Oil price jumps 2% as Saudi Arabia and Russia extend production cut

Global inventories aren’t yet at the level targeted by OPEC and its allies, Saudi Energy Minister Khalid Al-Falih and his Russian counterpart, Alexander Novak said

For free real time breaking news alerts sent straight to your inbox sign up to our breaking news emails

Sign up to our free breaking news emails

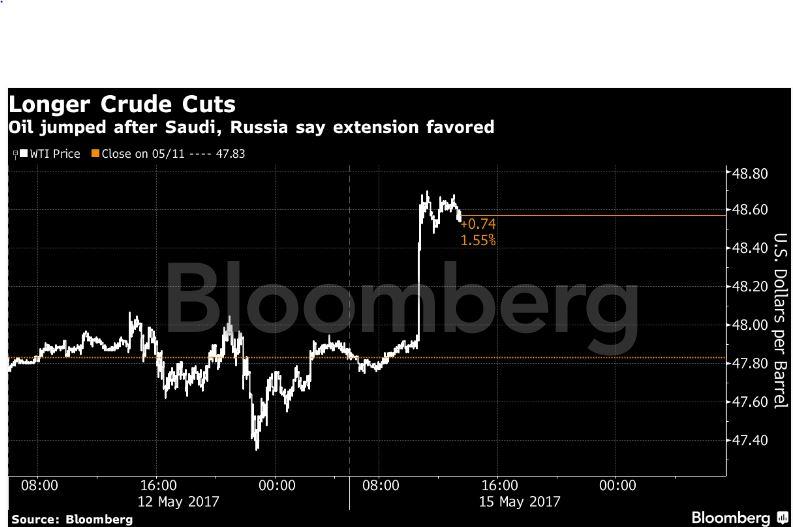

Oil jumped to its highest level in two weeks after the Saudi Arabian and Russian energy ministers said they are in favour of extending a production-cut deal for nine months.

Futures added as much as 2.2 per cent in New York, on course for their highest close since 28 April. While output curbs that started January are working, global inventories aren’t yet at the level targeted by OPEC and its allies, Saudi Energy Minister Khalid Al-Falih said in Beijing alongside his Russian counterpart, Alexander Novak. The ministers agreed the deal should be extended through the first quarter of 2018 at the same volume of reductions, they said.

“The market is certainly reacting to comments from Saudi Arabia and Russia’s ministers, and it should help at least maintain current prices,” Will Yun, a commodities analyst at Hyundai Futures, said by phone. “However, we’ll see whether the rebound remains until the US market opens. It could be short-lived and may not be able to boost prices anywhere above $60 or $70.”

Russia and Saudi Arabia, the largest of the 24 nations that agreed to reduce supply for six months, are reaffirming their commitment to the deal amid growing doubts about its effectiveness. An increase in Libyan output, together with a surge in North American production and signs of recovery in Nigeria, may undercut OPEC’s strategy to re-balance the market and prop up prices.

West Texas Intermediate for June delivery climbed as much as $1.04 to $48.88 a barrel before trading at $48.82 on the New York Mercantile Exchange at 7:56 a.m. in London. Total volume traded almost double the 100-day average. The contract gained 3.5 percent last week.

Brent for July settlement added as much as $1.04, or 2.1 per cent, to $51.88 a barrel on the London-based ICE Futures Europe exchange. The contract increased 7 cents to $50.84 on Friday. The global benchmark crude traded at a premium of $2.70 to July WTI.

Extending the curbs at already agreed-upon volumes is needed to reach the goal of reducing global inventories to the 5-year average, the energy ministers of the world’s biggest oil producers said in a joint press conference. They will present their position at a meeting of OPEC and other nations that are part of the agreement on 25 May in Vienna.

OPEC members agreed in November to cut output by 1.2 million barrels a day, and several non-members, including Russia, agreed in December to contribute a combined 600,000 barrels a day of reductions.

“Preliminary consultations show that everybody is committed” to the output agreement and no country is willing to quit, said Novak. “I don’t see reasons for any country to quit.”

Business news: In pictures

Show all 13Rigs targeting crude in the U.S. increased for a 17th week to 712, the highest since April 2015, Baker Hughes data showed on Friday. The number of working rigs has more than doubled from a 2016 low of 316 in May and is up more than 30 percent so far this year.

Oil-market news:

Money managers have cut their bullish Nymex WTI bets by 34,290 net-long positions to 168,814, weekly CFTC data on futures and options show. Libya is ratcheting up oil output with less than two weeks to go before the world’s biggest exporters decide whether to extend production cuts to clear a supply glut.

Bloomberg

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies