flier credit cards carry other strange features. Even though they’re targeted at a rarefied clientele, mileage cards tended to have much higher interest rates, Ru and Schoar noticed in their data. They also had lower late fees and other gotcha features. The kinds of cards aimed at rich, educated people did not seem interested in making money off financial mistakes like the occasional late payment.

In contrast, the card offers sent to poorer, less-educated people were often loaded with risky features: low introductory APRs, high late fees, and penalty interest rates that kick in if you break the rules.

“Poorer people usually have worse credit, so standard economic theory predicts their regular APR should be higher,” says Schoar, a professor of finance at MIT’s Sloan School of Management. “And it’s not clear why the late fees, the hidden fees, the fees that hit you when you fall behind on your payments — why are they so high for the poor.”

In other words, if everyone behaved perfectly rationally, the market for credit cards wouldn’t look like this. But Ru and Schoar believe that the system was tuned precisely to take advantage of those who make financial mistakes. "Backward loaded credit card features with high late fees can only be optimal [for companies] if customers do not understand their actual cost of credit," they write, using a term to describe arrangements that offer low upfront fees but higher penalty fees.

Credit card companies earn their money in three main ways. They collect merchant fees every time you swipe a card. They also collect interest on your balance. Finally, they make money off the penalties they hit you with if you miss a payment or go over your credit limit.

To get more money out of people, companies could take advantage of consumers who don’t fully understand the system of penalties and interest rates. Banks could encourage borrowing by lowering the interest rate, at least temporarily. They would recoup their money, and then some, from the penalty fees after borrowers inevitably run afoul of the rules.

This strategy only works, though, with people who are sloppy with their finances. Savvier customers are careful to pay on time and never blow their credit limits. Because they are less likely to make financial mistakes, educated people are offered more straightforward deals from credit card companies. No teaser interest rates for this crowd, but also smaller late fees and other penalties because sophisticated customers are turned off by those shenanigans.

“It sounds almost Machiavellian,” Schoar says of the two different schemes, “but the thing to keep in mind is that it's not in the interest of a lender to kind of confuse the customers too much. If somebody becomes unable to repay, then they become a problem.”

Ru and Schoar had over a decade of data on credit card offers all over the country, so they were able to detect companies navigating a delicate balance between cards that encouraged people to spend and cards that encouraged people to spend themselves into ruin.

The economists noticed that in states that suddenly increased their unemployment insurance benefits, credit card offers were more likely to become riskier — to have zero introductory APRs and higher late fees. Ru and Schoar believe that this is because the extra government benefits reduced the chance that customers would dig themselves into a hole they couldn’t get out of. So companies were more comfortable pushing the envelope with enticing terms.

Schoar emphasizes that the credit card market is not completely segregated. If you’re well-educated, you’ll still sometimes get offers with introductory APR rates. She says this is something of a test. “Often, credit card companies will send different types of offers to the same customer type to see which kind of offer you will respond to,” she says.

Will you pay attention to the late fees and other penalties? Or will you be distracted by the teaser interest rates?

In 2009, Congress passed the Card Act to curb excessive late fees and overlimit penalties, among other terms that legislators thought were predatory. Ru and Schoar’s data mostly cover the years before the law’s provisions kicked in, so their research describes a world that was harsher for people prone to making financial mistakes.

"It’s a portrait of what was," says Nessa Feddis, senior vice president at the American Bankers Association, an industry group. The industry, she says, has changed vastly since 2010. "Late fees are lower, because they’re capped. The overlimit fees are virtually gone. And, also, interest rates are higher upfront."

According to the Consumer Financial Protection Bureau, credit cards are now more likely to make their money on “upfront pricing” — regular interest rates and annual fees — instead of “backend pricing” — penalties and late charges. But as companies try to make up lost revenue, some have turned to new alternative fees. According to the CFPB, some of these features still seem to prey on the unsophisticated. Bank of America, for instance, was fined last year for selling "financial protection" plans in misleading ways to its credit card customers.

Despite these new concerns, the credit card industry used to be much more unforgiving toward the financially naive. There's more leniency nowadays. Everyone is treated a bit more like a rich person, instead of like a poor person.

© Washington Post

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks