The Independent's journalism is supported by our readers. When you purchase through links on our site, we may earn commission.

What’s wrong with the economy? Well, just look at how we create money

It might worry you to learn that private firms can create money from nowhere, writes Jack Mosse. Yet the process is widely accepted by economists and commmentators alike, and alarmingly straight forward

Due to pure good luck, I found myself, in my late twenties, to be the owner of a flat in London. It was an unusually decorated large mezzanine studio, in a relatively deprived area. During that time (2013-17), I worked in a pub, as a football coach, and occasionally as an associate lecturer, while trying to complete my PhD. I owned that flat for four years. It was a nice flat, except for the quasi-criminal freeholder, who made a number of thinly veiled threats against my personhood. I was earning around £12,000 a year from the part-time work, along with occasionally renting the flat out through Airbnb, and my partner was supporting me by paying some rent. However, the flat increased in value by around £120,000 over those four years – £30,000 a year!

During that period the average wage in the UK was around £28,000. There is a serious problem with an economic system that pays the owner of a property to sit around in his pants (not what I was doing all the time) – considerably more than what most people get for devoting 42 hours a week/most of their waking life, to a job.

This problem is deeply connected to how money is created and allocated.

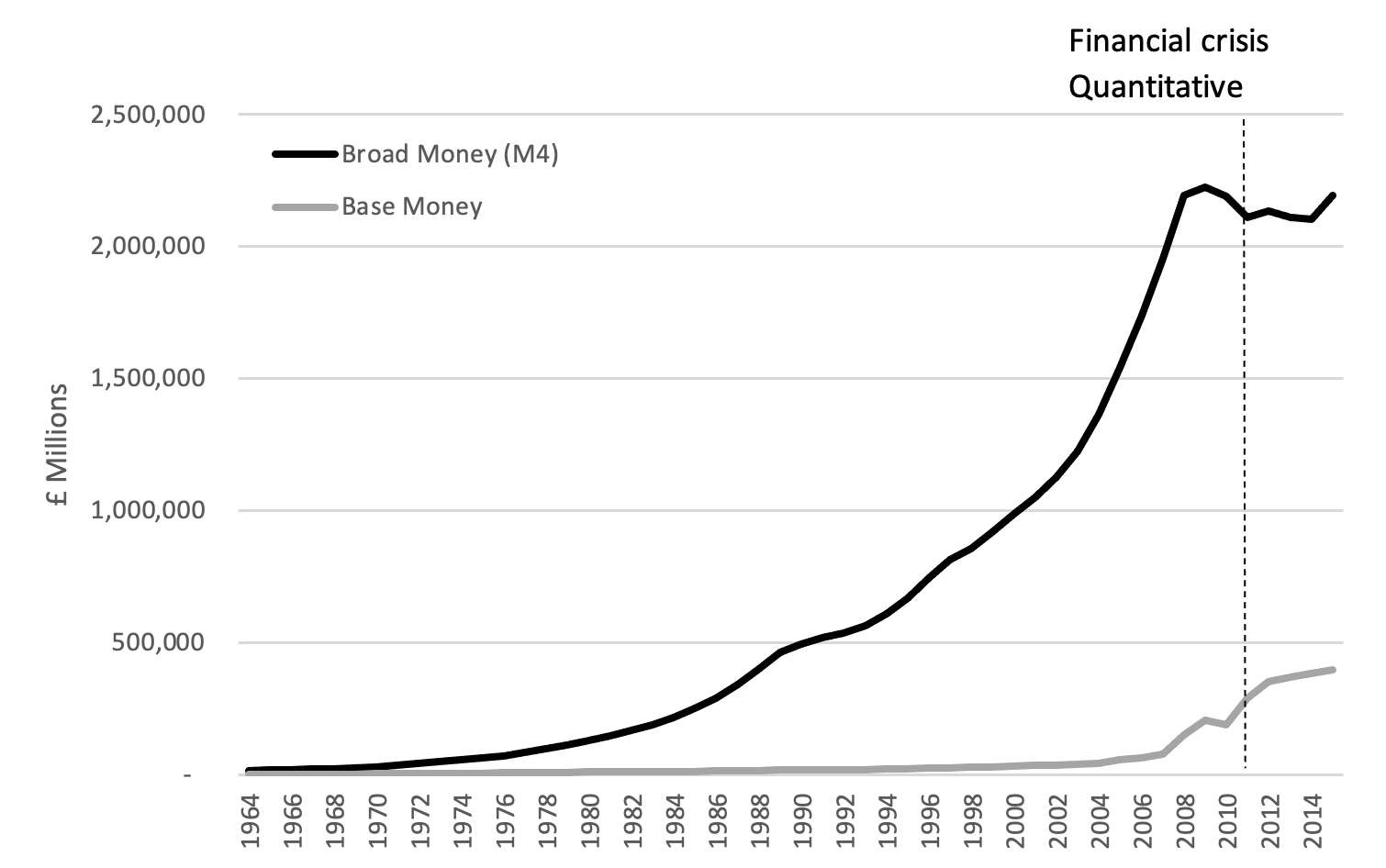

A recent poll of 100 MPs demonstrated that 71 per cent wrongly believed that: “Only the government – via the Bank of England or Royal Mint – has the authority to create money, including coins, notes and the electronic money in your bank account.” However, in fact less than 3 per cent of money in the UK has been created by the government. Figure 1 illustrates the exponential growth in money created by privately owned banks (M4) from the 1960s onwards and compares it to base money (money created by the government):

Figure 1

As Figure 1 shows, the money in our society is created mainly by private organisations. The result of this is that private organisations with the capacity to create money determine how wealth is allocated across society. There is strong evidence to indicate that when allocating money these institutions favour investments that are non-productive, and invest in existing assets that do not add to GDP. The recent unprecedented inflation in the housing market and the astronomical growth of trading on the foreign exchange market and in fixed assets and securities amongst banks are testament to this. In fact, only around 3 per cent of the money loaned out by the banking system in the UK is lent to firms engaged in the production of goods or services (ie to industries that employ people).

Readers who are new to the notion of credit creation may find it strange that private firms can create money from nowhere. Yet the process is accepted by mainstream economists and respected commentators, and is alarmingly straight forward.

A brief history of money

Different forms of private money creation have existed for millennia, but the version that characterises the contemporary scene in the UK is best understood by going back to the goldsmiths of the 17th century. The second half of the 17th century was a time of war and insecurity, so people wanted safe houses to store their precious metals (usually gold). Goldsmiths, who had secure spaces to store such valuables, began to earn money by acting as safety deposit holders. They had secure safes that were trusted storage spaces and charged people a small price for keeping their valuables in them.

When a customer deposited something in a goldsmith’s safe, the goldsmith would issue them with a receipt, which could be used to withdraw the deposit in the future. As this practice became widespread, depositors started to pay for things with deposit receipts, thus transferring ownership of the deposit to the seller. To facilitate this payment system, more and more unnamed deposit receipts were issued by goldsmiths, until eventually they became a generally accepted means of payment: paper money.

Private credit creation means that private institutions are able to determine which sectors of society receive money and which don’t

For goldsmiths, this presented a further business opportunity. They were amassing larger and larger quantities of gold, which were lying dormant in their safes, and they realised that they could lend out some of the gold and charge interest on it. The interest would be pure profit for the goldsmiths at almost no cost. To counter the risk of loaning out the gold, they had to ensure that they lent against collateral, which they would be able to collect if the loan wasn’t repaid. So, they started to loan out gold at small rates of interest against collateral.

Then another development occurred. Given that the receipts were an accepted means of payment, they realised that they could give borrowers deposit receipts instead of gold. They could print deposit receipts (even if they did not relate to any deposited gold) and loan them out, charging interest.

If all went well, the goldsmiths would collect their interest and be repaid in full, but if the debtor failed to pay, the goldsmiths could foreclose and collect the collateral. It was fraud (as there was often no gold backing up the receipts), but also a win-win situation for the goldsmiths. The economist Richard Werner (quoting his colleague Withers) writes of this process: “Banking was born: the same process describes the activity of present-day commercial banks: ‘some ingenious goldsmith conceived the epoch-making notion of giving notes not only to those who had deposited metal, but also to those who came to borrow it, and so founded modern banking’.”

The story doesn’t quite end there. In time, central banks were established, and the issuance of paper money (ie banknotes or deposit receipts) by private firms was outlawed. Only central banks (which were often connected to governments) were allowed to print paper money or mint coins, as policy makers sought to control the supply and allocation of money. However, while it remains the case that commercial banks cannot issue physical banknotes or coins, there is nothing to stop them typing numbers on computer screens and creating digital money. As such, digitisation, combined with deregulation in the mid and latter part of the 20th century, and the move away from the gold standard (Bretton woods) has led to an enormous resurgence in private bank money over the past five decades. To reiterate, currently about 97 per cent of the UK’s money supply is created by private banks.

You don’t need a Nobel Prize in economics, or even an economics degree, to recognise that the institutions that create and allocate the vast majority of money in a society (like the kings and queens of old), will have significant power over the shape of that society.

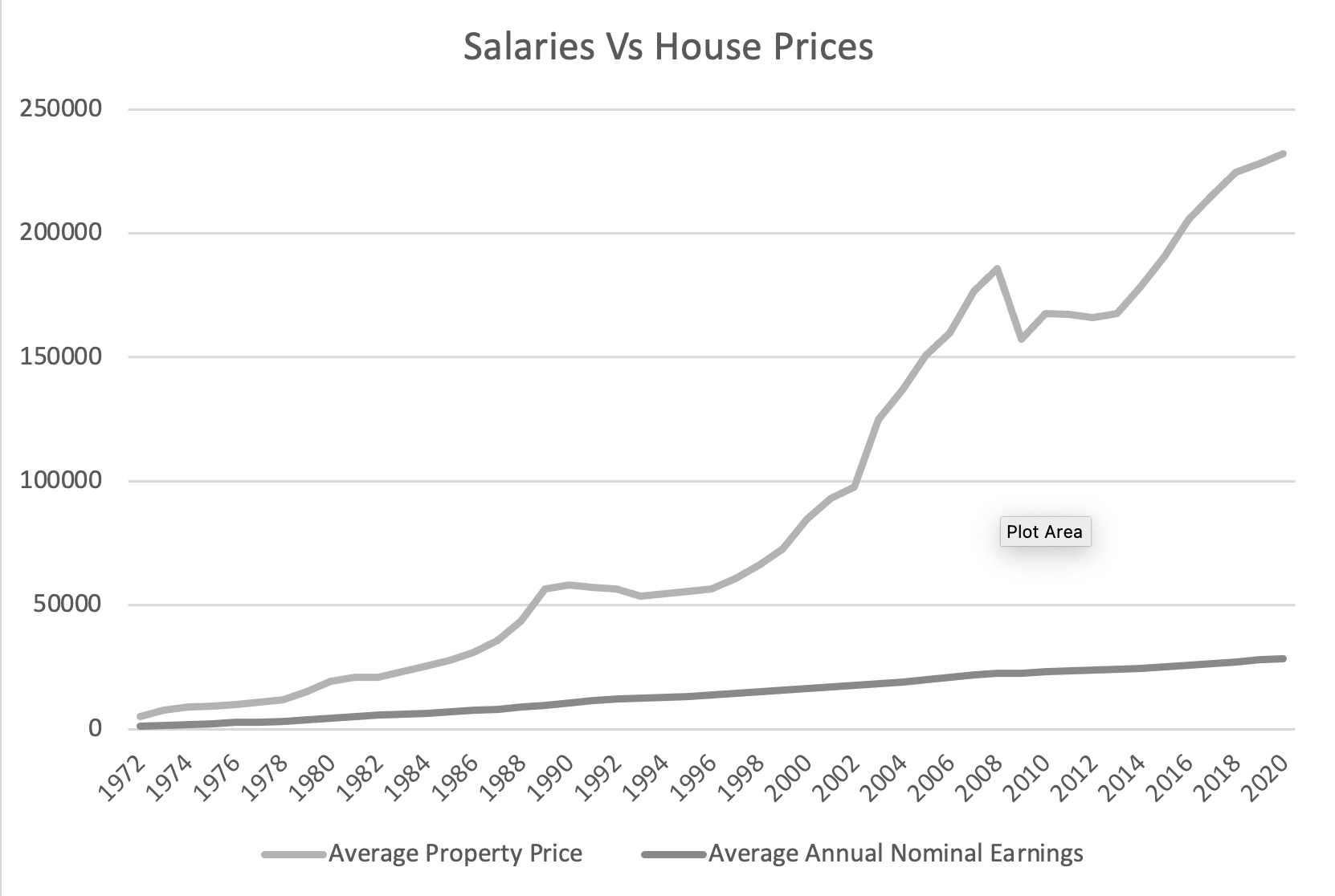

Private credit creation means that private institutions are able to determine which sectors of society receive money and which don’t. It will not have escaped the reader’s attention that over the past 40 years or so some things have become far more profitable than others. Working, for instance, has not been particularly profitable, whilst owning a property (as I found out) has been extremely profitable. This is the difference between what economists call income (the money you are paid for doing your job) and wealth (the value of the assets you own). Consider that in 1980 the average wage in the UK was £4,542, with the average house price at £19,273, while in 2021 the average wage is £31,461 and the average house price is £231,855. This shows that house prices have grown at almost twice the rate of wages: see the crazy disparity between wages and house prices in Figure 2.

Figure 2

The implications are that the people who own houses and/or other assets have become richer as the value of their assets has increased substantially, while those who don’t and have to work for a living get left behind.

This begs the question: why would private credit creators put money into static non-productive assets, rather than into firms and businesses that employ people to make or do things? Because, like the goldsmiths in the 17th century, credit creators want to lend against collateral: if you lend to a business that makes things or carries out services, then you are counting on repayment from a future income stream produced by product sales; but if it all goes wrong and they can’t repay, there won’t be much collateral for you to collect. However, if you lend on property (residential or commercial) or various kinds of bonds and the borrower can’t repay, you can take ownership of their property.

So, in a system in which private institutions driven by the profit motive create and allocate money as they see fit, there is a clear incentive to pump money into fixed assets that can be taken as collateral. If these assets are owned by an already wealthy minority, then the effect is to make them even richer, and to drive inequality by attracting investment away from the “real” productive economy of goods and services, from which the majority of the population draws income and relies on to survive. The asset distribution in our society means that at present, wealth inequality is about twice as great as income inequality on some measures, with around 10 per cent of the population owning 50 per cent of the wealth, and the average net wealth for the lowest 40 per cent being 0. This system is behind what Bret Christopher calls “rentier capitalism”, as it propels a situation in which the ownership of assets, rather than the creation of goods and services becomes the central determinant in the allocation of wealth and power across society. By driving up asset prices, it allows those who own them to capitalise on their increased worth, and to profit on the use of these assets by those who cannot afford to own them. As such, it is a key factor in the rising levels of inequality we have seen for the past 40 years or so.

Finally, there is no incentive for private firms to invest in social goods, like education, healthcare or green infrastructure. Investment in these areas often does not produce an income stream

Furthermore, as the scenario with the goldsmiths outlined above indicates, when bankers create money by lending they also create debt, as borrowers are expected to pay that money back. A system that depends on debt is one that is likely to be prone to boom-bust cycles (as there will be greedy periods of reckless lending and then fearful periods of paying some of that lending back). The most recent example was the crisis of 2008, when huge quantities of money that had been issued by banks created a global financial system that was entirely dependent on debt. When it became evident that some of that debt wasn’t going to be paid back and some of the assets used as collateral weren’t sufficient, trust was lost, the flows of credit and lending stopped and the system seized up. Money that had been flooding into institutions, industries and whole countries was suddenly withdrawn, creating social, political and economic chaos.

Linked to the boom-bust cycles intrinsic to an economy dependent on private debt, and the surge in investment in fixed assets, is a tendency towards speculation. As a result of the incentive to invest in static assets, the value of those assets increases, making them even more appealing. Profit-seeking credit creators then pump more money into these assets, thinking they will be able to sell them at a later date for a higher price. Speculation like this, along with the debt financing described above, leads to harmful instability, as when something else comes along and money is moved from one asset to another, the value of the initial asset begins to fall and there is then a rush to get money out of one area and into another.

Finally, there is no incentive for private firms to invest in social goods, like education, healthcare or green infrastructure. Investment in these areas often does not produce an income stream in return, so there is no reason a private firm, driven by the profit motive, would seek to invest in them. As such, an economy dominated by private credit creation underfunds these areas of social overhead expenditure, making healthcare and education more expensive for the average citizen. At the same time, fund investors and major corporates pump money into fossil fuel, high carbon industries, aggravating the climate emergency.

I have sketched, in the broadest of terms, some of the problems that arise in a system that is dependent on the creation of private money: it is a system that breeds inequality as it generates private affluence and public squalor while aggravating the environmental crisis. These structural problems stem from certain institutions enjoying the privilege of being able to create money out of thin air.

Controlling the money supply

There is some recognition of these problems among policy makers and the state does attempt to exert some control over the money-creation process. However, the three policies they traditionally use are ineffective at controlling private credit creation and allocation in any meaningful way. I will outline the issues here. Those who want greater detail should refer to more scholarly accounts.

1. The formal regulatory tool (eg the ability to set reserve requirement). Rather than gold, physical cash and central bank reserves, which are created by the central bank and issued to private banks, are now used as the reserve behind the private credit that banks create. The reserve requirement is the amount of reserves a bank needs in relation to the deposit accounts it has created for its customers. When customers physically take out cash from a commercial bank they take out notes that the bank has received from the central bank. In principle, a central bank (or government) can introduce a regulation that means that commercial banks must have a ratio of reserves in relation to the money they create in deposit accounts. In this way the central bank could control how much money is created by commercial banks, as the central bank is the only place reserves can be created. In reality, following deregulation in the early 1970s the Bank of England abolished the need for commercial banks to have a minimum level of reserves in relation to their total deposits. There have been some attempts to reintroduce a mandatory ratio following the 2008 crisis, but there is a fear that if ratio levels are increased there will be a liquidity crisis (i.e. the banks will not be able to provide customers with their deposits). Instead, the policy has been to create more reserves to match the already inflated credit.

2. The quantity tool (ability to manipulate the amount of reserves). Rather than setting reserve ratios for each bank, central banks can simply increase or decrease the amount of reserves in the system. In principle, this will have the knock-on effect of increasing or decreasing the amount of money commercial banks are willing to deposit in customers’ accounts. However, there are a number of reasons as to why this is ineffective. Firstly, issuance of reserves tends to follow rather than lead commercial bank created money. This is because if the central bank does not issue reserves when a commercial bank needs them to, the entire payment system may collapse, which would have detrimental effects on society at large. So, ultimately, the central bank will provide reserves if the commercial banking sector needs them to.

As Ryan-Collins et al state: “When a commercial bank requests additional central bank reserves or cash, the Bank of England is not in a position to refuse.” So, the “quantity tool” is ineffective in regards to its ability to restrict credit creation. Furthermore, if the central bank wishes to issue more reserves to increase bank credit creation and stimulate economic activity (as it may wish to do in times of recession), the result may well prove to be ineffective, as there is no guarantee that banks will spend their excess capacity if they do not trust the market. They might just sit on those new reserves or, as is happening with QE, they may elect to use their extra spending power to allocate money to non-productive assets, which do not contribute to the betterment of society but only push asset prices up. Thirdly, and the final major reason reserve ratios are ineffective in the current scenario, is rather than having to always settle up with each other in central bank reserves, commercial banks can net out with each other in the money they create.

What this means is that if bank A creates £100 and gives it to bankB, and then bank B creates £100 and gives it to bank A, both banks will be even and there will be no need to transfer central bank reserves. Money will have been created irrespective of central bank reserves, so if all the banks create money at the same time, total money will increase regardless of what the central bank does.

Increasing the reserve ratio or banning credit creation altogether would rein in the ability of private organisations to create money and add some stability to our economic system

3. Interest rates. In the UK and across other industrialised nations, starting in the early 1970s, there was a move away from trying to directly control the quantity of credit created by commercial banks and towards controlling the price of credit – ie towards controlling interest rates. Central banks thought that by controlling the price banks could borrow reserves at, they would be able to control the price at which banks lend to each other and to their customers, and thus have some control over the amount of money in the economy.

Higher interest rates would mean less people would want to borrow money and less money would be created; lower interest rates would mean that more people would want to borrow and more money would be created. However, Lee and Werner draw on empirical evidence from the US, the UK, Germany and Japan to show that rather than determining or controlling credit, interest rates follow credit growth or depletion. So again, the tail seems to be wagging the dog.

Further to this, as Pettifor has shown, the interest rate set by the Bank of England has very little effect on the interest rates set in the “real” economy because the Bank’s rate has been lowering over time while the real interest rate (the rates at which businesses and individuals borrow) has been rising over time. Furthermore, as is evidenced by the experience in the UK and in Japan over the past few decades, low interest rates do not mean that banks will lend (create) more money. As Werner has argued, banks lend (create), depending on whether or not they think they will be paid back or on the collateral behind the loan, rather than on the interest they hope to receive. As a central bank tool for controlling bank credit creation, setting the interest rate at which banks can borrow reserves has little effect.

Finally, even if central banks were successful in their attempt to control the supply of money through interest rates, they would still be unable to control how the money was allocated, and therefore would be unable to stem the allocation of money towards unproductive, speculative or environmentally damaging means and direct it towards productive purposes that benefit society.

So, private firms have a relatively free hand in creating our societies’ money and deciding where it goes. This is problematic, as the arguments above have demonstrated. However, reform is possible and there are things that can be done to change the situation. If we recognise this and start to do some of these things, whole new futures become visible.

For instance, one shock treatment method for regaining control over the money creation process would be to ban private credit creation altogether. Banks would therefore only be able to lend out the money their customers have deposited with them, which is how most people think banks work anyway. This would massively rein in their ability to pump money into unproductive assets.

However, placing a ban on credit creation in the institutions that create 97 per cent of our money is a draconian policy, and the effective withdrawal of established credit lines would have a huge immediate shock effect on all kinds of economic activity, which would dwarf any previous banking crisis. One different option, among others less radical, would be to increase the percentage of central bank reserves commercial banks are required to have in relation to the loans and deposits they make. Indeed, up until the late 1960s, UK banks had to hold 8 per cent of their assets in the form of cash and had to have a liquidity/reserve ratio of 28-32 per cent. This restrains credit creation as reserves can only be created by the central bank, thus allowing the policy makers a degree of control over the amount of money created. Some advocates of this approach think that banks should ultimately have 100 per cent reserves for all the money they lend out or deposit; this would give the central bank total control over how much money is in the system and effectively be a ban on private credit creation.

Increasing the reserve ratio or banning credit creation altogether would rein in the ability of private organisations to create money and add some stability to our economic system. But these solutions don’t deal with inequality or the climate crisis, as they don’t deal with the allocation of money – with “what goes where and who gets what”.

Yet there are many practical and historical examples of money being created and directed towards more productive and socially beneficial ends. For instance, in Germany regional saving banks known as Sparkassen have a mandate for public service and local development. As such, they are responsible to their local municipalities, and prioritise lending that benefits society. A large part of this is a focus on productive lending and they provide the finance for 70 per cent of Germany’s much envied SME (small to median enterprise) sector. Furthermore, because of their social mandate, which is decreed in Germany’s constitution, they are ‘significant contributors’ to the movement towards a green transition.

The same sort of system could easily be applied in the UK. Think of the benefits that would have occurred if the £500bn the state created as part of its QE programme after the 2008 financial crisis had been allocated towards green and other socially beneficial projects rather than handed over to the financial sector and then pumped into static assets. Furthermore, as we have witnessed throughout the Covid-19 pandemic, it is relatively straightforward for the state to create money and direct it to the places that need it.

Other high-profile examples of policy makers influencing the creation and allocation of money include: the UK up until the late 1960s, as banks were given ceilings on how much they could lend and also told where they should lend to; the Fed in the 1920s; the Japanese, Korean and Taiwanese systems from the 1940s onwards, and present-day China. Richard Werner’s highly regarded book on Japan shows how the Japanese post-war “miracle” growth was achieved through policy makers controlling and directing bank credit creation. As he puts it in a later work: “Essentially, the central bank told the private banks on a quarterly basis by how much they would increase their lending” and adds that the central bank also told the private banks which sectors of the economy to lend to.

I am writing as an outsider to the economics profession and drawing on the work of established economists and system critics like Werner. But, as the last few paragraphs show, there are historical examples and strong precedents which demonstrate practical ways in which we could shift the control of the production and allocation of credit away from private organisations and towards a more productive, socially constructive, greener way of doing things.

Modern monetary theory

Moving credit creation away from private firms means moving it towards the control of our democratically elected government, which raises further points of discussion.

Firstly, there is a widespread view that the state can’t just create money out of nowhere, as it is limited in how much it can spend by how much tax it collects and how much money it borrows. Secondly, there is a fear that if the state could just turn on the printing press, there would be rampant inflation, as they would succumb to the political pressure to create more and more money.

Yet the pandemic provides a good example of why government spending, as opposed to private credit creation, doesn’t need to be inflationary, and can be socially beneficial

However, an increasingly influential branch of economics known as modern monetary theory (MMT) argues that states who are in control of their own currency can create as much money as they want, and can do so without causing inflation as long as there is unused economic capacity and some unemployment of labour. This is because central banks or treasuries can always type more zeros onto their computer screens and then send those zeros to somewhere in the economy. MMT argues that this works because governments are currency issuers rather than currency users, and as long as the currency they issue has value in their society (which it is likely to as it is the currency that they collect tax in) they can determine the money supply and issue as much or little as they want. As such, according to MMT, once the important caveats about available resources have been established, there is no budget constraint: governments who are in control of their own currency do not have to only spend what they tax or borrow, they can, and do (QE), create money out of nowhere.

So, if this is true, and governments can create money out of nowhere, why don’t they create more of it to do things like buy medical equipment for our hospitals, build houses and pay nurses or teachers more? Inflation. More money being pumped into a system in which there is already full employment of resources, and therefore a limited quantity of goods and services, just produces general inflation and widespread higher prices: people will be paid more, but things will cost more, and nothing much will have changed. However, as things stand, private banks create and allocate almost all our money and this has led to inflation of some prices but not of others. As explained above, we have seen inflation in housing and other fixed assets, but little change in the wages people get paid or in the everyday things they spend their money on. This type of inflation, driven by private credit creators, clearly benefits wealthy asset holders at the cost of the rest of society.

Yet the pandemic provides a good example of why government spending, as opposed to private credit creation, doesn’t need to be inflationary, and can be socially beneficial. Consider that, since the beginning of the pandemic, the government has poured £450bn into the economy, but we have seen no significant inflation. This is because the money the government spent was targeted towards picking up the slack from private sector closure (ie providing income for workers and firms who were idle) in an economy which had masses of unused resources. As such, it shows that putting money into unused resources does not create inflation. And this implies that running the economy at less than full capacity (eg full employment) creates room for government spending that won’t be inflationary. A key aspect of this from an MMT perspective is that the government wouldn’t need to pay back any of the money because they didn’t borrow it from anywhere, but simply printed it from scratch.

MMT’s arguments do not only insist that the state can step in and spend money in areas where there are unused resources, they also highlight that through regaining control of the money supply the state gains the opportunity to move resources from one sector of the economy to another, as through tax and spending the government can move money around different sectors of the economy without causing inflation. For example, the state could engineer higher pay for care workers, teachers or nurses by creating money and directing it towards those sectors, and developing legislation that meant that it translated into higher wages. While at the same time, if they were worried about the inflationary impact such a policy would have, they could raise taxes on the incomes of those who work in less socially beneficial jobs, such as wholesale finance. This would result in a shift of resources, from those working in finance to those working in socially beneficial sectors. It would not lead to inflation or deflation as it would be a case of taking money away from one area and adding it to another. What MMT argues is that the government is much freer in its capacity to move money around the system like this than many people believe, as its spending will not be dependent upon how much it taxes or borrows. As such, it could both pay care workers more and invest in green infrastructure without raising taxes anywhere else, if it felt there was space in the economy to do so without causing undue inflation.

In total, the pandemic has seen the Bank of England (a publicly owned body) create and then pump £450bn into our economy; the Fed have spent close to $6 trillion. If state spending was entirely dependant on tax and borrowing it wouldn’t have been able to spend the way it has, the huge deficit and the enforced closure of large sections of the private sector would have emptied the coffers and led to utter havoc – rationing, mass unemployment, pitchforks at the door type scenarios. But that hasn’t’ happened, at the time of writing, the unemployment rate is no worse than it was at the start of 2016, and the stock market has had a bumper year.

The reason we are still standing is that the government have covered the tab. In creating more money, the state did what it always has had the capacity to do – it took over from a failing private sector. This included paying the wages of close to 10 million furloughed workers. So, there is a strong argument for querying the restraint that comes with the idea that the state can only spend what it taxes and borrows.

Yet, in the UK, despite this firepower to create money out of nothing at the state’s disposal, we are already beginning to hear the murmurings of austerity: that we will need to pay it all back in the post-pandemic world; that there is no magic money tree and we will need to suffer, to tighten our belts. This is nonsense, but unless the process of money creation is demystified, we may well have to face another decade of needless austerity.

Indeed, the impact on our communities of not recognising and addressing the money-creation problem is significant. In the UK the percentage of the nation’s wealth controlled by the bottom 90 per cent of the population had been steadily growing for a century up until the early 1980s, but since then it has started to decrease. Now, the richest 1 per cent in the UK control 22 per cent of the country’s wealth. In the US it’s even worse. The richest 1 per cent account for 39 per cent of the nation’s wealth. At the same time, real wages haven’t improved since the 1970s, social services are hollowed out, public healthcare is struggling, work is precarious, and education is increasingly expensive, as our societies are becoming structured towards serving the needs of the wealthy.

That the policies which have led to this situation have been barely challenged is testament to the power of the myth that cloaks the unjust reality of how our economy works. If you accept the prefabricated set of interpretations behind the myth, then there is no way to challenge the status quo; there is no way for the state to set things right because the state, like a household, is restricted by a finite budget (tax and borrowing). What has made this so outrageous over the last decade is that while this myth has been spread and amplified by the government, the state has simultaneously been creating money through QE and pumping it into a sector of the economy that benefits the already wealthy. It is only through recognising the absurdity of this state of affairs that can we hope to build a better future.

The Pound and the Fury: Why Anger and Confusion Reign in an Economy Paralysed by Myth by Jack Mosse. Manchester University Press, £14.99.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks