The Independent's journalism is supported by our readers. When you purchase through links on our site, we may earn commission.

How to apply for student loan forgiveness – and scams to watch out for

Here’s what you need to know about student loan forgiveness and the plans available for you

The cost of colleges has increased over recent years in the United States and paying for fees through savings and investments is not as easy as it used to be.

As of this year, Americans now owe $1.77 trillion in federal and private student loan debt and while the Biden administration tried to decrease that amount, the Supreme Court issued a decision blocking the one-time student debt relief plan.

The three-part plan aimed to help working and middle-class families and included a loan forgiveness of up to $20,000.

It was set in place to address the “financial harms of the pandemic” and “provide borrowers with a smooth transition back to repayment.”

Here is everything you need to know about student loan forgiveness and what you might need to watch out for…

What plans are available and how is my monthly payment amount calculated as a repayment plan?

Federal Student Aid has said that in certain circumstances if a person has taken out student loans, these can be “forgiven”, “cancelled” and “discharged”. This basically means you may not need to pay some or even all of the loan.

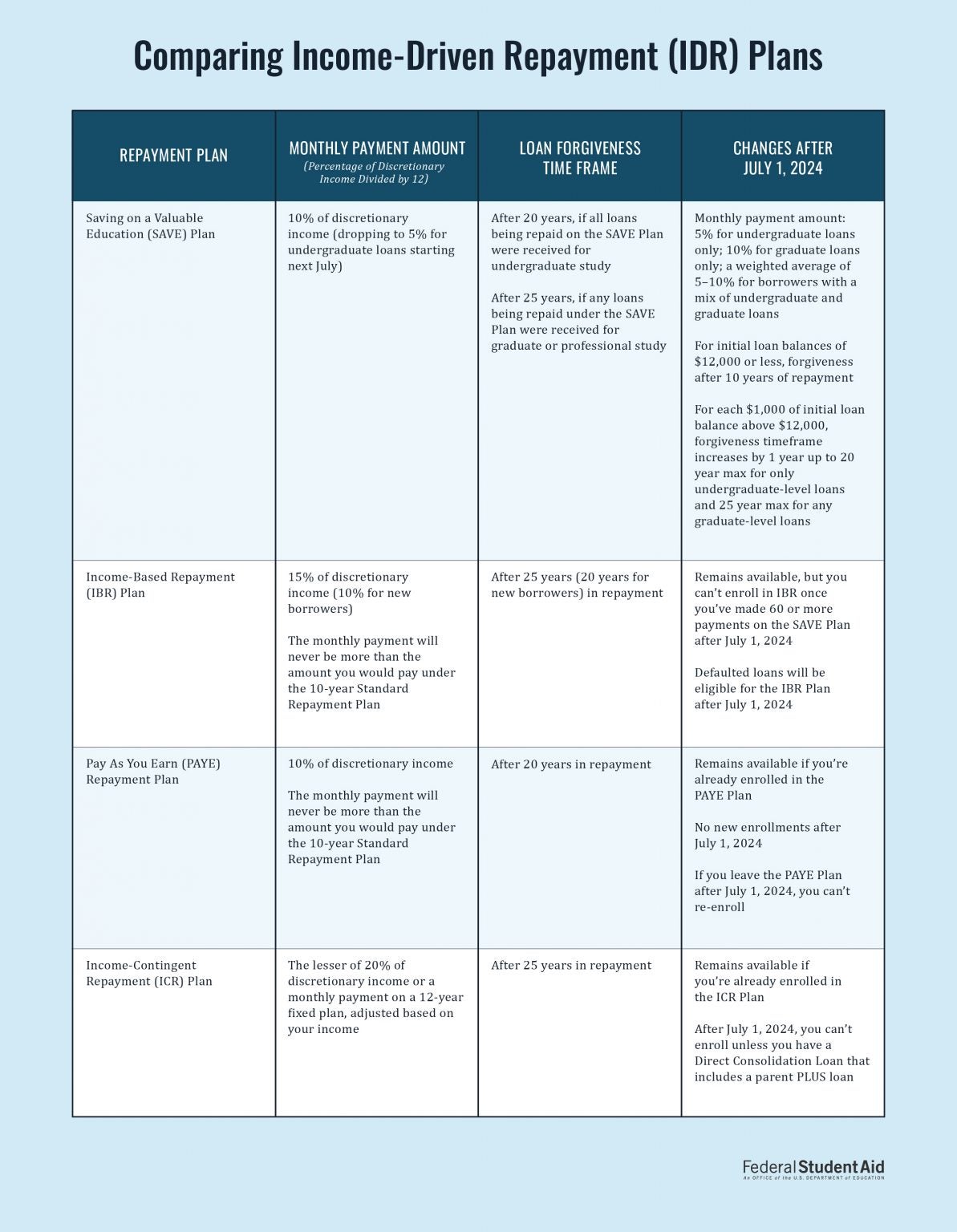

There are currently four different income-driven repayment plans, as per the Federal Student Aid website – these are:

• Saving A Valuable Education (SAVE) plan – formerly known as PAYE. This payment generally takes 10 per cent of your discretionary income.

• Income-based Repayment (IBR) – for this payment it is generally 10 per cent of your discretionary income, but never more than the 10-year Standard Repayment Plan amount.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

• Pay As You Earn (PAYE) – The FSA says this is generally 10 per cent of your income if you’re a new borrower on or after 1 July 2014, but never more than the Standard Repayment Plan amount.

Generally, 15 per cent of your discretionary income if you’re not a new borrower on or after 1 July 2014.

• Income-contingent Repayment loan (ICR) - The lesser of the following: 20 per cent of your discretionary income or what you would pay on a repayment plan with a fixed payment over the course of 12 years, adjusted according to your income.

“Under all four plans, any remaining loan balance is forgiven if your federal student loans aren’t fully repaid at the end of the repayment period,” the FSA says on its site.

The table below, provided by the Federal Student Aid website shows data comparing monthly amounts and repayment periods under each plan.

Who qualifies for student loan forgiveness?

Each individual income-driven replayment (IDR) plan has its own set of further eligibility requirements that you’ll need to meet to qualify.

For, SAVE any borrower with qualifying student loans is eligible for this plan.

With PAYE and IBR, the estimated payment you make for either of these plans has to be less than what you would pay on the Standard Repayment Plan within a 10-year period.

But for PAYE, only loans given after 1 October 2011 are eligible.

And with ICR, just like SAVE, any federal student loan borrower is eligible for this plan. But this plan is the only income-driven repayment plan that accepts PLUS (Parent Loan for Undergraduate Students) loans made to students.

How do I apply?

The FSA recommends that you contact your loan servicer if you have any questions as this will help you decide whether one of these plans is right for you.

To apply for the right plan, you can fill in the form online or via paper format – which you can get from your loan servicer.

During the application process, you’ll be asked to provide income information that will be used to determine your eligibility for the PAYE or IBR plans and to calculate your monthly payment amount under all income-driven repayment plans.

Find out more about the IDR plan request here.

Is there a deadline for applications?

The application period for student loan forgiveness will close on 31 December 2023.

How to avoid student loan scams

Getting a bunch of texts, emails and calls about student loan forgiveness?

Scams come in different forms, so it’s best to take extra caution. Here are a few ways to spot a scam:

- Being asked for log-in information: the FSA and loan providers will never ask you for these details.

- Promises that are too good to be true: according to the FSA, most government forgiveness programs require years of qualifying payments and/or employment in certain fields before forgiving loans.

- Typos in texts, emails or other forms of communication.

- Unofficial addresses or phone numbers:remember, official emails from the FSA will only come from these emails:

noreply@studentaid.gov

noreply@debtrelief.studentaid.gov

ed.gov@public.govdelivery.com

And text messages from the FSA will only come from 227722 or 51592.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks