Hamish McRae: When the money taps are turned off, the scramble to recovery will begin

Economic View: The world ought to have several years of decent cyclical growth until the next recession

If central banks print shedloads of money it has to go somewhere and the price of assets goes up. But when they stop printing, as the Federal Reserve will eventually do despite last night's surprise, does that mean that prices will go back down? It is not, of course, quite as simple as that, but the world's financial markets are heading into unknown territory because we have never had quantitative easing on the scale we have just experienced, or at least never in peacetime. So there is no precedent for what is beginning now.

Here in the UK it is pretty clear that QE is finished. The issues are when and how the Bank of England's stock of the national debt will be sold back to long-term holders and when and how interest rates will rise back to normal levels. The general assumption is that the Bank will be forced to increase interest rates earlier than the "forward guidance" it has sought to give.

At the long end policy has already been tightened, for long-term rates have doubled since the summer of last year and sterling has been the strongest performing major currency this year. Anyone who took the efforts of Sir Mervyn King to talk down the pound last spring as a "buy" signal will have done very well.

But we are a sideshow on the global bond and equity markets. The big driver is and will remain the Federal Reserve. The rise in US bond yields since the summer of last year, and particularly since the spring, has pulled up yields elsewhere. A year ago 10-year US treasuries yielded 1.8 per cent; now they yield 2.8 per cent. Ten-year gilts have gone from 1.9 per cent to 3 per cent. German bunds have risen from just over 1.6 per cent to just below 2 per cent, showing that even Germany is not immune.

You can read this at least three ways. One is to say that the end to the Fed's QE programme, albeit not starting today, is already "in the markets" and long rates would only rise much further if there were some unexpected new blow, say a sudden rise in inflation. Another is to say that if even the prospect of an end to QE has pushed up rates, wait until things really get back to normal. And a third (which I rather favour) is to say that bond yields were absurdly low last year and this is a sensible return to normality.

So that is where we are now; what of the future?

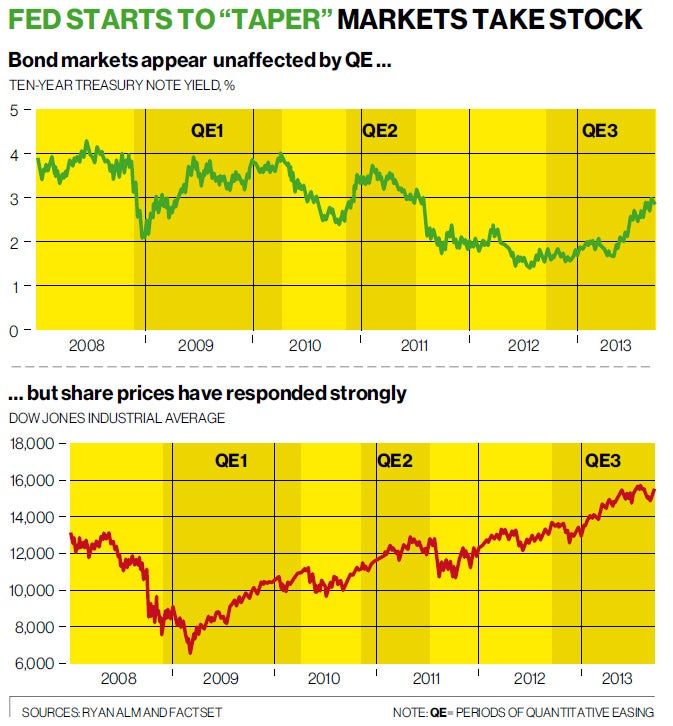

The graphs show how the three bouts of QE in the US (the third still continuing) have affected bonds and equities. You would expect these to depress bond yields and boost equity prices. But actually they don't seem on the face of it to have had much effect on bond yields, for the big declines in yields occurred between the bouts of QE, not during them. However, they do seem to have had a strong impact on share prices, for QE coincides with sharp increases in the Dow. On the basis of this, you might expect not a lot to happen to bond yields either way, but share prices to struggle to sustain their present strong performance.

Would that it were so simple. Those bouts of QE all took place against a background of weak demand – very weak in the first instance. During the intervals demand continued to be pretty weak. Now the end of QE comes at a time when demand is decently strong: forecasts for US growth next year range between 2.5 per cent and 3 per cent. More broadly, the developed world as a whole seems to be recovering, with even the eurozone forecast to grow next year, but recovering with plenty of slack to be absorbed.

We cannot hope to get the detail right, but the world ought to have several years of decent cyclical growth until the next recession. Pessimists argue that because we have been left with a huge burden of debt, the current recovery will be weaker than previous ones.

Optimists point to the amount of slack in the economy and that growth has in the past reverted to mean, which would suggest a strong recovery lasting several years. Both, however, do expect some years of growth, growth that will support corporate earnings and justify the present relatively high levels of share prices.

If this is anything like right the "not much happens to bonds but shares will be weak" message has to be modified a bit. The common-sense position would be to note that bond yields are still historically low. Just look at that top chart: they still look low don't they? Investors that played the so-called great rotation game earlier this year, rotating holdings out of bonds and into equities, have done very well. It may turn out that the rotation has some way still to run, for shares at the present level are pricing in decent growth, rather than a runaway boom.

This big point here is that the world faces several years of scrambling back to balance. In another three or so years' time, barring some dreadful catastrophe, fiscal deficits will be back to sustainable levels and interest rates will be positive. The pile of debt will still be there but a decent start will have been made at chipping it down.

The detail will vary from country to country and I fear that much of southern Europe will still be struggling. But elsewhere living standards will be climbing again and unemployment will, in most countries, be a structural problem rather than a cyclical one.

We will look back on this period, including the ending of the Fed's QE programme, as a natural and inevitable process. There will be debates as to whether the exit could have been managed better, started earlier, done faster or slower – whatever. But those monthly purchases have to be stopped and that is all there is to it.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks