Support truly

independent journalism

Our mission is to deliver unbiased, fact-based reporting that holds power to account and exposes the truth.

Whether $5 or $50, every contribution counts.

Support us to deliver journalism without an agenda.

Louise Thomas

Editor

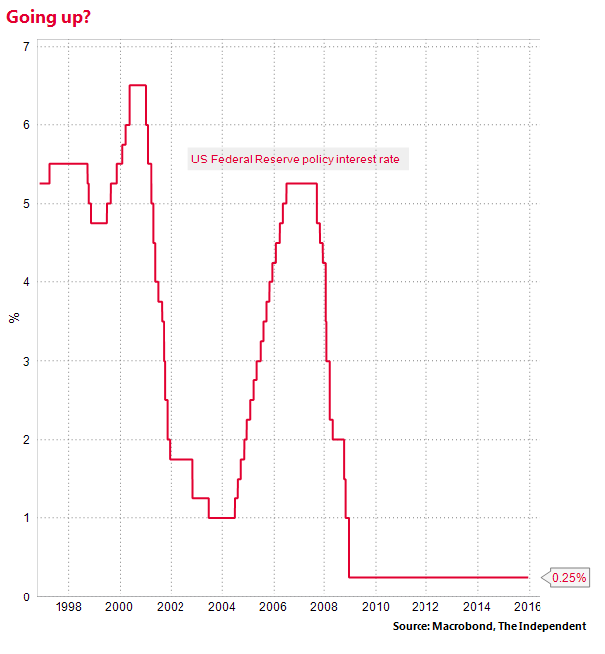

America’s central bank, the Federal Reserve, is almost universally expected by financial traders to put up interest rates for the world’s largest economy on Wednesday in order to reduce the risk of a burst of inflation.

The move has a deep economic significance because this will be the first time the Fed has put up rates since 2006. On the face of it a hike would signal the US economy has returned to something like normality and has finally recovered from the deep damage inflicted by the global financial crisis. But there is also profound uncertainty about how the economy will cope with this monetary tightening after such a long period of rock-bottom 0.25 per cent rates. Here we look at some of the possible impacts of the Fed’s fateful decision on Wednesday evening.

1) Impact on US households and employment

If rates do rise the cost of taking out a new mortgage in the US will become more expensive. The cost of unsecured consumer credit will also increase. But few expect a 0.25 percentage point increase in the Federal Funds rate to 0.5 per cent to prompt a destructive collapse in household spending.

For one thing most Americans have fixed, rather than floating, rate mortgages meaning the impact will not be immediate. A greater fear than a return to recession is that a rate hike will slow growth unnecessarily. “It is entirely possible that in trying to slay the inflation bogey by raising rates the Federal Reserve merely crimps economic growth” says Peter Toogood of City Financial.

The headline US unemployment rate is currently just 5 per cent, down from a peak of 10 per cent in 2009. But the participation rate has plummeted from 66 per cent before the financial to around 62 per cent today. And wage growth remains tepid. Some economists think this implies there is still considerable slack in the labour market and that tightening monetary policy now will mean that the slack will not be rapidly used up, creating a needless waste of resources.

“The clamor for higher rates has nothing to do with the public interest” argues the Nobel economics Laureate Paul Krugman.

Another fear among economists is the “neutral” rate of interest is now lower than it was before the financial crisis for a demographic and structural economic reasons, meaning rates will not climb to their old average of around 4-5 per cent, but may top out at at only 2-2.5 per cent. This means if another recession does hit the US it will be hard for the Fed to stimulate growth by cutting rates again because they will already be uncomfortably close to zero.

This asymmetry of risk, these economists argue, makes the case for only raising rates when inflation is an unequivocal and unmistakably imminent threat.

2) Impact on US companies

A rate hike will mean the cost of borrowing also rises for companies. Yet this is unlikely to have a direct impact on big American companies’ investment plans.

These firms are so cash rich they don’t actually need to borrow to invest. Indeed higher rates could make them more inclined to hang on to the cash because they will earn higher returns on their bloated balances. And if the rate rise impeded aggregate consumer demand growth it could reduce their willingness to spend those surpluses in expanding their productive capacity.

Further, if rising interest rates cause financial market turbulence that could also undermine their willingness to invest.

Finally, a rate hike will could push up the value of the dollar against other currencies, making US exports less competitive in global markets and reducing corporate profit growth. That too could result in lower investment than otherwise – although the dollar has already been rising fast this year as expectations of a rate rise have piled up.

3) Impact on bonds and shares

Declines in interest rates generally push up the value of government debt and corporate bonds.

The assumption is that a rise in rates will have the opposite effect. One $788m investment fund run by Third Avenue Management that invested in high-yield (risky) corporate debt had to wind itself down last week due to losses and redemption.

This fund was particularly exposed due to the risk and illiquidity of its portfolio. Yet there could well be others that get into trouble too. The activist investor Carl Icahn has suggested there is a “meltdown” coming for high-yield debt. The question is whether these failures will set off a general financial panic.

Some pundits think this a risk. “At this moment of fragility, raising rates risks tipping some part of the financial system into crisis, with unpredictable and dangerous results” says the former US Treasury Secretary (and one time leading candidate to take charge of the Federal Reserve) Larry Summers.

Share prices also tend to benefit from monetary stimulus – but the S&P 500 is already trading lower than at the start of the year, implying the impact of the rate rise might already be priced in for equities.

4) Impact on rest of the world

The American dollar is the world’s number one reserve currency. The bulk of cross-border trade and investment is denominated in US dollars. Emerging market states hold most of the foreign exchange reserves in dollar debt. They also often borrow in dollars.

All this means that what the Fed does has a profound impact on the global financial system. During the 2013 “taper tantrum”, when the Fed announced that it would be reducing the pace of its asset purchases, traders yanked money out of emerging market economies in order to plough it back into (anticipated) higher-yielding US assets. This rapid dollar flight caused major problems for states such as India, Mexico, Turkey and Indonesia.

Those countries seem better prepared for US monetary tightening now. “Fundamentals have improved in several large emerging market economis since the taper tantrum” say analysts from Bank of America. But there is still a non-neglible risk that the actions of the Fed could set of an earthquake elsewhere, pushing the global economy back into recession.

Some note that it would not take much to tip the scales. The Chinese economy, still the world’s big motor of economic growth, is slowing down at an alarming pace. And the world economy is already set for its slowest growth since the financial crisis this year.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments